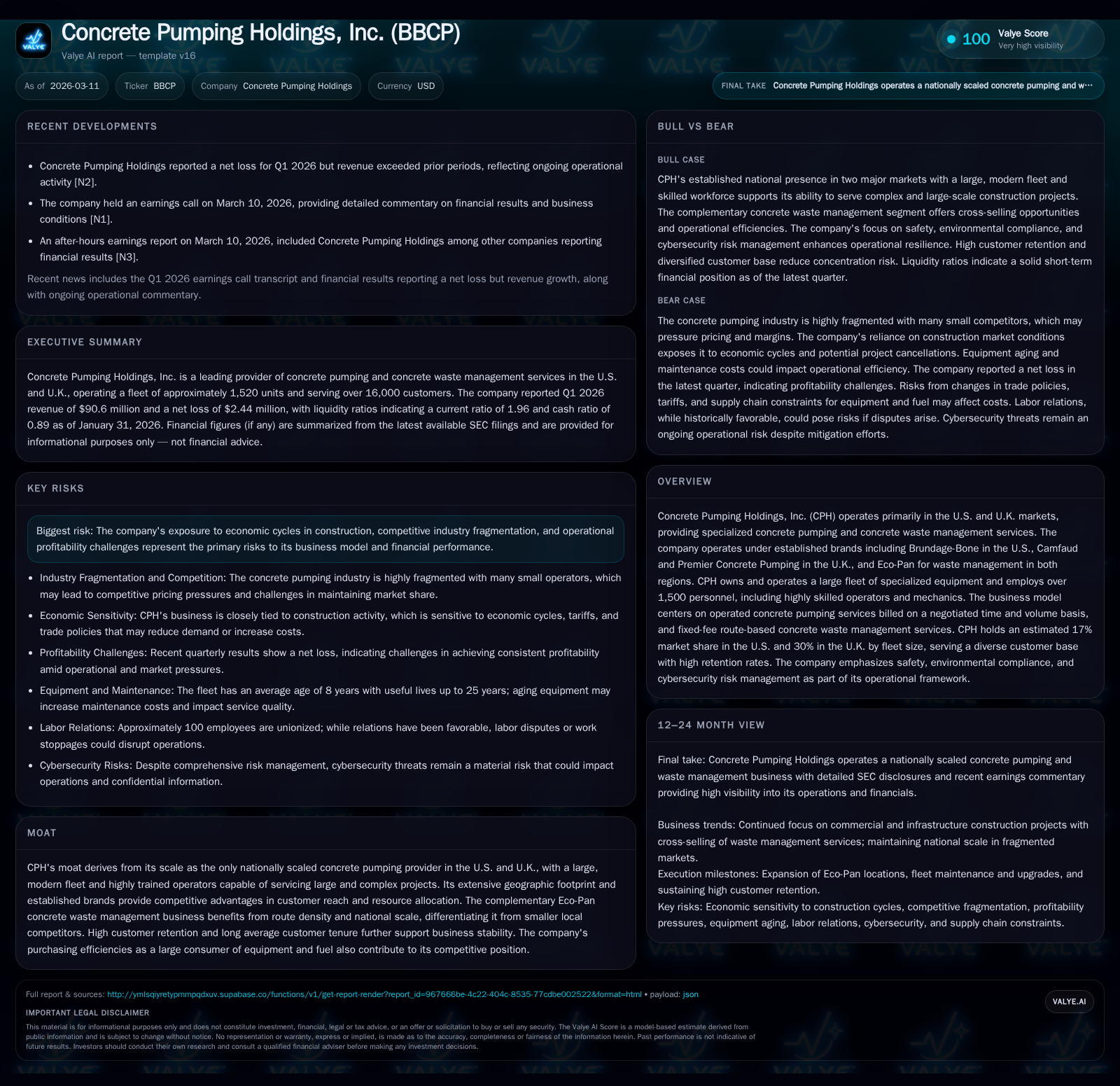

Concrete Pumping Holdings, Inc.: Analyzing Scale and Efficiency in Specialized Construction Services

Concrete Pumping Holdings leverages its unique national footprint and fleet scale in U.S. and U.K. concrete pumping and waste services amid profitability pressures.

Concrete Pumping Holdings, Inc. (CPH) operates the only nationally scaled concrete pumping fleet in both the United States and United Kingdom, with complementary concrete waste management through its Eco-Pan brand. While the company has achieved considerable scale via over 70 acquisitions and maintains strong customer retention, FY2025 results showed a near 8% revenue decline and significant net income compression amid industry cyclicality and margin pressures. Capital allocation balances increased maintenance capex with continued moderate share repurchases. Near-term growth emphasizes cross-border synergies and Eco-Pan expansion, but persistent economic sensitivities and operational costs impose challenges.

From National Growth Leader to Current Performance Shifts: Historical Review

Concrete Pumping Holdings (CPH) has established itself as a leading provider of concrete pumping and concrete waste management services across the U.S. and U.K., distinguished by its rare national scale within a traditionally fragmented industry landscape. The company's expansion has been largely driven by an acquisition strategy exceeding 70 completed deals since inception.

In FY2025, the company reported revenues of approximately $393 million, marking a 7.7% decline from the prior year and down from a peak of $442 million in FY2023 [F1]. Operating income also decreased by nearly 16% to $41.5 million during this period, while net income contracted sharply by over 60% to $6.4 million—underscoring ongoing margin pressures despite scale advantages [F1].

Operating cash flow remained solidly positive at $64.3 million but declined by roughly 26% year-over-year, reflecting elevated operational costs amid challenging market conditions [F1]. Capital expenditures increased modestly to $46.8 million as CPH continues investing in maintaining its specialized equipment fleet [F1].

Historical Financial Performance:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 393 | 6 | 64 | 42 | -7.7% | -60.7% |

| 2024 | 426 | 16 | 87 | 49 | -3.7% | -49.0% |

| 2023 | 442 | 32 | 97 | 61 | +10.2% | +10.9% |

| 2022 | 401 | 29 | 77 | 50 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 14 | 18 | 2.4 |

| 2024 | 10 | 43 | 5.0 |

| 2023 | 11 | 42 | 10.3 |

| 2022 | 4 | -25 | 10.3 |

Source: SEC companyfacts cache [F1].

(Figures sourced from latest SEC filings; percentage changes calculated from absolute values)

Distinctive Market Positioning: National Fleet Scale and Customer Agreements

CPH benefits from being the only operator with a truly national footprint on both sides of the Atlantic Ocean [S6]. In the U.S., its Brundage-Bone brand operates roughly 1,000 specialized equipment units across nearly 95 locations spanning approximately 23 states [S5]. The U.K.’s Camfaud brand adds around 370 equipment units serving more than 35 locations mainly focusing on operated pumping services; Premier Concrete Pumping complements this with rental equipment offerings without operators .

The Eco-Pan business provides concrete waste management services across both markets, leveraging route density economics uncommon among smaller regional competitors—with approximately 150 trucks and over 12,000 specialized metal pans or containers deployed for construction washout containment systems . Unlike pumps billed on negotiated time-and-volume terms (including fuel surcharges), Eco-Pan’s revenue is primarily derived from fixed-fee route schedules encompassing delivery, pickup, compliant disposal, and specified rental durations; incremental fees apply for extended usage or irregular waste presence [S5].

The industry remains highly fragmented: most U.S.-based competitors operate fleets of only five to ten pumps each, with few having multi-regional reach; none rivals CPH’s scale or geographic breadth [S4]. Consequently, CPH typically competes with only one or two peers capable of executing larger commercial or infrastructure projects demanding advanced technical capabilities.

Customer metrics highlight contract stability: more than 16,000 customers have been served (often multiple projects per client), featuring an approximately 90% retention rate among top-500 customers—and effectively full retention within top-100 accounts—reflecting longstanding relationships averaging over two decades tenure for top ten clients who collectively contribute less than 10% of total revenue [S6].

The workforce comprises highly trained operators supported by experienced management averaging decades in the field; fleet assets average about eight years old—relatively young given typical pump equipment lifespans ranging from ten to twenty-five years [S6].

Financial Pressure Points: Margins, Cash Flows, and Profitability Challenges

Despite commanding an enviable market position by volume and geographic reach, recent financial trends reveal margin compression linked to cyclical impacts on construction demand combined with rising operating expenses.

Operating income declined to just over $41 million—a nearly sixteen percent drop year-over-year—while net income fell more than sixty percent compared with prior fiscal periods—impacted partly by elevated capital expenditure needs for fleet upkeep alongside cost inflation notably affecting fuel and labor inputs [F1], [N2], [N1], [S18].

Cash flow generation remains positive at $64 million annually but down markedly from prior peaks near $97 million due to slower collections timing and higher working capital consumption related to project phasing variability [F1]. Free cash flow (operating cash flow minus capex) narrowed to approximately $17 million in FY2025, limiting capacity for discretionary investments or aggressive capital returns.

Capital allocation reflects a measured approach: share repurchases totaled about $14 million during FY2025—a moderate increase versus prior years—highlighting cautious prioritization amid profitability headwinds alongside substantial recurring investments required for ongoing fleet maintenance estimated near $47 million annually [F1], [S18]. No dividends were declared according to public filings.

Return on equity remains subdued at roughly 2.4%, indicative of compressed earnings alongside increased equity balances following acquisition integrations yet to fully translate into higher net returns [F1]. Liquidity appears adequate; cash & equivalents stood near $53 million against current liabilities around $59 million at early calendar year-end data yielding a current ratio close to two—signaling manageable short-term obligations capacity currently [F1].

Growth Outlook Anchored by Cross-Border Synergies and Eco-Pan Expansion

Looking forward, CPH emphasizes leveraging its dual-market presence alongside growth within its higher-margin Eco-Pan concrete waste management segment that benefits from scalable route density advantages not easily replicated locally.

Recent earnings commentary outlines strategic plans focused on penetrating existing customers further through cross-selling Eco-Pan services while selectively expanding presence in profitable geographies where infrastructure-driven demand remains resilient despite overall cyclical softness [N1], [N2], [S6]. This targeted focus aligns well with CPH’s technical competencies relative to local smaller operators.

Potential expansion into residential markets offers additional upside but is approached cautiously given smaller project sizes and comparatively lower margins versus commercial endeavors.

Geographic flexibility constitutes a key competitive advantage—the sizeable fleets can be rapidly redeployed across markets aligned with localized construction activity surges—enabling optimized asset utilization critical amid cost pressures.

Capital Allocation Review: Balancing Reinvestments With Shareholder Returns

CPH manages a balance between reinvesting heavily into maintenance capital expenditures essential for sustaining specialized fleets—which are capital-intensive assets requiring continuous upkeep—and returning value primarily through share buybacks.

Capital spending rose slightly to just under $47 million annually reflecting ongoing replacements necessitated by aging equipment averages (~8 years old), contrasted against historically higher investment levels exceeding $100 million during earlier acquisition-driven fleet build-out phases now stabilized but still crucial for long-term reliability [F1].

Share repurchases totaled about $14 million during FY2025 representing measured capital returns consistent with cautious confidence amid prevailing margin challenges rather than aggressive distribution policies [F1], [S18]. No dividend payments have been declared.

Liquidity remains solid supported by cash holdings exceeding $53 million offsetting current liabilities below $60 million as of early CY2026 quarter-end providing financial flexibility while sustaining operational capacity through downturns without excessive leverage reliance ([F1], [S16], [S24]).

Operational Risks: Economic Cyclicality, Competitive Landscape, and Cybersecurity Governance

Key risks stem primarily from sensitivity to economic cycles affecting construction volumes especially within commercial/infrastructure sectors dominating revenues—a known source of volatility impacting equipment utilization rates and pricing power given a fragmented competitive environment featuring many small operators lacking capital depth or broad geographic reach ([S1],[S8],[S13]).

Additional risks include exposure to rising operating costs influenced by commodity price volatility—especially fuel—and supply chain disruptions impacting availability of specialized pump equipment sourced mainly from limited manufacturers ([S11],[S12]). Foreign trade policies including tariffs could indirectly escalate costs affecting customer demand patterns ([S11],[S12]).

Cybersecurity risk is managed via disciplined enterprise-wide frameworks aligned with National Institute of Standards and Technology (NIST) guidelines; governance includes dedicated IT security leadership reporting directly into the CFO supported by ongoing external assessments such as penetration testing plus comprehensive employee training programs addressing phishing threats ([S13]). These measures aim to minimize operational disruption or data breaches that could materially impact service delivery or reputation.

Key Milestones Ahead and What Investors Should Monitor

While explicit forward guidance remains limited beyond general strategic initiatives discussed during quarterly earnings calls ([N1],[N2],[N3]), investors should watch several key indicators:

- Stabilization or improvement in revenue trends reversing recent declines,

- Margin improvement potentially driven by cost controls or pricing leverage,

- Success expanding Eco-Pan’s geographic footprint alongside incremental cross-sales within existing customer bases,

- Efficient capital expenditure balancing reinvestment needs against free cash flow generation,

- Effective integration of acquisitions sustaining market share gains,

- Progress on cybersecurity resilience mitigating operational disruption risks.

These milestones will provide insight into whether Concrete Pumping Holdings can translate structural competitive advantages into sustained financial performance amid ongoing macroeconomic headwinds.

This analysis relies exclusively on publicly available information from SEC filings through early March 2026 ([F1],[S#]) together with contemporaneous earnings reports ([N#]). It does not constitute investment advice but aims to offer informed insights into Concrete Pumping Holdings’ operations within its specialized construction services niche.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments