RYTHM, Inc.'s Transition from Extraction to Brand Licensing: Assessing Growth and Risks

RYTHM shifted focus from extraction technology to licensing a portfolio of hemp-derived THC brands, reshaping its revenue base and risk profile.

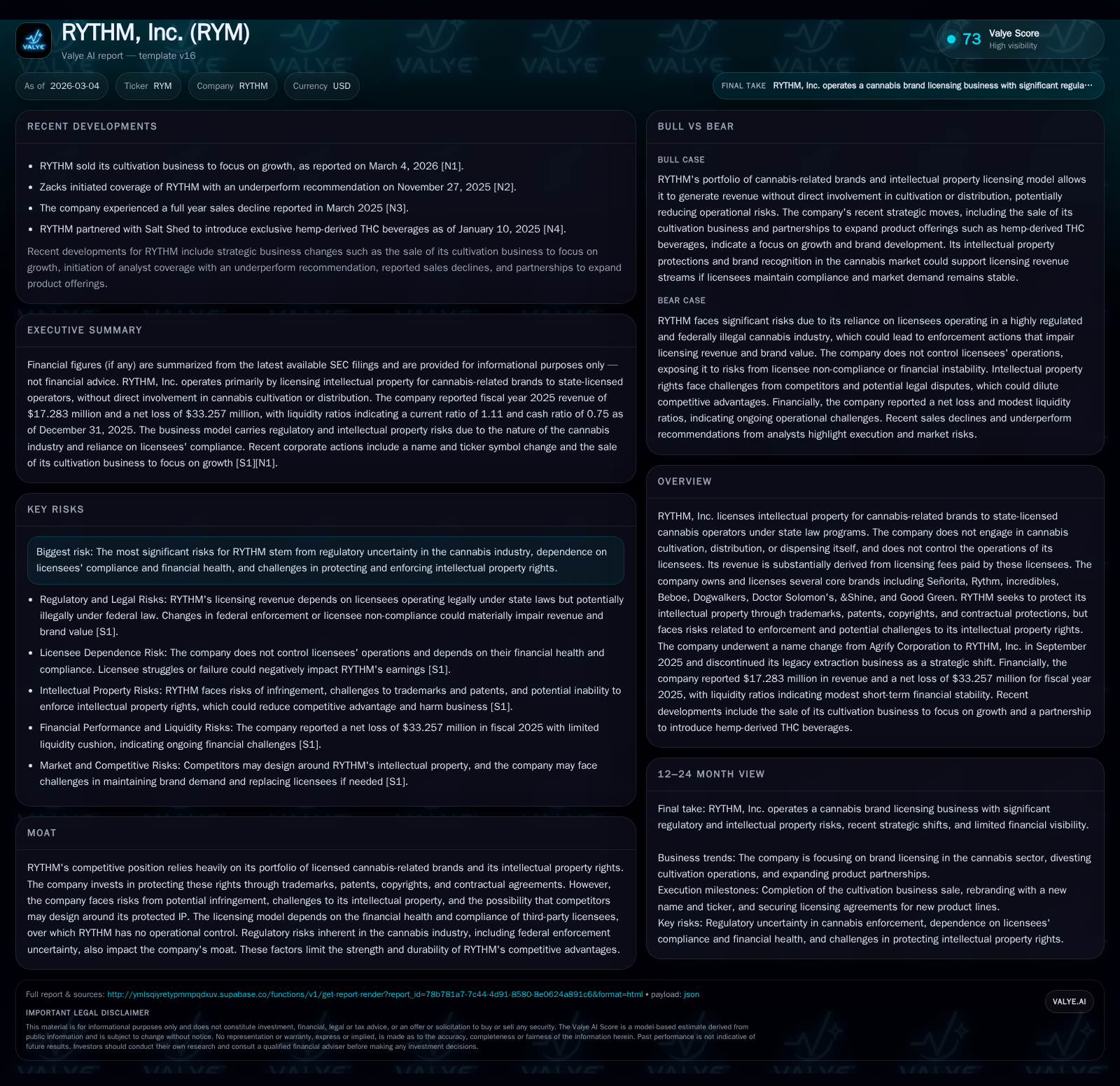

RYTHM, Inc., formerly Agrify Corporation, completed a significant strategic pivot in 2025 by exiting its legacy cannabis extraction business and rebranding to focus exclusively on licensing intellectual property for hemp-derived THC products. This transition drove a near doubling in revenue in 2025 compared to 2024, fueled primarily by brand licensing fees from established cannabis operators. However, ongoing federal regulatory uncertainty and licensee compliance risks temper near-term growth prospects. The company continues to absorb operating losses and negative free cash flow, reflecting costs associated with maintaining and defending its intellectual property portfolio amid a contested cannabis legal framework.

Evolution of RYTHM’s Business Model: From Extraction to Brand Licensing

RYTHM, Inc.’s transformation is anchored in its strategic divestment of its legacy extraction business and renaming from Agrify Corporation effective September 2, 2025 [S1][N1]. Historically known for providing extraction and cultivation equipment—capital-intensive segments within cannabis production—the company has repurposed itself as a pure-play licensor of intellectual property (IP) surrounding hemp-derived tetrahydrocannabinol (THC) consumer brands. This pivot reflects a deliberate retreat from asset-heavy operations toward leveraging intangible assets tied to branded product lines such as Señorita, incredibles, Beboe, Dogwalkers, Doctor Solomon’s, &Shine, and Good Green [S1].

The shift reinforces RYTHM’s reliance on licensing fees paid by state-licensed cannabis operators who manufacture and distribute products under these well-recognized brands. The rationale centers on reducing capital expenditures associated with manufacturing hardware while focusing resources on protecting and monetizing the IP portfolio through trademarks, patents, copyrights, and binding contractual arrangements—a structural strategy designed for scalability absent direct operational control [N1][S1].

Historical Financial Performance and Growth Drivers Through 2025

Following the exit of the Extraction Business in March 2025—a move accounted for retrospectively as discontinued operations—RYTHM’s financial profile reveals significant volatility but signs of top-line recovery. Revenue declined steeply after FY2022's $58.3 million peak reflecting legacy hardware sales but recovered notably to $17.3 million in FY2025 from only $9.7 million in FY2024—a 78.5% year-over-year increase driven predominantly by licensing fee revenue growth [F1].

Despite improving revenue figures, operating income remains substantially negative at -$32.3 million for FY2025 (worsening by over 200% from the prior year’s -$10.2 million), attributable to ongoing investments in IP protection infrastructure and scaling brand licensing activities [F1]. The net loss narrowed compared to extremely deep deficits recorded through FY2023 and FY2022 yet remains sizable at -$33.3 million [F1]. Operating cash flows continue trending negative (-$23.5 million in FY2025), though the steep falloff in capital expenditure—from $8.13 million in FY2022 down to only $4 thousand USD post-exit—indicates a successful shedding of capital-intensive operations [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17 | -33 | -24 | -32 | +78.5% | +20.3% |

| 2024 | 10 | -42 | -12 | -10 | -42.6% | -123.9% |

| 2023 | 17 | -19 | -31 | -19 | -71.0% | +90.1% |

| 2022 | 58 | -188 | -72 | -193 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | -255.4 |

| 2024 | -12 | -149.8 |

| 2023 | -31 | 124.8 |

| 2022 | -80 | 2029.5 |

Source: SEC companyfacts cache [F1].

Table reflects annual data through FY2025 showing recovery in revenue post-extraction exit with continuing operating losses.

Licensing Revenue Dynamics and Dependence on Licensees’ Compliance

RYTHM generates most earnings via licensing fees paid by third-party cannabis operators authorized under various state programs [S1][S2][N1]. Key licenses involve notable consumer brands including Señorita—known for hemp-derived THC cocktail-inspired beverages—and incredibles edibles primarily distributed through online channels and select retail partners [S1]. Through trademark and recipe license agreements (e.g., with Green Thumb Industries subsidiaries), RYTHM cedes manufacturing responsibility while retaining contractual rights tied to usage of its intellectual property [S16].

However this model depends heavily on licensees’ continued financial health and regulatory compliance; these licensees operate independently without RYTHM's operational control [S2][S6]. Financial struggles or regulatory non-compliance among licensees could disrupt royalty streams or impair brand reputation if quality standards slip [S6]. While RYTHM enforces contracts against misuse or infringement when feasible [S4][S9], it cannot guarantee licensee adherence or control their business conduct.

Regulatory Headwinds Shaping Market Access for Hemp-derived THC Products

The legality underpinning RYTHM’s licensed products faces federal regulatory uncertainty [S1][S4]. The landmark 2018 Farm Bill legalized hemp defined as Cannabis Sativa L. containing less than 0.3% delta-9-THC; however a provision enacted within the 2026 Appropriations Act (Section 781) threatens to amend this definition effectively prohibiting many hemp-derived THC products currently commercialized—including those licensed by RYTHM—effective November 12, 2026 unless legislative action occurs [S1].

This creates acute uncertainty for market access both federally and across states where regulations vary widely—from bans to restrictive frameworks involving labeling or potency limits [S1]. The FDA has not approved THC-containing ingestible consumables under the Federal Food Drug & Cosmetic Act interpretations adding another layer of complexity [S1]. Any adverse regulatory changes could materially curtail RYTHM’s licensing revenues.

Intellectual Property Protections: Fortifying the Moat Amid Risks

RYTHM relies on a robust intellectual property portfolio including trademarks covering key brands such as Señorita and incredibles alongside patents related to formulations or production methods [S9]. These rights are protected through U.S.-based laws supplemented by nondisclosure agreements embedded within licensing contracts ensuring confidentiality around recipes and branding [S4][S9].

Nonetheless enforcement involves costs that may divert management attention; trademark registrations face opposition risk; courts might narrowly interpret patent claims; competitors could design around protections [S4][S5][S9]. Thus while IP ownership is central to RYTHM's moat in a branded cannabis market segment valuing name recognition plus quality perception—the durability of this advantage depends on effective enforcement amid evolving challenges.

Capital Structure and Cash Flows Reflect Transition Phase Priorities

At December 31st 2025 snapshot levels show $32.2 million cash & equivalents alongside total current assets of approximately $47.6 million slightly exceeding current liabilities of $42.9 million yielding a current ratio near 1.11—indicative of balanced short-term liquidity management amid ongoing operating deficits [F1][S25]. Equity stands modestly positive at $13 million after recovering from highly negative positions recorded years prior reflecting legacy losses alongside restructuring efforts [F1].

Free cash flow remains negative by roughly $23.5 million primarily due to operational expenses related to IP maintenance despite minimal capital expenditures (~$4K) post-extraction exit confirming disciplined spending aligned with the new low-capital model focus [F1][S12][S18]. No dividends or share repurchases have been declared recently consistent with preservation priorities during turnaround phase [F1][S12]. Convertible notes issued mostly to related parties impose leverage considerations requiring prudent balance sheet management ahead of maturities approaching early 2027 [S10][S11].

Return metrics remain adverse with approximate ROE near negative -255%, underscoring ongoing profitability challenges despite top-line improvement indicative more of residual restructuring impacts than sustainable margins generation presently [F1].

Outlook: Navigating Regulatory Uncertainty Amid Licensing Growth Prospects

Looking forward into mid-2026 the impending Farm Bill amendment deadline presents pivotal uncertainty impacting RYTHM’s core licensed hemp-derived THC product lines regardless of state-level variances or potential federal repeal/delay efforts as disclosed by management [N1][S1][S2]. Legislative developments around Section 781 will be critical for continuity.

Important performance indicators include:

- Licensee financial health affecting royalty payment reliability;

- Effectiveness of contractual enforcement safeguarding IP revenues;

- Litigation outcomes influencing cost structure or IP defensibility;

- Quarterly cash flow trends signaling stabilization or further burn;

- Pipeline progress regarding new license agreements validating brand traction.

These factors frame an environment where licensing revenue momentum must contend with complex regulatory constraints plus execution risks within largely federally illegal state-regulated cannabis sectors posing material sustainability questions beyond pure financial metrics.

This analysis synthesizes publicly filed SEC documents along with recent news releases related strictly to RYTHM Inc.’s reported facts up to early March 2026 without speculative forward-looking assertions beyond company disclosed information or verifiable statistics per provided sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments