Stifel Financial Corp Secures $1B Credit Facility While Sustaining Solid Growth and Capital Returns

Stifel's expanded liquidity and ongoing stock split underscore its financial stability amid evolving market dynamics.

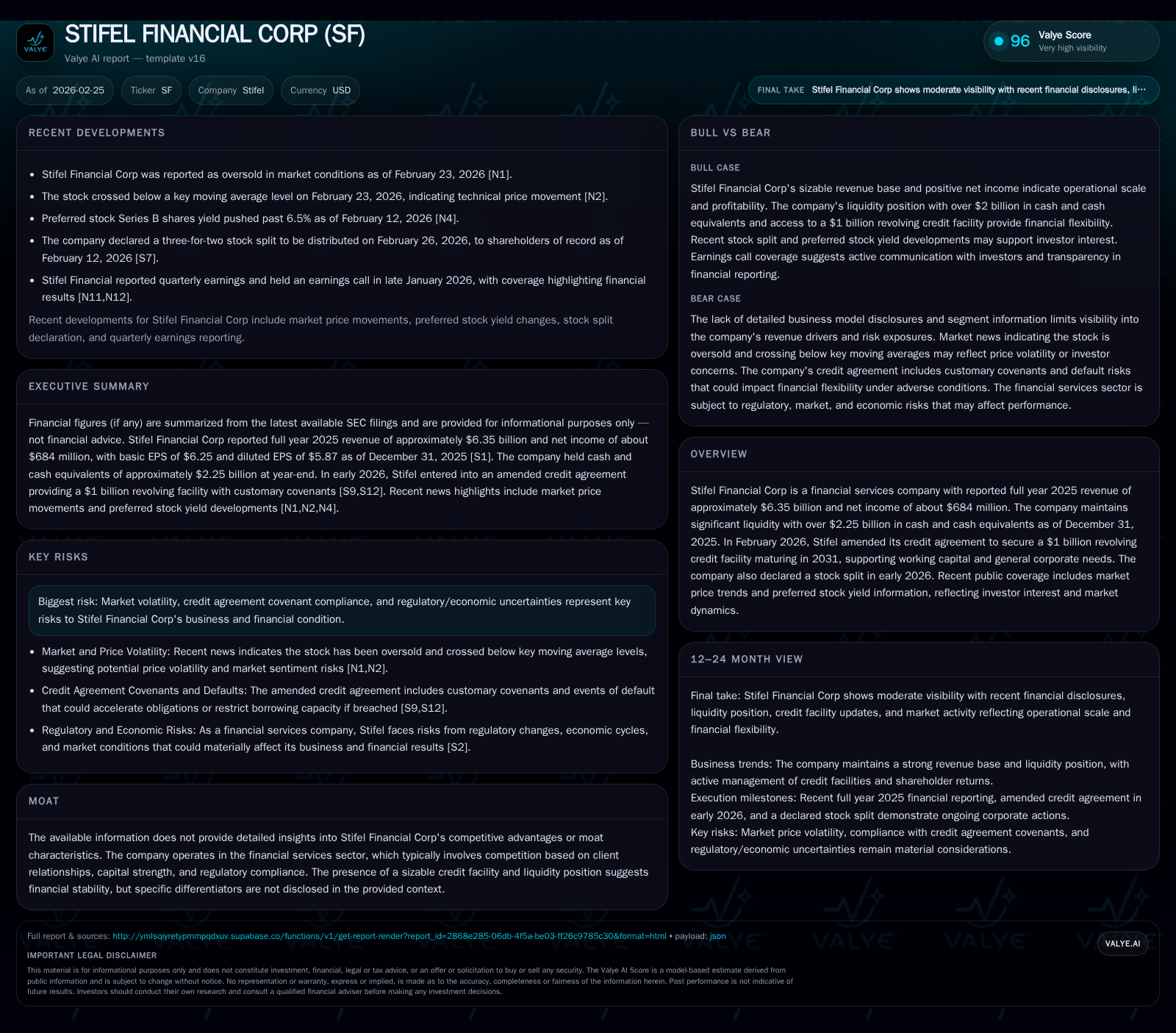

Stifel Financial Corp reported steady revenue growth reaching $6.35 billion in 2025, driven by diversified financial services amidst a competitive landscape. The company strengthened liquidity by amending a $1 billion revolving credit facility maturing in 2031, signaling confidence in capital flexibility. Despite a modest net income decline and fluctuating operating income dynamics, Stifel continues disciplined capital allocation highlighted by increasing buybacks and dividend distributions alongside a recent 3-for-2 stock split. Market and regulatory risks remain active considerations for the firm's trajectory.

Historical Financial Performance

Stifel Financial Corp's revenue has demonstrated consistent expansion over recent years, culminating at roughly $6.35 billion for FY2025, up from approximately $5.95 billion in FY2024—a year-over-year increase of about 6.7% [F1]. This growth trajectory follows earlier years marked by steady gains: $5.16 billion in 2023 and $4.59 billion in 2022. The company’s ability to scale revenues suggests effectiveness in client acquisition and service diversification within the financial services segment.

Net income trends reflect some variability; the firm posted $683.8 million for FY2025, down about 6.5% from the prior year's peak of $731.4 million [F1]. This dip could be attributed to elevated expenses or lower operating margins potentially influenced by a more cautious investment climate or rising costs of capital-related activities.

Operating cash flow illustrates marked improvement, especially notable is the leap from approximately $490 million in FY2024 to over $1.11 billion in FY2025 [F1]. With capital expenditures decreasing moderately to around $62 million (versus prior years averaging nearer to $70–80 million), Stifel converted these efficiencies into strong free cash flow exceeding $1 billion annually—an important metric signifying internal financial health and funding capacity.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 6.3 | 684 | 1117 | 62 | +6.7% | -6.5% |

| 2024 | 6.0 | 731 | 490 | 74 | +15.4% | +40.0% |

| 2023 | 5.2 | 523 | 499 | 52 | +12.3% | -21.1% |

| 2022 | 4.6 | 662 | 1157 | 82 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Div, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 245 | 1055 |

| 2024 | 144 | 417 |

| 2023 | 444 | 447 |

| 2022 | 106 | 1075 |

Source: SEC companyfacts cache [F1].

Dividends paid data not available for recent years; buybacks consistently increased up through FY25 suggesting strategic share repurchase activity.

Recent Corporate Developments and Liquidity Management

In early February of 2026, Stifel amended its credit agreement expanding its revolving credit facility to $1 billion with a maturity extending to February 2031 [S7][S10][S11]. This unsecured revolving facility replaces prior commitments and provides vital flexibility for working capital requirements and general corporate purposes.

The facility carries variable interest rates based on the Secured Overnight Financing Rate (SOFR), integrating modern benchmark interest rate systems post-LIBOR transition—a relevant detail for treasury management professionals assessing interest rate risk mitigation strategies.

Loan covenants include maintaining minimum consolidated tangible net worth thresholds along with regulatory excess net capital ratios applicable especially to Stifel Nicolaus & Company subsidiaries—reflecting prudent balance sheet oversight mandated by banking and securities regulations [S7][S10]. These restrictive covenants ensure that Stifel preserves solid capitalization metrics even while drawing on available credit lines.

Additionally, on January 26, 2026, the Board approved a three-for-two stock split executed as a 50% stock dividend effective late February—which typically aims to improve trading liquidity and attract retail investor interest without altering fundamental value per share [S9][N1].

Growth Prospects and Constraints

Looking forward, Stifel's growth could be propelled through several avenues evidenced by company commentary during earnings calls [N1][N2] including expanding wealth management services amid rising client asset inflows and strengthening institutional brokerage operations benefiting from market recovery phases.

However, certain factors may limit upside potential: the sensitivity of margins to market volatility affecting transaction volumes, regulatory scrutiny increasing compliance costs—as noted risks—and macroeconomic uncertainties impacting client investment behaviors all pose challenges documented within SEC risk disclosures [S4][S8].

Moreover, maintaining credit covenant compliance under variable economic conditions is essential given that covenant breach risks could trigger facility acceleration or capital structure stress points [S7][S10].

Returns and Capital Allocation Discipline

Capital deployment illustrates a balanced approach: while buyback spend rose appreciably to nearly quarter-billion dollars in FY25 from prior levels (up from $144 million in FY24), dividends have been consistent though specific recent payout amounts are not disclosed publicly [F1][S13]. Operating cash flows comfortably cover these uses after accounting for capex.

Approximate return on equity based on reported net income relative to shareholders’ equity (last available at ~$4.25 billion end-2020 but assumed growing since then) is roughly calculated at about 16% for FY25—a healthy figure reflective of profitable operations despite net income fluctuations [F1].

Such returns are consistent with norms seen among diversified financial services firms that blend transactional revenues with asset management fees, where capital efficiency is critical given intense regulatory capital requirements.

Market Positioning Amid Sector Dynamics

Although detailed moat characteristics are not explicitly disclosed, Stifel’s sizable cash reserves exceeding $2.25 billion as of year-end support operational resilience amidst episodic equity market pullbacks or credit environment tightening [F1][N1]. This liquidity buffer enables opportunistic investments or acquisitions if market disruptions arise.

In addition, preferred stock series maintaining yields above ~6.5% may attract fixed-income oriented investors seeking stable income streams—increasing investor base diversification amid broader capital market fluctuations [N7][N13].

Competition within brokerage and investment banking remains fierce; however, successful navigation of credit markets with prudent covenant designs combined with proactive shareholder relations via stock splits signal strong governance fundamentals.

What To Watch Next (Analysis)

Absent explicit forward guidance from filings or press releases beyond public earnings discussions [N2], attention should focus on:

- Quarterly revenue composition shifts between wealth management vs institutional segments,

- Compliance updates concerning amended credit agreements,

- Trends in share repurchases versus dividend payments,

- Any changes in regulatory environment impacting capital adequacy,

- Market conditions influencing transaction volumes affecting operating income quality,

- Execution details regarding client acquisition costs relative to rising competition.

Monitoring management commentary on these vectors will provide clarity on whether current momentum sustains or if challenges require strategic recalibration.

This analysis aims solely at providing an informative examination of company performance indicators combined with contextual industry insights based on publicly accessible financial statements and news items as of February 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments