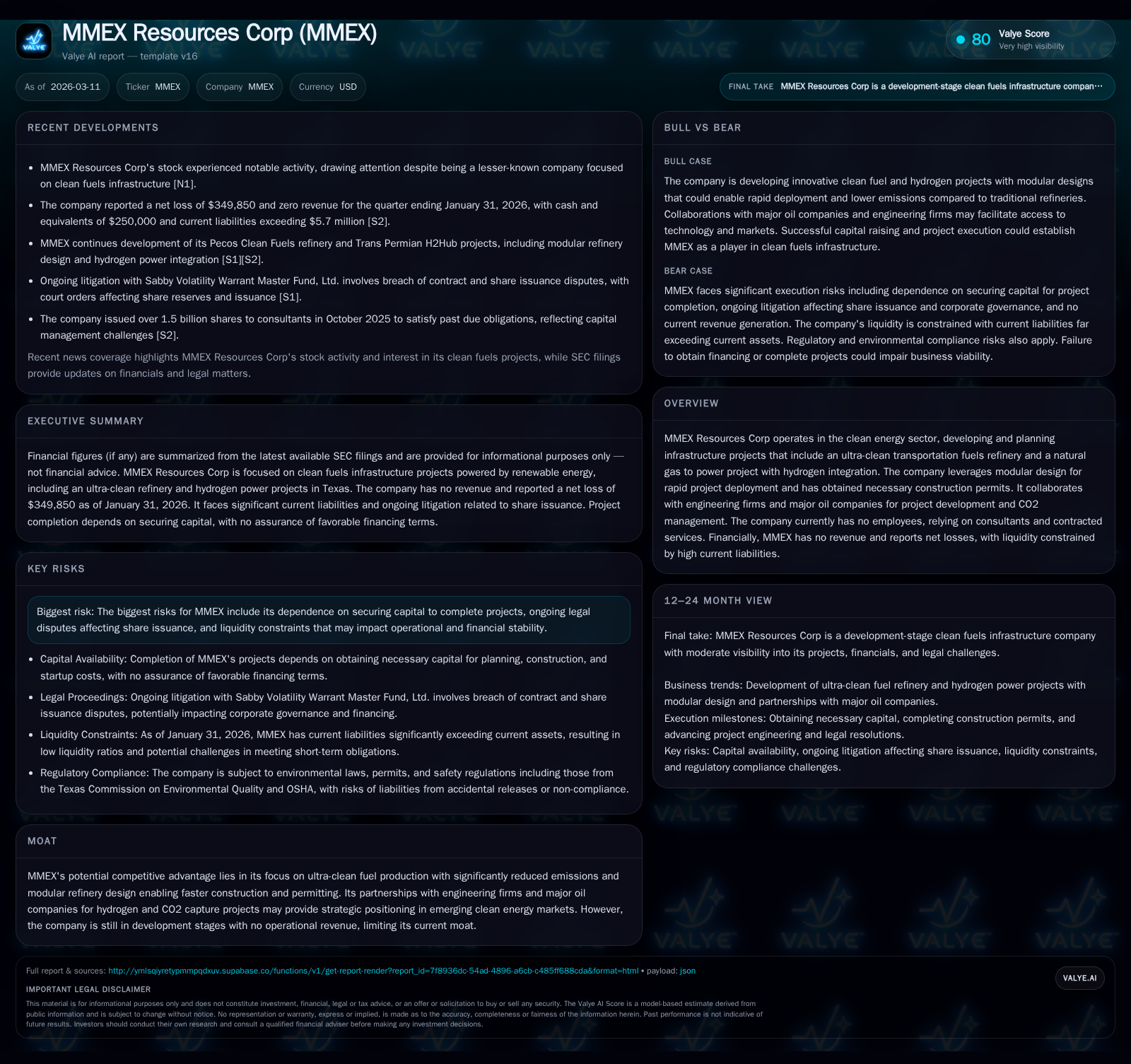

MMEX Resources Corp Navigates Development Challenges Amid Financial and Legal Headwinds

Focused on ultra-clean fuel infrastructure with modular design, MMEX Resources Corp remains pre-revenue with persistent operating losses, constrained liquidity, and ongoing litigation affecting capital structure.

MMEX Resources Corp is advancing plans for an ultra-clean transportation fuels refinery and a natural gas to power project with hydrogen integration at its Pecos County, Texas site. The company has secured key construction permits and established partnerships with engineering firms and major oil companies. However, it continues to operate without revenue, reporting consistent net losses and negative equity. Liquidity pressures are acute, with current liabilities vastly exceeding current assets, while legal disputes over convertible note conversions have complicated share issuance and capital allocation. MMEX’s growth prospects hinge on successful financing and execution of its clean energy projects amid regulatory and market challenges.

Company Overview and Historical Performance

MMEX Resources Corporation, established in Nevada in 2005 and restructured via reverse merger in 2010, focuses on clean fuels infrastructure projects powered by renewable energy. Its primary initiatives are located in Pecos County, Texas near the Permian Basin.

The flagship Pecos Clean Fuels & Transport refinery is designed for up to 11,600 barrels per day capacity producing zero sulfur gasoline (87°), ultra-low sulfur diesel, and low-sulfur fuel oil. This Ultra Fuel® configuration targets criteria pollutant emissions approximately 95% below those of conventional Gulf Coast refineries—a material environmental improvement aligned with tightening regulations.

Complementing this is the Trans Permian H2Hub project featuring a phased approach: initially generating electric power using 100% natural gas turbines with plans to transition to blue hydrogen production integrated with CO2 capture for enhanced oil recovery through partners identified as super major oil companies. The hydrogen produced is intended as zero-CO2 refinery fuel gas.

Construction leverages modular fabrication enabling off-site assembly with an estimated timeline of 18 months post-financing and permitting. The Texas Commission on Environmental Quality granted the necessary construction permit in February 2022.

Financially, MMEX has generated no revenue over the last four fiscal years ending April 30 (FY2022–FY2025) while reporting persistent operating losses that moderated slightly in FY2025 compared to prior years. Negative net income follows a similar pattern. Operating cash flow remains negative but shows modest improvement year-over-year.

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -2 | 0 | -1 | +6.7% |

| 2024 | 0 | -2 | 0 | -1 | -24.5% |

| 2023 | 0 | -2 | -1 | -2 | -765.4% |

| 2022 | 0 | 0 | -3 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 38.4 |

| 2024 | 0 | 64.6 |

| 2023 | -1 | 69.1 |

| 2022 | -4 | 13.0 |

Source: SEC companyfacts cache [F1].

Note: The absence of revenue highlights MMEX's pre-operational status as it progresses through development stages.

Capital Structure and Liquidity

As of January 31, 2026, MMEX reported current assets of approximately $14.7K against current liabilities exceeding $5.7 million—indicative of critical liquidity challenges that may jeopardize ongoing operations without successful capital raises. Cash reserves have been minimal in recent quarters.

The company employs no full-time staff but contracts consultants compensated primarily via equity issuances to conserve cash. These shares include those issued to entities related to two directors; however legal disputes have constrained share issuance capabilities.

A key legal challenge involves Sabby Volatility Warrant Master Fund’s litigation alleging breaches related to convertible note conversions and preferred stock warrants. Court orders imposed restrictions on share issuances until compliance was achieved through increasing authorized shares reserves to approximately 35 billion shares with about 10 billion reserved for Sabby conversions. Litigation entered discovery phases following these settlements.

Growth Prospects and Industry Positioning

MMEX’s competitive advantage lies in its ultra-clean fuel production technology combined with modular refinery design allowing expedited permitting and construction relative to conventional facilities—features well suited for evolving low-emission fuel markets.

Partnerships with Polaris Engineering and super major oil companies enhance technical capabilities and access to feedstocks like natural gas alongside advanced blue hydrogen reforming and CO2 capture technologies supporting decarbonization goals.

Nonetheless growth hinges on securing substantial financing required for project completion since operational revenues remain nil and cash burn persists. Progress beyond permitting into active construction phases remains unconfirmed publicly.

Locating modular units near crude production areas optimizes logistics costs while tapping into expanding regional demand amid tightening environmental regulations impacting traditional refining economics nationally.

Returns and Capital Allocation Analysis

Persistent operating losses combined with significant negative equity nearing $6 million as of FY2025 indicate an absence of positive returns typical in mature energy companies. An approximate ROE calculation based on net income divided by equity yields a positive figure; however this likely reflects distortions from deeply negative shareholders’ equity rather than true profitability.

Capital expenditures ceased after FY2022’s moderate spend reflecting initial engineering efforts; no new capex occurred through April 2025 indicating limited physical asset additions pending financing closure.

No dividends or share repurchases have been declared or executed given financial constraints. Equity compensation via share issuances remains the primary method for consultant remuneration but introduces dilution risks compounded by ongoing litigation affecting share authorization limits.

Outlook Considerations

Absent explicit forward guidance or disclosed milestones post-latest filings,[N#] MMEX’s advancement depends critically on:

- Securing capital sufficient for construction start-up costs,

- Resolving litigation impacts limiting equity issuance capabilities,

- Transitioning from permitting into active project construction,

- Market acceptance of ultra-clean fuel products amidst sector challenges,

- Regulatory developments incentivizing blue hydrogen adoption,

- Potential expansion of strategic partnerships beyond current engagements.

Delays or failures in these areas could materially hinder project realization while exacerbating liquidity pressures; conversely successful execution could position MMEX favorably amid accelerating shifts toward low-carbon fuel infrastructures.

This analysis is based exclusively on MMEX Resources Corporation's publicly filed SEC documents cited herein along with numeric data extracted from SEC companyfacts as of early 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments