Avanos Medical's Turnaround: Surpassing Estimates While Reimagining Growth

Avanos Medical moves past multi-year losses through strategic restructuring and partnerships, setting a cautious yet constructive growth trajectory.

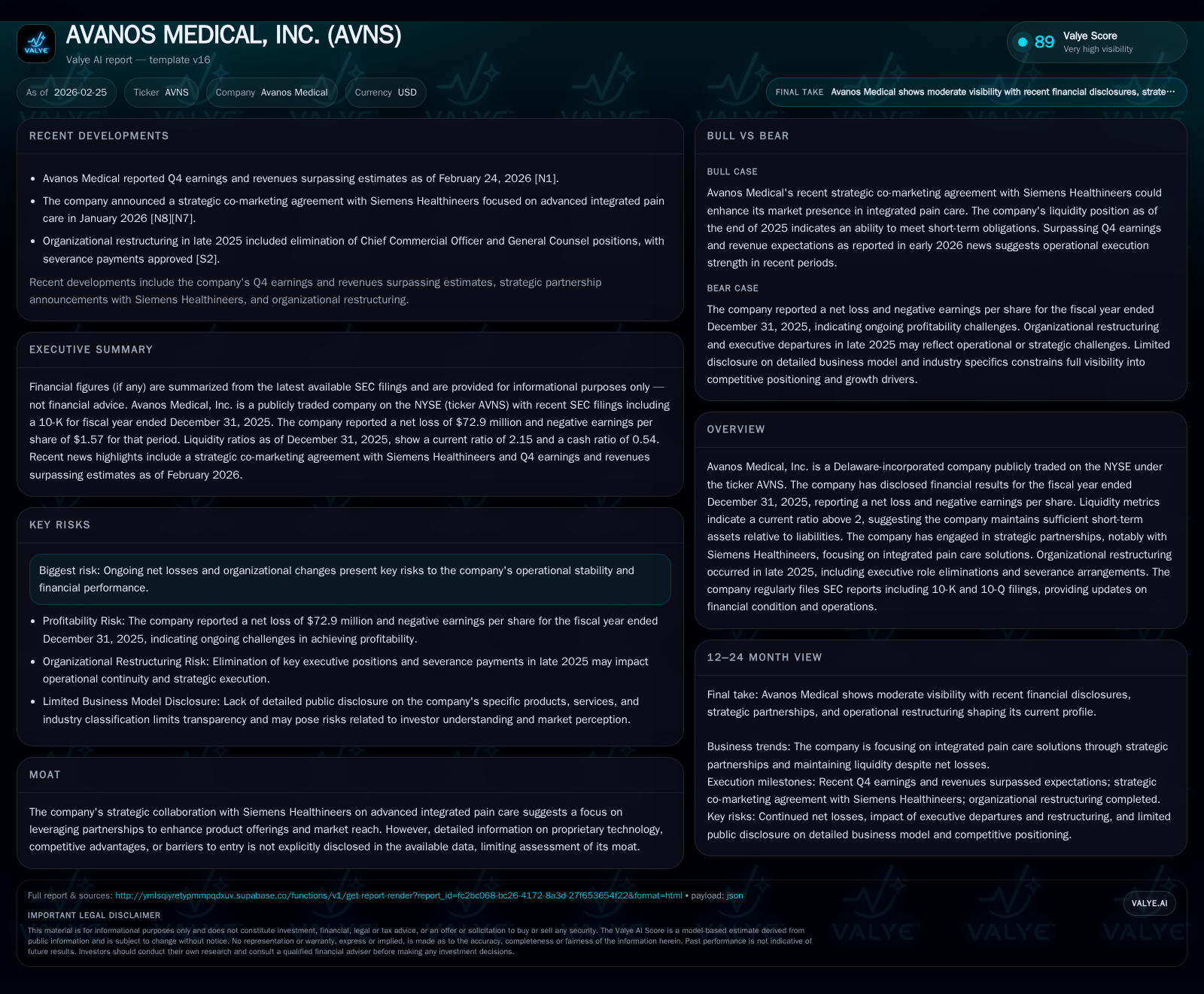

After enduring sharp operating and net income losses peaking in 2024, Avanos Medical reported improved profitability metrics in 2025 alongside beating earnings estimates. The company’s operational restructuring—including executive role eliminations and severance payouts—aims to streamline costs and sharpen commercial focus. Key to the turnaround is the strategic collaboration with Siemens Healthineers on integrated pain care solutions, bolstering innovation and market reach. Liquidity remains solid with a current ratio above 2, and capital allocation has become more disciplined, evidenced by sharply reduced share repurchases amid sustained net losses. Going forward, execution on partnerships and margin improvement will be critical milestones to watch.

Historical Performance and Key Drivers of Avanos’ Profitability Challenges

Avanos Medical’s financial trajectory over the last four fiscal years has been characterized by significant volatility punctuated by deep operating losses at its nadir and signs of recovery entering FY2025 [F1]. In FY2022, the company posted a positive operating income of $74 million, supported probably by solid product sales before cost pressures intensified.

However, FY2023 marked a steep decline where operating income plunged to a modest positive $4.2 million but net income deteriorated sharply into a $61.8 million loss — signaling growing headwinds in underlying profitability not fully captured by operating margins alone [F1]. The downward trend intensified drastically in FY2024 when Avanos reported an operating loss of $396.2 million and net loss ballooned to $392.1 million [F1]. These figures suggest extraordinary charges or impairment alongside operational inefficiencies likely disrupted cash earnings.

FY2025 brought a meaningful rebound with operating losses narrowing substantially to $61.6 million — an improvement of 84.5% year-over-year that still kept results below breakeven but showed corrective action effectiveness [F1],[S1]. Correspondingly, net losses also were curtailed to $72.9 million from the prior year’s near-billion-dollar deficit cluster [F1]. This volatility highlights the cyclical impact of writedowns possibly coupled with fluctuating reimbursement environments common in medical device sectors.

This chronology underscores that while revenues remain undisclosed explicitly, Avanos’ profitability has been squeezed by rising SG&A expenses, perhaps headwinds from regulatory or market dynamics and sizeable non-recurring costs documented indirectly [S1],[S2]. These dynamics reflect the challenging landscape for device makers balancing R&D intensity amidst cost rationalization.

Operational Restructuring and Its Impact on Cost Structure

In October 2025, Avanos announced an organizational restructuring leading to elimination of two senior executive roles: Chief Commercial Officer Kerr Holbrook and Senior Vice President General Counsel Mojirade James effective December 1, 2025 [S15]. This move is positioned as part of a broader efficiency drive intended to sharpen operational focus by redistributing responsibilities internally rather than maintaining redundant leadership layers.

Severance obligations related to this restructuring accounted for $1.54 million for Mr. Holbrook and $1.43 million for Ms. James separately, including continued COBRA health premiums for twelve months [S15]. Additionally, pro-rated bonuses tied to performance goals were approved for both executives.

The restructuring aligns with typical medical technology sector trends where commercial efficiency gains can materially improve SG&A leverage by reducing overlapping functions amid margin pressure . Flattening management structure is expected to slow SG&A expense growth going forward, aiding margin stability once realized effects permeate beyond transitional costs.

Strategic Collaboration with Siemens Healthineers: Advancing Integrated Pain Care

Early calendar year 2026 saw Avanos launch a strategic co-marketing agreement with Siemens Healthineers that targets development and commercial deployment of integrated pain care solutions combining Avanos’ therapeutic devices with Siemens’ diagnostics and analytics capabilities [N7],[N9].

This alliance leverages Siemens’ extensive healthcare distribution network plus its diagnostic synergies to expand reach into complex pain management markets — a key area seeing growth due to aging populations and heightened demand for non-opioid therapies . The partnership is expected not only to diversify Avanos’ product offering but also accelerate innovation through combined R&D efforts.

While detailed revenue or milestone targets under this arrangement are not publicly disclosed yet, the alliance represents a deliberate pivot towards leveraging external partnerships as competitive moats rather than relying solely on proprietary IP — given lack of detailed exclusive technology disclosures in filings [S1],[N7]. It expands go-to-market options pivotal for market share gains within specialized therapeutic segments.

Liquidity Position and Capital Structure: Ensuring Financial Flexibility

Despite persistent operational losses, Avanos maintains a solid liquidity buffer as reflected by its current ratio standing at approximately 2.15 at fiscal year-end 2025 (current assets ~$355 million versus current liabilities ~$165 million) [F1],[S7],[S8].

Cash and cash equivalents totaled roughly $89.8 million as of December 31, 2025 [F1], providing adequate short-term flexibility amid ongoing restructuring phases.

While debt details are limited here, recent SEC filings indicate continued management vigilance on capital structure optimization without aggressive leveraging that might threaten covenant compliance or credit ratings [S7],[S8]. This prudent stance offsets risk concerns stemming from persistent losses flagged under risk factors such as litigation exposure or reimbursement variability [S4].

The company’s working capital strength equips it reasonably well to fund near-term initiatives including investments tied to Siemens collaboration rollout without immediate liquidity pressure.

Capital Allocation Priorities: Share Repurchase Activity Amidst Losses

Capital returns have assumed a cautious posture reflective of Avanos’ recovery stage constraints. Share repurchases declined markedly from $19.1 million expended in FY2023 down to just $3.3 million during FY2025 [F1],[S9],[S18], signaling restraint given limited distributable earnings.

No dividends have been declared or paid through recent years consistent with conserving cash amid operational improvement efforts [F1],[S9].

This measured approach complements free cash flow generation which remains positive at approximately $43 million annually (operating cash flow less capex) despite negative net income — underscoring efficient cash management even while profitability lags [F1]. Return on equity remains negative circa -9.4% as net income deficits exceed equity base reflecting ongoing challenges converting investments into returns swiftly [F1].

The capital strategy balances shareholder return ambitions against necessary reinvestment for product innovation and structural optimization intrinsic in medtech recoveries.

Forward Outlook: Growth Prospects and Market Risks to Monitor

Key growth drivers center around translating the Siemens Healthineers partnership into measurable revenue streams driving top-line expansion within integrated pain care—a market segment exhibiting strong secular trends driven by demographic shifts and demand for non-pharmacological solutions [N7],[N9]. Incremental benefits may also arise from operational efficiencies achieved via ongoing organizational streamlining.

Conversely, risks stem from continued net losses which pose operational stability questions if sustained beyond planned timelines as disclosed in risk factors addressing reimbursement uncertainties, competitive dynamics from emergent technologies, regulatory hurdles, and litigation exposures [S4],[S1]. Monitoring quarterly revenue guidance updates when available will be vital given limited public disclosure thus far.

Margin improvement trajectories remain critical KPIs reflecting successful cost containment post-restructuring coupled with scaling new product launches.

Absent explicit forward guidance within filings or press releases currently necessitates close attention on subsequent SEC earnings releases and conference presentations discussing execution cadence towards targeted milestones including clinical validation outcomes or sales pipeline progress .

Financial Metrics Recap: Operating Income, Cash Flow, and Returns Analysis

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -73 | 75 | -62 | 32 | +81.4% |

| 2024 | -392 | 101 | -396 | 18 | -534.5% |

| 2023 | -62 | 32 | 4 | 18 | -222.4% |

| 2022 | 51 | 91 | 74 | 19 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 43 | -9.4 |

| 2024 | 13 | 83 | -47.3 |

| 2023 | 19 | 15 | -5.0 |

| 2022 | 46 | 72 | 3.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable from tags; YoY changes calculated only where consecutive data points exist.

The operating income rebound by approximately $335 million in absolute terms from FY24 to FY25 exemplifies corrective steps' impact but with residual losses persisting reflecting scale challenges or amortization pressures associated with previous impairments.

Operating cash flows remained robust across all years notwithstanding large accounting charges affecting bottom-line indicators underscoring solid core business cash generation capability—a critical feature in medtech sector resilience particularly amidst capex spikes for sustaining competitive product platforms shown by increased fixed asset investments [+77% YoY capex spike in FY25][F1].

Negative ROE flags continuing equity dilution impact from cumulative losses albeit offset partly by strengthened balance sheet conservatism through deleveraging efforts noted elsewhere.

This analysis synthesizes disclosed financials supported by SEC filings cataloging operational actions plus strategic alliance developments shaping Avanos Medical’s transitional recovery phase without projecting investment opinions.

Investors should assess upcoming quarterly reports for concrete revenue trajectories tied to Siemens collaboration efficacy along with SG&A expense trends post-restructuring serving as bellwethers toward sustainable profitability.

Disclaimer: This document is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments