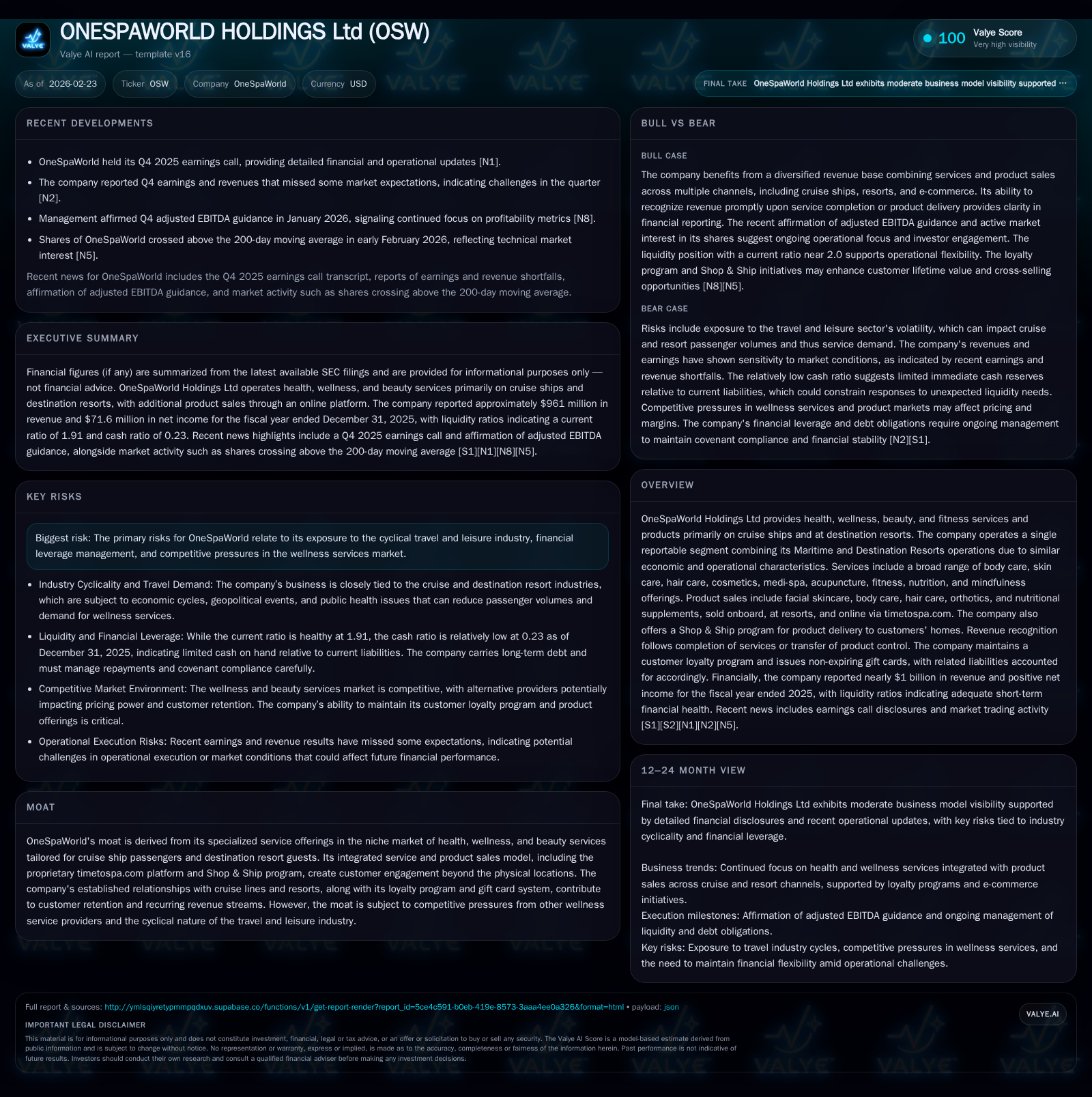

OneSpaWorld Holdings: Financial Recovery and Strategic Renewal in Maritime Wellness

Examining OneSpaWorld's recent financial trends and strategic capital moves as it leverages cruise industry recovery amid inherent sector risks.

OneSpaWorld Holdings has demonstrated consistent revenue expansion, driven primarily by the post-pandemic rebound in cruise passengers and enhanced product sales via its proprietary platforms. The company operates a unified reportable segment encompassing Maritime and Destination Resorts, enabling integrated wellness service delivery. Capital allocation initiatives including share repurchases and dividends align with improving cash flows and a moderately leveraged capital structure. Despite operational headwinds linked to cyclical travel demand and competitive wellness markets, upcoming quarterly earnings will be pivotal in assessing momentum sustainability.

Financial Trajectory: Revenue Expansion and Operating Margins

ONESPAWORLD HOLDINGS Ltd (OSW) has experienced a significant financial turnaround since FY2022, with revenues rising sharply from approximately $546 million to $961 million by FY2025—a compound effect amplified by the global recovery in maritime leisure travel post-pandemic [F1]. This represents an annual growth rate near 7.4% between FY2024 and FY2025 alone.

Operating income followed a similar upward trajectory, advancing from $15.1 million in FY2022 to $81.6 million in FY2025—an over fivefold increase within three years—and signaling improved operational leverage amid expanding margins [F1]. The notable rise in capital expenditures in FY2025 (+123.5% YoY to roughly $15 million), compared with previous years’ levels near $6-7 million, highlights an active reinvestment phase likely supporting facility upgrades or fleet expansions relevant to the cruise wellness ecosystem [F1], underscoring management’s commitment to long-term service quality.

Net income recovered robustly as well, reaching $71.6 million in FY2025 after negative results posted during more turbulent pandemic-affected periods, reflecting both revenue growth and enhanced cost discipline. This translated into a return on equity estimate of roughly 13.2%, demonstrating effective capital utilization given equity levels above $542 million at fiscal year-end [F1]. Operating cash flow also grew steadily to approximately $83.5 million in FY2025, outpacing capex spend sufficiently to sustain positive free cash flow generation.

Historical Financial Performance Summary FY2022-FY2025

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 961 | 72 | 84 | 82 | +7.4% | -1.7% |

| 2024 | 895 | 73 | 79 | 78 | +12.7% | +2550.0% |

| 2023 | 794 | -3 | 63 | 54 | +45.4% | -105.6% |

| 2022 | 546 | 53 | 25 | 15 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 17 | 75 | 68 |

| 2024 | 8 | 19 | 72 |

| 2023 | 9 | 58 | |

| 2022 | 20 |

Source: SEC companyfacts cache [F1].

Note: Some YoY calculations omitted due to negative or irregular prior year figures.

Drivers Behind OneSpaWorld’s Revenue Growth Over Recent Years

The primary catalyst behind OSW's sustained revenue growth is the resumption of cruising activities that had been severely disrupted during the COVID-19 pandemic era. As passenger volumes normalized, demand for specialized spa, wellness, fitness, and beauty services onboard ships accelerated correspondingly [N1]. Complementing this tailwind is OneSpaWorld’s strategic development of its proprietary digital asset portfolio—including timetospa.com—which extends its platform beyond physical locations into online product sales featuring skincare lines, supplements, orthotics, and more.

Additionally, the Shop & Ship program facilitates delivery of products directly to consumers’ homes post-trip, thus nurturing ongoing engagement outside the transient nature of cruise visits [N1]. The company’s loyalty scheme contributes meaningfully too; it incentivizes repeat visits through gift cards that do not expire, creating deferred liabilities but securing predictable future revenues.

This symbiotic business model blending services with retail concessions captures additional wallet share per passenger while smoothing revenue seasonality common with maritime leisure cycles.

Service Integration and Market Position within Cruise and Resort Wellness

OneSpaWorld consolidates its Maritime operations with Destination Resorts into a single reportable segment reflecting congruent service profiles and economic drivers [S1]. This integration aligns seamlessly with its focus on affluent travelers seeking holistic wellness journeys that combine spa treatments, fitness regimes, medi-spa therapies such as acupuncture or nutrition counseling alongside cosmetic products.

The company’s footprint on multiple major cruise lines—where spa concessions often operate under exclusive agreements—and select luxury resorts enables it to leverage captive customer bases presenting higher average spends than standalone urban spas or resorts absent maritime affiliation [S15]. Combining these venues blurs the line between hospitality service provision and retail concession economics, blending fixed fee components with performance incentives linked to guest traffic.

The timetospa.com website acts as a digital extension of this ecosystem offering convenience-driven commerce post-disembarkation while enabling data insights into consumer preferences fueling tailored marketing.

Assessing Operational Challenges and Market Headwinds for Future Growth

Despite favorable demand patterns resurfacing through mid-2020s recovery phases, OSW faces pronounced cyclicality endemic to the leisure travel sector that renders revenue predictability challenging during downturns or macro disruptions [S12]. Analyst revisions following Q4 earnings indicated some softness in bookings impacting near-term top-line expectations with missed consensus estimates reported [N2], highlighting vulnerability tied directly to fluctuating cruise itineraries or geopolitical factors affecting passenger confidence.

Competitive pressure intensifies as land-based spa chains or standalone resort operators mount increasingly sophisticated wellness offers potentially diverting discretionary spend from cruise-specific vendors while e-commerce giants encroach on niche beauty supplement spaces previously dominated by specialty providers.[N3]

Further complexity arises indirectly from cost inflation pressures associated with fuel surcharges impacting cruise operators who may pass along expenses via ticket pricing – subsequently influencing passenger volumes relevant for OSW’s client base [N5]. Currency volatility could affect expense structures given multinational operation footprints.

Capital Structure, Debt Covenants, and Liquidity Management

ONESPAWORLD maintains leverage discipline under a New Credit Agreement executed September 20, 2024 featuring a senior secured term loan facility ($100 million fully drawn) complemented by an undrawn revolving credit facility of up to $50 million providing liquidity optionality without immediate drawdown requirements [S6][S9].

Mandatory quarterly amortization payments commenced March 31, 2025 equating to roughly 1.25% of original principal have been offset partly via voluntary prepayments totaling at least $10 million recently—effectively reducing scheduled amortization obligations through late 2026 per debt amortization schedules disclosed publicly [S17]. The agreement stipulates a maximum consolidated total leverage ratio ceiling at four times EBITDAR-related metrics alongside minimum fixed charge coverage ratios ensuring prudent leverage controls are preserved.

Approximately all assets serve as collateral under these credit facilities with customary negative covenants restricting additional indebtedness issuance or excessive dividend payouts beyond defined bounds maintaining lender comfort levels amid operational business cycles.[S7]

Capital Allocation: Dividends, Share Repurchases, and Investment Strategy

Capital returned to shareholders reflects confidence aligned with improving cash flows; management inaugurated quarterly dividends at $0.04 per share starting early calendar year 2025 marking a strategic shift toward returning value after prolonged retention during pandemic stress periods [S8]. Dividend payments totaled nearly $17.5 million by end-FY25 reflecting this policy consistency facilitated by enhanced free cash generation.

Share repurchase programs exhibit incremental scale-up — expanding from initial authorizations of $50 million in April 2024 followed by approval of a $75 million plan April 2025 underpinning an opportunistic buyback strategy revisiting valuation multiples pragmatically amidst market fluctuations [S5][S27].[F1]

Investment spends evidenced by capital expenditure hikes underpin growth strategy centered around upgrading spa facilities aboard vessels or rejuvenating retail outlets possibly aimed at enhancing guest experience quality standards commensurate with competitive positioning.[F1]

Forward-Looking Milestones: What Watching Q1 2026 Earnings Can Reveal

The forthcoming Q1 earnings release commands focus on oscillations tied to seasonal demand patterns intrinsic to cruise itineraries which modulate passenger flow strength early in calendar years relative to busier summer quarters.[N4] Metrics spotlighted include adjusted EBITDA confirmations against previous guidance signals alongside granular commentary on loyalty program enrollment trends critical for projecting future deferred revenues sourced from non-expiring gift cards.[N3]

Margin evolutions serving combined service-and-product sales models will also provide early confirmation of operational leverage sustainment or cost pressures encountered within inflationary environments.[N1] Any material deviations can recalibrate medium-term forecasts significantly given market sensitivity surrounding travel sector recoveries continuing amid lingering headwinds.[N2]

Valuation Considerations: Balancing Growth Opportunities Against Sector Risks

ONESPAWORLD's competitive advantage derives principally from its niche maritime wellness specialization supported by proprietary digital platforms engendering customer stickiness extending beyond physical venues. However, dependence on cyclical leisure spending renders earnings subject to sharp variability connected to global travel patterns susceptible to health crises or geopolitical shocks.[N3]

Investors should incorporate scenario analyses when contemplating valuation multiples; factoring predictable recurring revenue streams from loyalty programs against periodic soft patches related to vessel deployments constitutes prudent modeling assumptions for more balanced outlooks.

Capital return strategies emphasize cautiousness balancing reinvestment needs against shareholder distributions which flirt dynamically between growth investment phases and yield-oriented allocation reflecting evolving business maturity stages.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available filings and news sources as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments