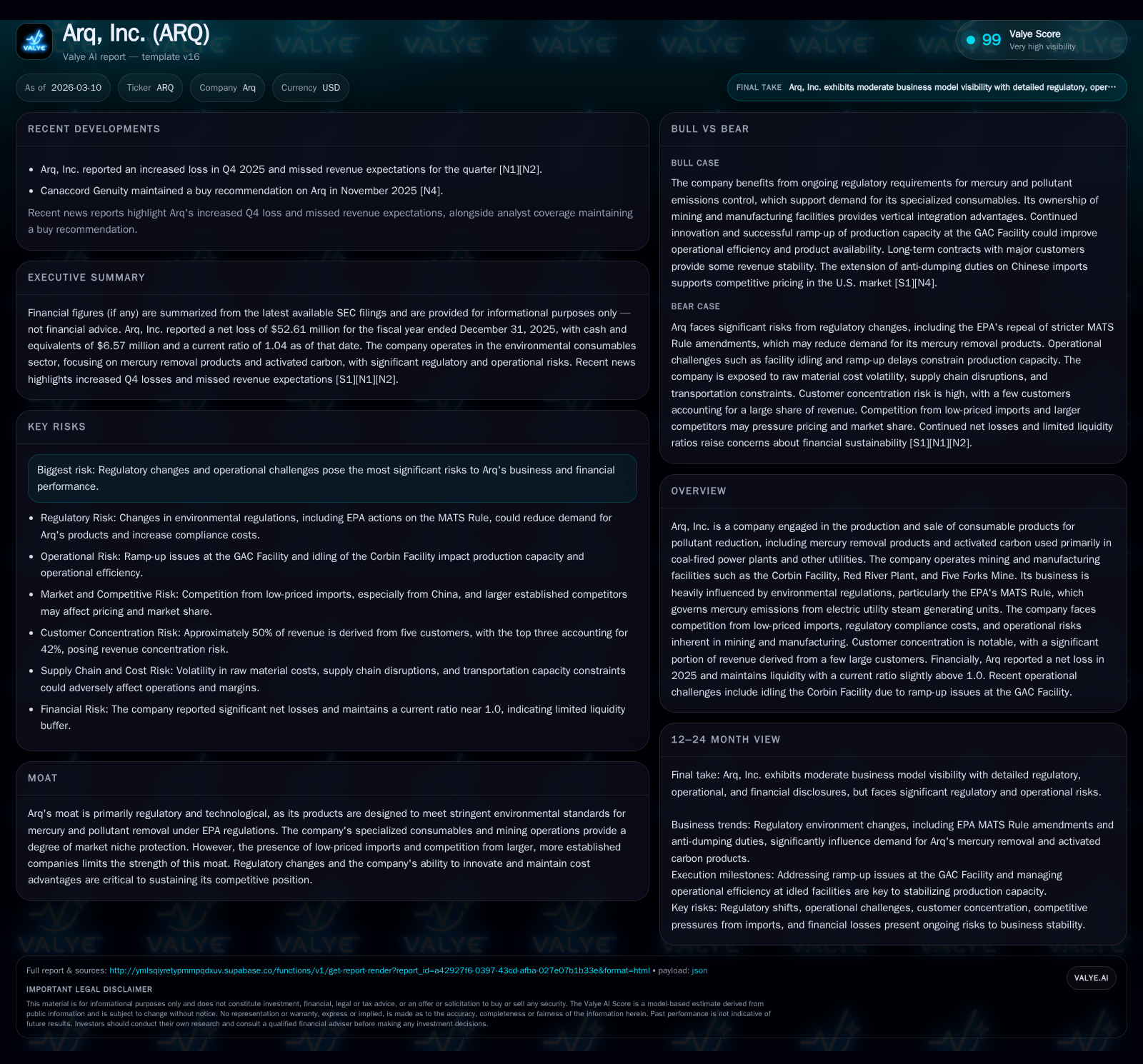

Arq, Inc. Confronts Product Ramp-Up Challenges and Regulatory Uncertainty Impacting Financial Health

Product design setbacks and evolving EPA regulations pressurize Arq’s operating performance and liquidity.

Arq, Inc. experienced significant operational hurdles in ramping up production of its granular activated carbon (GAC) products due to design flaws and feedstock challenges at its Red River Plant, resulting in halted production and increased costs in 2025. Regulatory shifts, including the EPA’s rollback of stricter mercury emission standards under the MATS Rule, pose demand risks for Arq’s core consumable products targeted at coal-fired power plants. Financially, the company reported a substantial net loss of over $52 million in 2025 and negative operating cash flow, despite a history of revenue growth through 2021. Liquidity remains supported by a revolving credit facility and cash on hand for now, but continued resolution of production setbacks and regulatory clarity are critical to shifting financial trends.

Historical Performance and Growth Drivers

Arq, Inc. has focused its business on manufacturing activated carbon (AC)-based consumables primarily aimed at pollutant reduction in coal-fired power generation units under stringent environmental controls. The company’s revenues demonstrated solid growth from $10.6 million in 2018 to nearly $25.8 million by 2021 ([F1]). This expansion was largely driven by increased EPA regulations such as the Mercury Air Toxics Standards (MATS) Rule which mandated pollution control technologies, fostering demand for Arq's mercury removal chemicals.

However, detailed revenue figures post-2021 are not available; operating income deteriorated sharply from losses of $12.1 million in 2022 reaching a steep negative $52.9 million by the end of 2025 ([F1]), underscoring mounting operational difficulties.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -53 | -3 | -53 | -929.8% |

| 2024 | -5 | 10 | -2 | +58.3% |

| 2023 | -12 | -17 | -13 | -37.4% |

| 2022 | -9 | -6 | -12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | ROE% |

|---|---|---|

| 2025 | -31.3 | |

| 2024 | -2.4 | |

| 2023 | 0 | -6.9 |

| 2022 | 45000 | -6.4 |

Source: SEC companyfacts cache [F1].

Financial figures post-2021 reveal severe profit contraction amidst operational disruptions.

Operational Setbacks: GAC Facility Challenges

Arq’s strategic thrust included scaling production of granular activated carbon at its Red River Plant’s newly commissioned GAC Facility which completed construction early in 2025 ([S1]). Initial commercial runs started that year but soon unveiled critical design flaws exacerbated by variability in the primary feedstock—Corbin Wetcake coal—leading to an inability to achieve nameplate production capacity without significant reengineering.

Consequently, in December 2025, the company halted GAC production entirely, idled the Corbin mining operation as a cost-saving measure, and initiated comprehensive engineering reviews targeting modifications to plant systems as well as adopting bituminous coal feedstocks deemed more consistent for product quality ([S1], [S15]). These disruptions heavily contributed to sharp losses and negative operating cash flow.

The technical obstacles underscore risks inherent in specialized purification technology manufacturing where feedstock quality impacts both operational efficiency and product compliance with environmental standards.

Regulatory Environment and Market Demand

Arq’s business is closely tied to EPA emissions regulations addressing mercury and other hazardous pollutants from coal- and oil-fired electric utility steam generating units (EGUs). The MATS Rule historically provided a regulatory underpinning mandating consumable product use for pollutant capture.

In February 2026, the EPA rescinded provisions from the April 2024 amendments to MATS that had tightened emission limits especially for lignite coal-fired EGUs ([S15]). This rollback returns emission standards to benchmarks set in 2012, potentially diminishing incremental demand growth for Arq’s mercury removal solutions given relaxed compliance requirements.

While regulation remains central to market size, any weakening or uncertainty around EPA standards poses direct downside volatility risk for Arq’s consumables niche.

Customer Concentration and Competitive Landscape

The company operates one reportable segment—advanced purification technologies—selling AC-based remediation products primarily within the U.S., with some sales into Canada ([S5], [S21]). Customer concentration is material; two largest customers accounted collectively for about one-third of total revenues recently ([S21]). This elevates counterparty risk should contract renewals falter.

Competition includes low-cost imports—particularly Chinese activated carbon—and larger incumbents with scale advantages ([S15]). Tariffs have not fully offset these pressures.

Capital Structure, Liquidity & Cash Flow

As of December 31, 2025, Arq carried approximately $28.7 million total debt comprising about $19 million outstanding under a secured revolving credit facility (with a $30 million limit) plus an amortizing CTB term loan of approximately $8.4 million related to mining assets ([S6], [S7], [S16]). Cash and equivalents stood near $6.57 million with current assets slightly exceeding current liabilities yielding a current ratio near 1.04 ([F1]).

Despite this liquidity buffer, operating cash flow turned negative at approximately -$2.7 million in FY25 compared with positive inflows previously due largely to increased net losses and working capital changes ([F1], [S18], [S20]). Capital expenditures planned for 2026 focus mainly on routine maintenance and potential GAC Facility modifications pending engineering reviews ([F1], [S12]).

The Revolving Credit Agreement contains covenants including maximum leverage ratios and minimum liquidity thresholds ($5 million minimum), requiring close monitoring amid ongoing losses ([S16], [S19]).

Returns and Capital Allocation Policies

Net losses precluded dividends or share repurchases during recent periods; the stock repurchase program was terminated in August 2025 leaving no ongoing buyback activity ([S13]). The company maintains a tax asset protection plan designed to safeguard net operating loss utilization against ownership change limitations under IRC Section 382 rules ([S13], [S17]).

Return on equity based on latest net income versus equity of roughly $168 million signals deep negative levels at approximately -31%, reflecting sustained unprofitability ([F1]).

Outlook & Factors To Watch

The near-term outlook hinges largely on resolving GAC Facility bottlenecks via successful engineering redesigns enabling capacity ramp-up using improved feedstocks alongside maintaining necessary regulatory licenses ([S1], [S12]).

Market demand will continue shaped by regulatory trajectories: stabilization or tightening of EPA hazardous air pollutant emission requirements would sustain mercury product necessity whereas further weakening could compress volumes ([S15]).

Liquidity management remains vital given limited borrowing capacity (approximately $1.4 million available under credit line), ongoing operating losses, yet relatively moderate maintenance capex commitments ([S14], [S20]).

Monitoring customer contract renewals within concentrated accounts alongside competitive pressures particularly from imports will also influence revenue stability ([S21], [N2]).

Risks include legal proceedings linked to claims against engineering contractors over project delays adding complexity given potential cost exposures but reflecting management efforts at recouping damages ([S19]).

Given these headwinds combined with innovation demands typical in specialized environmental technology consumables markets, Arq must bridge operational gaps efficiently while sustaining regulatory alignment.

This memorandum synthesizes filings through March 10, 2026; it does not constitute investment advice but aims for analytical clarity based on publicly disclosed data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments