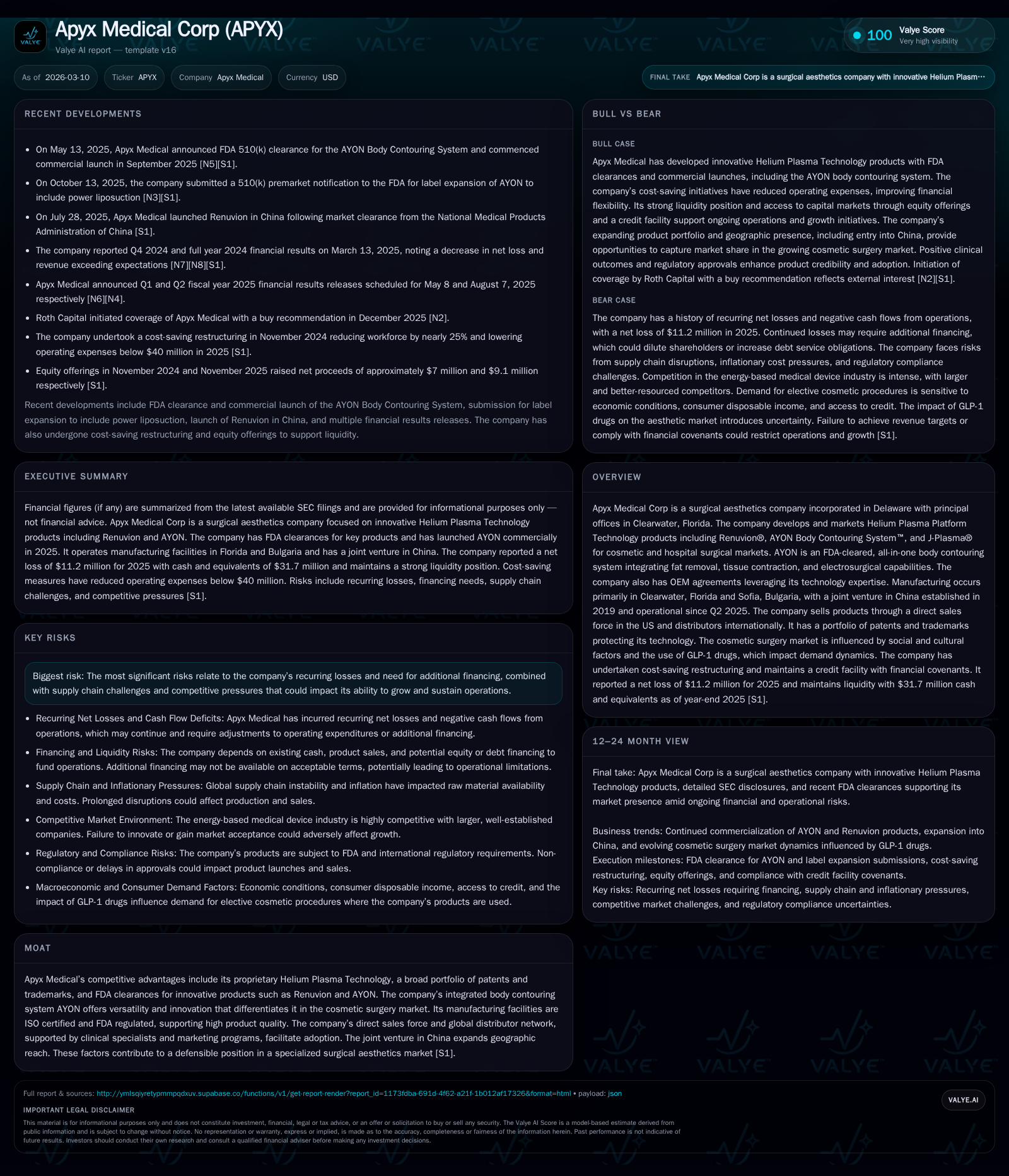

Apyx Medical Advances Body Contouring Tech Amid Ongoing Losses and Regulatory Challenges

Apyx Medical Corp leverages patented Helium Plasma Technology in surgical aesthetics while navigating recurring losses and market pressures.

Apyx Medical Corporation specializes in innovative surgical aesthetic devices based on proprietary Helium Plasma Platform Technology, including the Renuvion and AYON systems. The company’s revenue showed modest growth in recent years but remains unprofitable with persistent operating losses and negative cash flow. Its strategic progress includes FDA clearance for AYON and geographic expansion via a joint venture in China. However, macroeconomic headwinds, regulatory complexity, supply chain risks, and competitive dynamics continue to challenge near-term profitability and cash flow sustainability.

Company Background and Business Overview

Apyx Medical Corporation is a Delaware-incorporated surgical aesthetics company headquartered in Clearwater, Florida. It develops and markets cutting-edge devices built around its proprietary Helium Plasma Platform Technology. Its key products include Renuvion®, the AYON Body Contouring System™, and J-Plasma®, which serve cosmetic surgery and hospital surgical markets globally [S1].

Renuvion offers surgeons controlled thermal energy to remodel tissue effectively with precision heating. AYON stands out as an all-in-one FDA-cleared body contouring platform combining fat removal (including ultrasound-assisted liposuction), tissue contraction powered by Renuvion technology, electrocoagulation for excess tissue removal, volume enhancement capabilities, infiltration systems, and dual aspiration allowing simultaneous users [S1]. This integration positions AYON uniquely versus more fragmented competitors.

Manufacturing is centralized primarily at two ISO-certified facilities located in Clearwater and Sofia, Bulgaria. The company also expanded internationally via a manufacturing joint venture operational since Q2 2025 in China – aimed at accelerating access to Asia’s growing cosmetic surgery market [S1]. Sales execution relies on a direct sales force domestic to the U.S. augmented by distributors overseas [S1].

Historical Financial Performance

Financially, Apyx Medical has struggled with recurring operating losses though it recorded modest improvement in top-line revenues recently. Revenue increased approximately 11% year-over-year reaching $8.3 million in FY2025 [F1]. Operating losses narrowed significantly from -$18.8 million in FY2024 to -$6.4 million in FY2025 [F1]. Net losses remain substantial at approximately -$11.2 million for FY2025 [F1]. Free cash flow was negative at roughly -$9.1 million (operating cash flow of -$8.0 million less capex of $1.1 million) indicating ongoing operational cash burn exceeding investment outlays [F1]. Equity declined sharply from about $37.6 million at end-2022 to $14.5 million by end-2025 due to cumulative net losses [F1]. The company maintains a strong current ratio of about 5.0 owing to current assets of $58.5 million against current liabilities of $11.7 million as of December 31, 2025 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | -8 | -6 | 1114000 | +52.2% |

| 2024 | -23 | -18 | -19 | 722000 | -25.4% |

| 2023 | -19 | -5 | -17 | 533000 | +19.3% |

| 2022 | -23 | -20 | -24 | 1010000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -9 | -77.1 |

| 2024 | -19 | -165.1 |

| 2023 | -6 | -70.1 |

| 2022 | -21 | -61.7 |

Source: SEC companyfacts cache [F1].

Growth Drivers and Market Positioning

Apyx's growth prospects hinge notably on continued adoption of its innovative technology suite within the growing cosmetic surgery segment worldwide, supported by social acceptance trends towards elective aesthetic procedures [S1]. The AYON system's FDA clearance achieved May 13, 2025 is central to competitive differentiation as it integrates multiple procedural functions into one platform designed for surgeon convenience and improved patient outcomes [S1]. Commercial launch began September 2025 with ongoing efforts toward FDA label expansion for power liposuction anticipated in Q2 2026 [S1].

The company's strategic establishment of a manufacturing joint venture facility in China since Q2 2025 expands geographical market reach into Asia’s fast-growing cosmetic surgery market offering potential new revenue streams beyond established U.S./EMEA channels [S1]. Additionally, leveraging OEM partnerships allows monetizing proprietary waveform technology expertise without direct marketing investment [S1].

Cost containment initiatives implemented following a workforce reduction (~25%) announced November 7, 2024 have reduced operating expenses below $40 million annually by FY2025 compared to prior years exceeding $48 million [S22], aligning with management’s focus on optimizing cost structure while maintaining sales efforts.

Risks and Constraints

Key risk factors remain relevant:

Recurring Operating Losses & Liquidity Needs: The company continues generating net losses which deplete equity capitalization posing going concern risks without successful capital raises or improved profitability [S12]. Debt covenants tied to revenue growth impose performance thresholds critical to avoid defaults under credit agreements [S6]. Recent equity offerings indicate attempts to bolster liquidity but involve ownership dilution.

Supply Chain Dependencies: Significant reliance on single-source suppliers for raw materials such as plastics and specialized components alongside outsourced subassemblies creates vulnerability to availability disruptions or price volatility that could affect margins or product delivery reliability [S16].

Macroeconomic & Market Sensitivities: Exposure primarily to elective cosmetic procedures means demand fluctuates with consumer disposable income shifts influenced by inflation and interest rate changes impacting financing availability for patients or practitioners; Federal Reserve policy uncertainty adds variability [S24][S12].

Regulatory Complexity: Global distribution requires navigating increasingly stringent regulatory environments including FDA clinical data scrutiny, intensified post-market surveillance due to EU MDR implementation affecting approval timelines and costs as well as advertising restrictions limiting promotional strategies [S15][S18][S25].

Legal & Product Liability: Product liability claims arising from design defects or adverse patient outcomes may lead to costly settlements or reputational harm despite insurance coverage provisions [S4][S10].

Competitive Environment: Innovation-driven markets require continuous R&D investments to sustain patent protection advantages; competition from incumbents or lower-cost entrants poses ongoing challenges requiring vigilance [S1].

Capital Allocation and Returns Profile

No dividends or share buybacks have been declared historically reflecting prioritization of reinvestment amid net loss conditions [F1]. The equity base eroded from nearly $38 million in early pre-pandemic years down below $15 million currently primarily due to cumulative losses heightening capital preservation concerns [F1]. Operating cash flow remains deeply negative (-$8M in FY25), underscoring dependence on external financing—preferably equity given debt covenant constraints limiting borrowing capacity [F1][S6][S12].

Capital expenditures remain modest though somewhat elevated year-on-year reflecting ramped manufacturing readiness for new product launches and facility enhancements but do not indicate aggressive physical expansion ambitions given financial constraints [F1]. Return metrics are deeply negative reflecting the challenging loss-making stage typical for innovative medical device companies still scaling commercialization efforts.

What To Watch Going Forward (Analysis)

Key developments will likely center on:

- Commercial traction of AYON post-clearance alongside progress toward FDA label expansion expected Q2 2026 affecting addressable market size.

- Execution progress broadening international penetration especially leveraging the Chinese joint venture as Asian markets mature socially toward aesthetic procedures.

- Effectiveness of cost management sustaining margin improvements aligned with revenue scale increases.

- Continued compliance with debt covenants amidst liquidity needs highlighting potential further equity raises.

- Navigating regulatory approval timing prudently while avoiding costly setbacks such as recalls or warnings.

- Macro impacts including shifts in consumer credit availability influencing customer purchasing patterns.

- Monitoring litigation exposure developments particularly related to clinical safety assertions.

These factors collectively will shape whether Apyx advances sustainably toward commercial profitability within the surgical aesthetics sector.

Summary

Apyx Medical Corp presents a specialized surgical aesthetics innovator leveraging proprietary plasma technology powering integrated devices like AYON addressing multi-faceted body contouring comprehensively. After regulatory clearances ramped mid-2025 including entry into China through a joint venture operation, the firm achieved modest revenue growth accompanied by substantial yet improving net losses indicative of early commercialization under stringent cost controls.

Nonetheless risks stemming from discretionary patient demand fluctuations amid economic uncertainties, complex global regulatory hurdles, critical supply chain dependencies, and persistent liquidity pressures present tangible hurdles requiring meticulous strategic execution paired with careful financial stewardship.

Investors should focus keenly on regulatory milestones—especially projected Q2 2026 label expansions—and operational efficiency management amid prevailing macroeconomic sensitivities impacting elective procedure demand globally.

Disclaimer: This analysis is based solely on publicly available information as of March 10, 2026, including SEC filings indexed under Apyx Medical Corporation (CIK:0000719135). It is intended solely for informational purposes without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments