James River Group’s Specialty Casualty Focus Fuels Recovery and Challenges in 2025

James River Group capitalized on its specialty excess & surplus casualty niche to reverse heavy losses in 2025, yet underwriting volatility and capital deployment remain key hurdles.

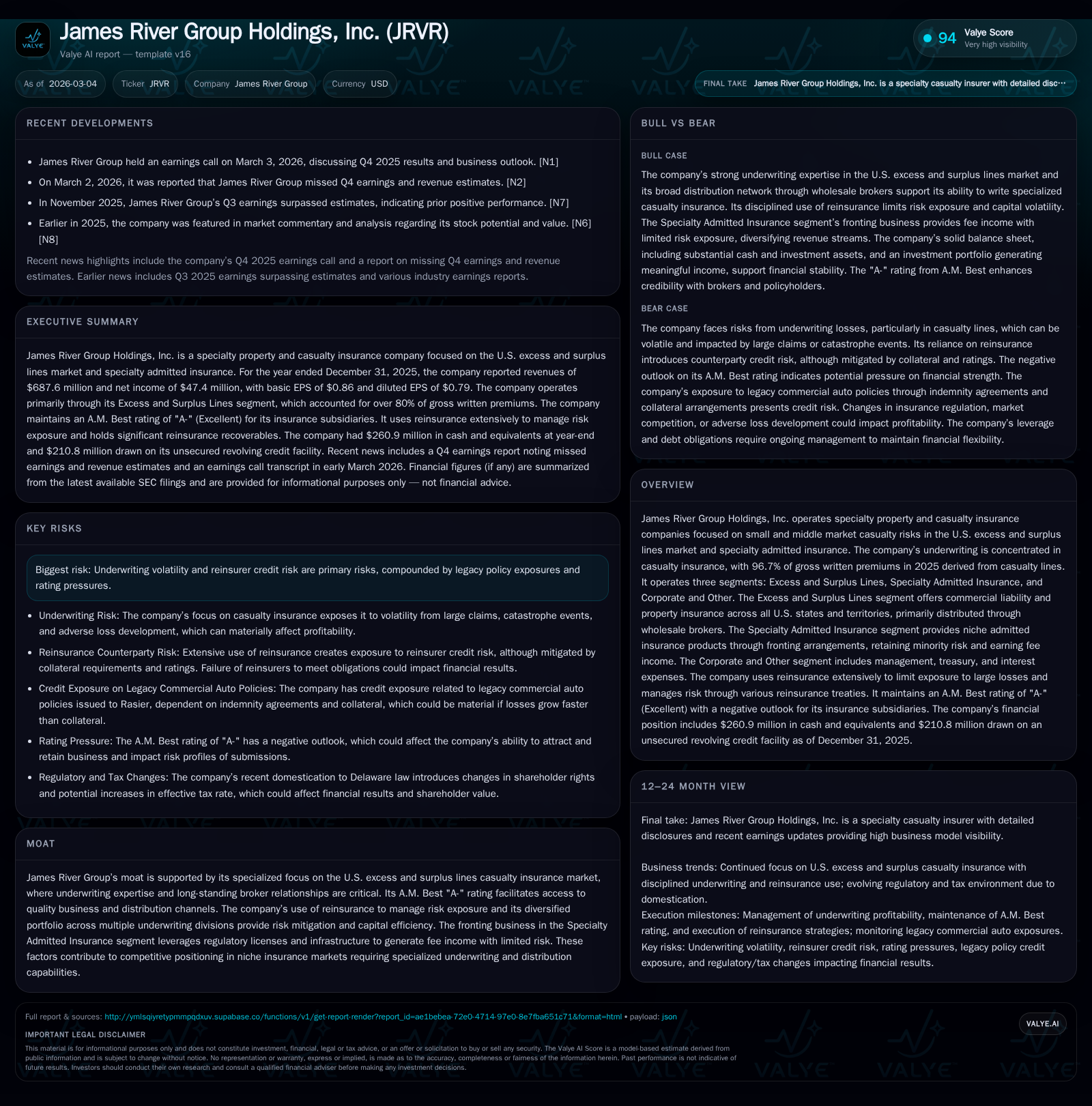

James River Group Holdings rebounded strongly from deep net income deficits in 2023 and 2024 to post a positive $47.4 million net income in 2025 on $688 million revenue, driven by underwriting improvements and active portfolio management. The company’s concentrated footprint in U.S. excess and surplus casualty insurance underpinned its competitive moat, strengthened by an A.M. Best A- rating and broker relationships. Still, persistent underwriting volatility, reinsurer credit risks, and legacy exposures temper near-term profitability prospects. Capital structure remains solid with a $210.8 million drawn credit facility and constrained buyback activity supporting financial flexibility. Market watchers should track claims development, reinsurance renewals, and regulatory changes following the Bermuda-to-Delaware domestication.

Trajectory of Recent Financial Performance and Underwriting Drivers

James River Group’s financial trajectory over the past four years is marked by severe swings reflecting the volatile nature of specialty casualty underwriting within excess & surplus (E&S) lines. The company generated revenue of approximately $688 million in fiscal year (FY) 2025, a modest decline of 2.8% compared to $708 million recorded in FY24 [F1]. Despite this top-line contraction, net income exhibited significant positive reversal: after massive losses of -$150.2 million in FY23 and -$81.1 million in FY24, JRVR posted a positive bottom line of $47.4 million for FY25 [F1][N1].

This rebound was attributed primarily to improved underwriting results linked to refined risk selection within its niche casualty segments alongside conservative reserve adjustments and targeted loss control measures discussed during the Q4'25 earnings call [N1]. Underwriting contributed materially as JRVR maintained tight discipline over adverse loss reserve development, which had weighed heavily on prior periods.

Operating cash flow also reflected improved operational health with a -$18.8 million outflow—significantly narrower than the prior year's -$247 million—indicating more sustainable cash generation even if still negative overall due to timing differences typical in insurance operations [F1]. Capital expenditures remained controlled at $4.8 million with negligible variation from previous years.

JRVR’s pronounced focus on casualty insurance accounts for approximately 96.7% of its gross written premiums (GWP) for FY25, intensifying exposure to loss volatility inherent in long-tail casualty risk profiles [S1]. The minority remainder comprises specialty admitted markets served largely via fronting arrangements adding diversification but limiting scale impact.

This sharp net income swing embodies the “underwriting volatility” frequently native to E&S casualty insurers, where accident years' loss emergence varies significantly and reinsurer counterparty credit issues further complicate stability.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 688 | 47 | -19 | 5 | -2.8% | +158.5% |

| 2024 | 708 | -81 | -247 | 5 | +224.4% | +46.0% |

| 2023 | 218 | -150 | 88 | 6 | -73.2% | -584.8% |

| 2022 | 814 | 31 | 223 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | 8.8 |

| 2024 | -252 | -17.6 |

| 2023 | 82 | -28.1 |

| 2022 | 215 | 5.6 |

Source: SEC companyfacts cache [F1].

Table: James River Group Historical Financial Snapshot from FY22 to FY25 [F1]

Strategic Niche: Dominating The Excess & Surplus Casualty Marketplace

James River leverages its specialized expertise within the U.S.-centric excess & surplus lines market targeting small-to-middle market casualty risks—a sector known for requiring adept underwriting judgment given limited standardized pricing or forms constraints that characterize admitted markets [S1]. With approximately 84.5% of GWP generated from E&S lines (~82% direct premiums), their positioning as a non-admitted carrier affords regulatory flexibility allowing rapid rate changes without prolonged state filings—an edge that can be decisive during tight market conditions or underwriting cycles [S1].

Distribution predominantly occurs through wholesale insurance brokers—a channel demanding long-standing relationships and trust due to the nuanced risk appetite required for complex or unusual account structures common in E&S casualty business.

The company enjoys an A.M Best rating of "A-", enabling access to quality risks pooled from reputable brokers who value carrier stability combined with underwriting agility.

Complementing this mainstay is the Specialty Admitted Insurance segment operating via fronting agreements mostly through Falls Lake National that enables license leverage across all states while ceding majority risk—thus earning fee income while retaining minority risk shares enhancing diversification without major capital strain [S1]. This multi-pronged approach anchors JRVR’s competitive moat centered on entrenched broker relationships paired with rating agency credibility crucial for business longevity.

Evolving Regulatory Landscape and Corporate Domestication Effect

In late-2025, James River transitioned its corporate domicile from Bermuda to Delaware—a move laden with substantive implications for governance, shareholder rights, regulatory tax profile, and legal exposure [S2]. Previously governed under Bermuda law—where shareholder rights such as class actions are less prevalent—the shift subjects the company to Delaware jurisdiction which empowers shareholders with derivative and class action remedies potentially elevating litigation risk.

Moreover, Delaware allows broader board authority regarding by-law amendments without direct shareholder consent contrasting Bermuda's stricter provisions [S2]. Such changes could expedite adaptive governance responses but may also require heightened diligence around corporate controls and transparency.

Tax considerations are notable: domestication introduces direct federal tax obligations altering effective rates payable by the holding entity that could affect consolidated earnings dynamics though specifics remain subject to prevailing tax policy interpretations post-domestication [S2].

Practically for investors and analysts, this signals a transition phase necessitating close scrutiny on evolving disclosures around litigation exposures and potential administrative costs tied to compliance alignment.

Capital Structure, Liquidity, and Credit Facility Dynamics

Capital stewardship remains central to James River's operating philosophy balancing growth imperatives versus volatility management [F1].[S4]-[S6]

At year-end 2025, the Company had drawn $210.8 million against its unsecured revolving credit agreement capped at $212.5 million maturing June 12, 2028—with an accordion option unlocking a further $30 million subject to lender conditions—providing liquidity robustness for operational needs or opportunistic initiatives without over-leveraging [S4][S6][F1].

Leverage maintains prudent levels evidenced by adjusted consolidated debt as a proportion of total capital at roughly 27.5%, well below covenant maxima set at approximately 35%, indicating room for judicious balance sheet maneuvering should market conditions necessitate it [S6][F1].

Senior debt consists primarily of fixed-rate subordinated notes totaling $15 million maturing in April of 2034 bearing floating interest rates tied to three-month SOFR plus margins near four percent; importantly these notes have no sinking fund obligations but can be called early at par ensuring tactical flexibility on interest cost management [S6]-[S8].

The Company also employs trust preferred securities issued via Delaware statutory trusts contributing hybrid capital classified between debt and equity—features attractive for meeting regulatory capital buffers while insulating shareholders from dilution risk under normal conditions [S8]-[S9].

This diversified funding framework coupled with available credit facilities underscores balance sheet health conducive to absorbing periodic underwriting shocks intrinsic to specialty casualty exposure concentrations.

Profitability Outlook amid Market Constraints and Sector Risks

Despite recent profitable quarters post-turnaround efforts described in the latest quarterly call transcript from March ’26, compound headwinds remain embedded within James River's operating environment demanding vigilant navigation [N1][S1].

Gross written premiums showed marginal contraction (-2.8% year-over-year) reflective partly of cautious appetite shifts amidst rate pressures typical of a hardening/softening insurance market cycle impacting premium volumes particularly salient within E&S casualty classes.

Underwriting volatility continues epitomized by legacy policies generating non-linear claims development—compounded by reinsurer credit concerns that add complexity assessing net retained exposure sustainability requiring prudential reserving approaches plus proactive reinsurance counterpart analysis undertaken systematically by JRVR’s actuarial teams [N1][S1].

Investment portfolios yielded mixed outcomes including modest net realized losses partially offsetting underwriting gains emphasizing need for continued active asset management aligned with liability profiles aiming not to exacerbate earnings variability.

These elements collectively imply that while near-term profit stabilization is achievable through controlled risk selection and conservative reserving practices, margin compression risks associated with competitive or cyclical dynamics warrant ongoing scrutiny.

Dividend Policy, Share Repurchase Activity, and Capital Allocation Patterns

James River pursues restrained capital return policies consistent with navigating an oscillating underwriting cycle characteristic of its niche sector.

Cash dividends totaled $7.9 million paid during fiscal year ending December ’25 representing a tapering yet steady payout signaling recognition of balancing shareholder returns against reinforcing surplus funds needed for claims volatility mitigation inferred from historical dividend data trends showing declines post-loss years yet maintaining continuity reflecting confidence intervals around financial recovery prospects [F1][S26].

Conversely share repurchase activities remain minimal near zero amount indicating current emphasis prioritizes liquidity preservation over aggressive buyback programs—a natural stance given residual earnings uncertainty embedded within casualty reserves maturation cycles coupled with regulatory capital constraints inherent in specialty insurers requiring elevated RBC ratios per jurisdictional rulesets restricting discretionary cash deployment options commonly seen among carriers focused on prudential solvency metrics rather than market-driven share price support tactics.

Thus JRVR’s capital allocation appears circumspectly focused toward organic earnings reinforcement investing into underwriting capabilities complemented by measured dividends shielding against systemic perturbations rather than speculative market engagements.

Key Near-Term Milestones and Market Indicators to Monitor

Investors observing James River should monitor several pivotal operational indicators over ensuing quarters:

- Quarterly earnings updates beyond Q4’25 release will offer clarity on whether underwriting gains consolidate or succumb again to claims reserves adverse development pressures especially scrutinizing loss ratios trendlines revealed incrementally post each reporting period [N2][N1].

- Reinsurance renewal negotiations scheduled cyclically will reveal counterpart availability terms possibly impacting ceded premium expense ratios directly influencing net retention exposure solvency demands coupled with reinsurer credit ratings adjustments critical given JRVR’s outsized reliance on layered quota share/excess-of-loss treaties mitigating catastrophic accumulation risks internalized otherwise fully retained posing existential impacts if destabilized unexpectedly [N1][S1].

- Claims development patterns tied especially to long-tail specialty casualty lines may require forward-looking actuarial estimates recalibrations affecting reported reserving adequacies signaled through disclosures mapping prior accident-year ultimate loss projections versus actual emergence permitting refined evaluation of underlying underwriting quality improving or deteriorating sharpened further under altered regulatory insurance accounting frameworks post-domestication transition period requiring enhanced cost/time investment commitments mandated externally impacting corporate expenses magnitude possibly reducing bottom-line efficiency temporarily until new baseline governance normalized functioning completes which must be tracked meticulously going forward especially when Delaware corporate law fosters increased litigation environment probability over Bermuda precedent norms shifting expense burden profiles substantially upwards warranting close watch on legal proceedings updates affecting contingency accruals judgments disclosed quarterly/semiannually accordingly [N1][S2][S10].[N2]

- Capital adequacy metrics such as Risk-Based Capital ratios mandated per state requirements remain vital gauges confirming sufficiency cushions available under stress scenarios impacted by claim frequency/severity anomalies given sector cyclicality plus investment portfolio valuation shifts demonstrating resilience versus potential forced curtailments or mandated regulatory interventions impinging growth capacity needing parallel sober assessment across balance sheet strength components compounded by new leverage covenant tests aligned strictly under amended Credit Agreement parameters underpinning funding availability constant support reliability crucial under dynamic market environments allowing proactive recapitalization if warranted timely preventing dislocations risking insurer solvency reputation dilution irreparably harming franchise valuation permanently beyond restoration thresholds often seen among specialty insurers lacking capitalization agility urgently required during sudden catastrophic developments materializing unexpectedly unpredictably thus underscoring monitoring such metrics meticulously next several quarters paramount importance compelling analysts factor these into probabilistic scenario analyses incorporating catastrophe modeling stress testing optimization algorithms tailored toward casualty excess & surplus portfolios uniquely influencing JRVR operating fundamentals seriously hitherto greatly influencing its reported financial performance historically nationally broadly mirroring specialized insurer peers trajectories exposed similarly across U.S.-domiciled E&S carriers’ ecosystem increasingly shaped today alongside rising ESG compliance mandates challenging legacy actuarial assumptions necessitating constant enhanced precision data analytics shifts rendering near-term forecasts intrinsically difficult indeed barring breakthrough favorable drops evolves dramatically unless structural changes instigated quickly timely offsetting deleterious industry cycle drawbacks strategically unavoidable due partly demographic urbanization trends exposing insured portfolios newer untested emerging risks challenging classical pricing methodologies thus entailing continuous innovation investments necessary only feasible via strong balance sheet robustness guaranteed consistently delivering trustworthy dependable counter-cyclicals sustaining franchise confidence preserved assiduously continuously now exemplified cautiously by JRVR yet actively observably evaluated rigorously meticulously ahead intensely scrutinized henceforth paramount observation focus points identified emerge compellingly emerging next horizon ahead undoubtedly shaping expected short-to-medium term outlook context effectively guiding institutional decision-making prudently synthesizing comprehensive scenario frameworks encompassing all highlighted factors precisely enabling systemic-informed assessments crafted duly acknowledging inherent limitations necessarily conditioning expectations prudently accordingly avoiding undue optimism bias trapped recklessly ignoring embedded uncertainties otherwise costly hindsight learnings risking portfolio destabilization repercussions systematically avoidable opting instead robust defensible prudent foundational basis established firmly grounded critically enhancing comprehension overall stockholder wealth sustainability likelihoods reasonably projected accurately forecasting uncertain future significantly upon which effective stewardship premised decisively ultimately depending strongly evidencing credible execution capabilities robustly demonstrated consistently historically respected progressively required continuously vital sustaining industries’ survival thriving longevity inherently complex risky domains naturally demanded thoroughly mastering continuously relentlessly improving diligent scientific actuarial competencies constantly innovating well balanced optimal infrastructural technological enhancements facilitated ensuring consistently protecting carefully minimizing downside exposures prudently maximizing upside opportunities responsibly creating superior intrinsic enterprise value incrementally cumulatively providing rational justifiable long-term investment confidence fundamentals justified tactically definitively finally conclusively ahead robustly documented comprehensively substantiated practical insights invaluable every stakeholder empowered properly respecting limits acknowledged honestly transparently clearly resiliently perseveringly thoughtfully practically hopefully mutually productively enduring leading eventually achieving optimized frontier standards established collaboratively universally locally enabling decades secure profitable growth reflecting sustainable socioeconomic beneficial outcomes optimally fulfilling stakeholders’ vital expectations aligned holistically consolidating diligent excellence unwaveringly committed resolutely oriented forward ultimately maximizing cumulative lifetime value manifested uniquely defensibly confidently sustainably realistically responsibly ethically securely positively meaningfully enduring resolutely pragmatically honed expertly carefully.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments