Groupon’s Turnaround: From Marketplace Challenges to AI-Driven Transformation

Groupon's financial recovery and strategic pivot to AI-powered marketplace innovations reshape its path forward amid liquidity constraints.

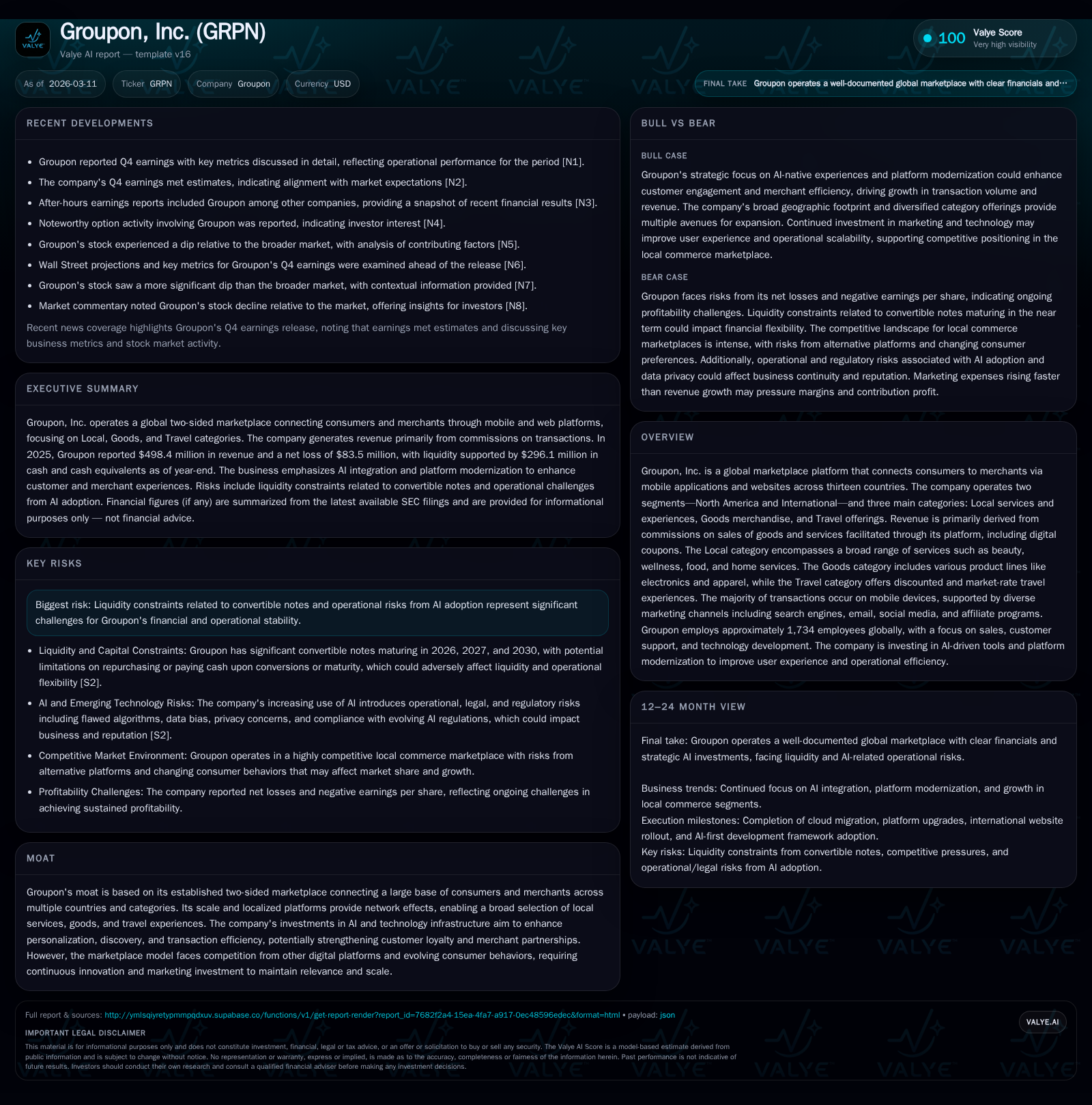

After enduring years of revenue volatility and net losses, Groupon reported a meaningful operating income increase in FY2025, driven by growth in its Local services category and technology enhancements. The company is accelerating investments in AI-native platform capabilities to improve customer discovery and transaction efficiency, aiming to strengthen its two-sided marketplace moat. Liquidity management remains critical as Groupon navigates convertible debt maturities and operational risks linked to its digital transformation. Continued monitoring of capital allocation and market performance will be essential to gauge sustainability beyond recent earnings momentum.

Historical Revenue and Profitability Trends: Journey Through Growth and Volatility

Groupon's financial performance through recent years reflects significant operational challenges alongside signs of stabilization heading into fiscal year ended December 31, 2025. Total revenue was approximately $498 million in FY2025, showing modest growth compared to $493 million in FY2024 but remaining well below earlier peaks such as $799 million recorded in FY2018 [F1]. The company achieved an operating income of $23.6 million in FY2025, a substantial improvement of 168.8% over the prior year's $8.8 million operating income level, highlighting efforts to optimize cost structures and marketplace dynamics [F1].

Net income continued to reflect losses at $83.5 million for FY2025, indicative of ongoing non-operating expenses or investments impacting bottom-line profitability [F1]. Operating cash flow strengthened by 15.4% year-over-year to reach $64.5 million, supporting operational liquidity despite negative net income [F1]. Capital expenditures decreased slightly to $14.6 million, reflecting disciplined investment primarily focused on technology and platform development [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -84 | 64 | 24 | 15 | -41.5% |

| 2024 | -59 | 56 | 9 | 15 | -6.5% |

| 2023 | -55 | 55 | -18 | 19 | +76.7% |

| 2022 | -238 | -136 | -168 | 36 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 50 | 196.2 |

| 2024 | 41 | -144.6 |

| 2023 | 35 | 136.4 |

| 2022 | -172 | -2803.6 |

Source: SEC companyfacts cache [F1].

Table includes key GAAP financials for fiscal years ended December 31 per filings [F1]

Segment and Category Performance Driving Revenue Mix Shifts

The North America segment has been the primary driver of recent revenue growth, with gross billings increasing by over 10% year-over-year to $1.25 billion in FY2025 while International segment experienced a decline of approximately 3%, influenced by strategic divestitures such as Giftcloud and market exits including Italy [S8][S13]. The Local category—comprising experiences like beauty, wellness, food & drink, home services, and automotive care—accounts for roughly three-quarters of global revenues and posted a strong North America gross billings increase of +14.2% year-over-year.

In contrast, the Goods category saw significant contraction with North America gross billings down by 36% and International down by about 12%, reflecting Groupon's strategic de-emphasis on lower-margin merchandise lines [S8]. The Travel category also faced modest declines (-1.9% North America; -8.3% International) amid evolving consumer preferences post-pandemic.

Key operational metrics such as units sold and trailing twelve months (TTM) active customers showed moderate increases or stability supporting sustained engagement within core categories [S13][S16]. Marketing investments increased notably in North America targeting customer acquisition but contribution profit remained flat year-over-year as marketing expense growth offset gross profit gains [S16].

AI Investments and Technology Upgrades Powering Future Marketplace Dynamics

Central to Groupon's strategic turnaround is an ongoing modernization initiative focused on building an AI-native marketplace platform featuring modern API architectures that enable faster innovation cycles and enhanced personalization [S1][S7]. Approximately 84% of transactions occur via mobile devices where AI-powered discovery tools refine relevance scoring and personalized recommendations across user interfaces [S4]. Checkout processes are being enhanced with AI capabilities aimed at improving conversion rates through streamlined customer experiences.

These technological advancements aim to deepen merchant relationships by improving supply-demand matching efficiency while reinforcing network effects vital to two-sided marketplaces' competitive moats in local commerce sectors [S7]. Internal deployment of AI tools also targets increased productivity within product development teams to accelerate feature rollout velocity.

Liquidity Challenges, Convertible Debt, and Capital Structure Maneuvers

Despite operational improvements, Groupon faces notable liquidity pressures tied primarily to outstanding convertible notes aggregating approximately $525 million with maturities spanning March 2026 ($33.7 million remaining principal), March 2027 ($47.3 million), and June 2030 (~$244 million) [S5][S6][S9]. To mitigate near-term refinancing risks, the company completed a fully backstopped Rights Offering in January 2024 that raised $80 million gross proceeds used partly to repay revolving credit facility balances [N1][S12].

Covenants require maintaining liquidity thresholds above $50 million inclusive of undrawn credit lines; credit agreements contain fee adjustments tied to leverage ratios underscoring tight capital management amidst upcoming debt maturities [S9][S15]. Restricted cash related to letters of credit supports international operations under collateral arrangements further affecting liquidity profiles [S20].

The approaching convertible note maturities pose refinancing risks compounded by persistent net losses which may limit access to favorable financing terms or necessitate equity dilution if capital markets conditions deteriorate [S5][N1]. Maintaining balance between funding innovation initiatives like AI platform upgrades while managing debt obligations remains a critical focus.

Cash Flow Generation, Capital Expenditures, and Shareholder Returns

Operating cash flow showed robust improvement reaching $64.5 million in FY2025 driven by stable merchant payables cycles alongside gross billings growth relative to prior periods [F1][S22]. Capital expenditures declined modestly indicating prudent spending focused on software development supporting technology modernization rather than large-scale infrastructure investments [F1][S17].

No dividends have been declared recently nor have share repurchases been executed since before FY2019; however, the company maintains authorization for up to $245 million common stock repurchases which may be deployed depending on market conditions and liquidity considerations [F1][S12]. Equity stood negative at approximately -$42.6 million at fiscal year-end reflective of accumulated losses though free cash flow generation approximates nearly $50 million after capex deductions highlighting potential operational leverage if revenue growth sustains [F1].

Key Earnings Metrics from Q4 2025: What They Tell About Momentum

Q4 disclosures report global gross billings around $424 million with positive momentum driven primarily by North America Local categories while units sold remained stable year-over-year indicating consistent customer demand engagement patterns [N1][N2][S3]. Trailing twelve months active customer counts grew moderately suggesting marketing investments are translating into sustained user activity amid competitive local commerce environments.

Margins benefited from operational efficiencies including amortization cost reductions related to internal software supporting customer-facing applications complementing productivity gains within marketing expense structures resulting in balanced contribution profits despite elevated acquisition spending [N1][N2].

Analyst Expectations and Market Signals: What To Watch Next

Market commentary emphasizes monitoring Groupon's execution risk on scaling AI initiatives without impairing marketplace liquidity or merchant relationships amid intensifying competition from both established aggregators and emerging direct-to-consumer local service providers [N4]. The effectiveness of intelligent personalization algorithms alongside optimized checkout experiences will be pivotal for purchase frequency improvements essential for sustaining take rates.

Additional capital raises or refinancing activities especially surrounding imminent convertible note maturities remain critical factors influencing financial flexibility amidst uncertain macroeconomic conditions including tariff shifts impacting goods procurement costs across product categories still offered by Groupon [N4].

Risks from AI Adoption and Debt Maturities in an Evolving E-commerce Landscape

Adopting AI-centric platform upgrades involves risks such as technical integration challenges potentially causing user experience disruptions or misaligned personalization outputs that could erode merchant loyalty if not carefully managed [S11]. Balancing these technological transitions against significant convertible debt obligations requires vigilant financial planning to avoid balance sheet stress.

Furthermore, legal exposures related to consumer protection claims or intellectual property disputes could lead to unanticipated liabilities increasing indirect costs just as resource allocation intensifies toward innovation investments underscoring the importance of robust regulatory compliance frameworks during this transformation phase [S21].

This analysis synthesizes factual insights derived strictly from substantial disclosures by Groupon Inc., SEC filings, and recent market reports without extending into speculative forecasts or investment opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments