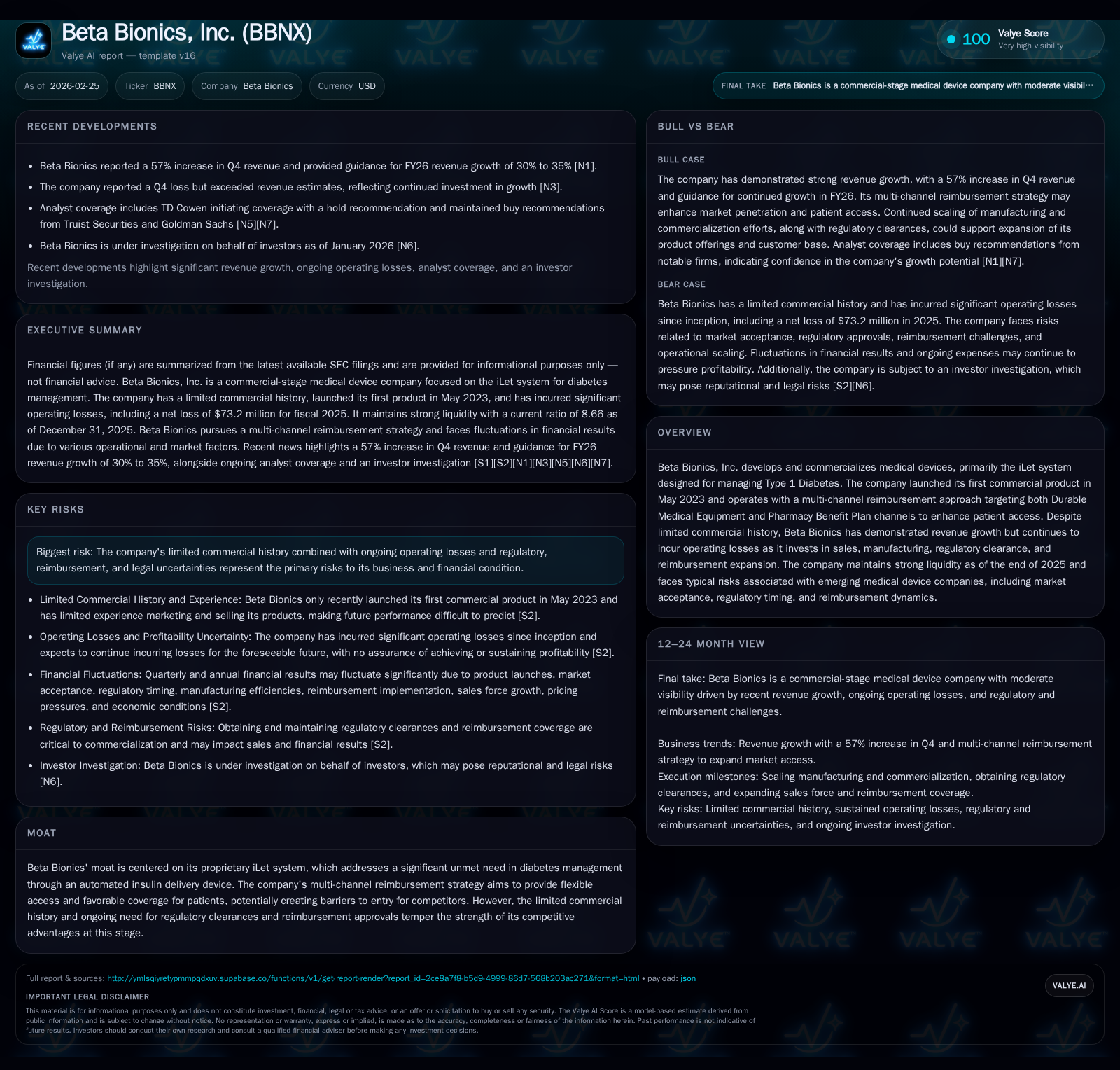

Beta Bionics’ Growth Trajectory Constrained by Regulatory Challenges and Profitability Pressures

Beta Bionics has shown promising revenue growth post-commercial launch of its iLet system while facing regulatory scrutiny and sustained operating losses.

Beta Bionics, a commercial-stage medical device company specializing in automated insulin delivery for Type 1 Diabetes, has demonstrated accelerating revenue growth since launching the iLet system in May 2023. Despite this progress, the company continues to operate at sizable losses intensified by regulatory inspections culminating in a recent FDA Warning Letter. Its multi-channel reimbursement strategy targeting Durable Medical Equipment and Pharmacy Benefit Plans supports expanding patient access but has yet to translate into profitability. With strong liquidity and corporate governance typical of emerging medtech firms, Beta Bionics enters 2026 balancing promising market positioning against persistent operational and regulatory risks.

Overview and Market Positioning

Beta Bionics, Inc. entered the commercial stage relatively recently with its flagship iLet automated insulin delivery system targeting Type 1 Diabetes (T1D) management—a field characterized by substantial unmet medical needs and growing demand for advanced medical devices that simplify glucose control. Commercialization commenced in May 2023 following regulatory clearance, situating Beta Bionics within the burgeoning medtech sub-sector focused on closed-loop insulin delivery systems.

The company’s moat derives principally from its proprietary iLet platform's ability to automate glucose-responsive insulin dosing—a critical differentiator over traditional pump therapy reliant on manual input and frequent user intervention. This positions Beta Bionics favorably against established competitors attempting to innovate within tight regulatory frameworks.

Moreover, Beta Bionics pursues a nuanced reimbursement approach utilizing both Durable Medical Equipment (DME) and Pharmacy Benefit Plan (PBP) channels. This multi-channel strategy allows broader payor engagement by optimizing coverage pathways across different patient insurance plans—essential given reimbursement complexities typical for high-cost diabetes devices.[S12][S9]

Historical Growth and Financial Performance

Since launching the iLet product, Beta Bionics has experienced tangible revenue acceleration as market adoption progresses. Q4 2025 results highlighted a striking 57% year-over-year revenue hike,[N1] signaling growing acceptance among healthcare providers and patients with diabetes (PWD). However, specific revenue figures are not disclosed in available filings,[F1] reflecting still nascent reporting transparency common for emerging device companies.

The table below summarizes key financial metrics illustrating Beta Bionics’ operational scale-up accompanied by deepening losses as it invests heavily across commercialization initiatives:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -73 | -51 | -72 | 5 | -33.7% |

| 2024 | -55 | -48 | -45 | 3 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -56 | -25.5 |

| 2024 | -52 | 22.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available from provided tags; dividends and share buybacks data also unavailable.

The sharp deterioration in operating income reflects escalation in SG&A expenses primarily tied to expanding the sales force geographic footprint and scaling manufacturing capabilities ahead of demand growth.[S7][S8] Meanwhile, net income losses remain substantial with only gradual improvement linked partially to cost absorption efficiencies.

Operating cash flows stayed deeply negative (-$50.9M in 2025), pointing to continued funding needs despite rising revenues, while capital expenditures surged notably (+56%) as Beta Bionics invests in production capacity enhancements required to meet projected demand surge.[F1][S8] These cash burn dynamics underscore the company’s typical early commercial-stage profile: prioritizing top-line expansion over near-term profitability.

Equity turned markedly positive in FY25 (+$287.6M versus negative equity previously), boosted by capital raises that have reinforced the balance sheet,[F1] enabling ongoing spending flexibility without immediate liquidity stress—a premium for small-cap device innovators navigating reimbursement complexities.

Recent Operational Developments and Regulatory Environment

In January 2026, the company disclosed receipt of a Warning Letter from the U.S. Food and Drug Administration stemming from a June-July 2025 inspection at its Irvine manufacturing site.[S14][S15] The FDA raised concerns surrounding aspects of the quality management system including reporting processes tied to adverse events and product corrections/removals.

While these deficiencies do not currently restrict Beta Bionics’ ability to market or manufacture products or seek new clearances directly,[S14] they introduce uncertainty around regulatory timelines especially pertinent as Beta Bionics prepares next-generation product submissions such as “Mint,” expected to enter commercial phases toward end-2027.[N4][S10]

The company has initiated corrective measures including process improvements responsive to FDA observations,[S14] but no firm resolution date is provided, highlighting an ongoing risk vector that may impact investor sentiment or payor confidence if protracted.

Growth Prospects and Commercial Strategy

Management projects fiscal year 2026 revenue growth of approximately 30%–35%, reflecting robust demand traction following initial product rollout.[N1][N2] This outlook leans on continued scaling of sales infrastructure combined with expanded payer coverage resulting from their multi-channel reimbursement approach targeting both DME and PBP pathways.[S11][S12]

This dual-channel model enables flexible patient access depending on individual insurance benefits; for example, pharmacy benefit coverage often yields lower upfront out-of-pocket costs compared to traditional durable equipment routes which typically require more complex prior authorization procedures.[S12]

However, several growth constraints temper optimism:

- The limited number of cleared products caps near-term addressable market expansion until new product authorizations succeed.

- Pricing pressures common within competitive automated insulin delivery technology segments could squeeze margins.

- Adoption rates are dependent on physician recommendation patterns alongside patient acceptance levels—areas still evolving given relatively recent market introduction.

- Regulatory compliance issues outlined above create potential hurdles delaying new launches or increasing costs.[S14]

Given these factors along with typical seasonal variations linked to deductible resets affecting purchase timing,[S7] forecasting remains challenging though prospects reflect an improving commercial foundation.

Capital Allocation and Returns

Beta Bionics reinvests virtually all cash flows into business development; it neither pays dividends nor executes share repurchases.[F1]

Return metrics remain negative; approximate return on equity based on trailing annual net loss relative to equity stands near -25.5% for FY25,[F1] consistent with early commercialization phases where investments outweigh earnings.

The focus lies clearly on building long-term value through strategic capital deployment aimed at:

- Scaling manufacturing capabilities ensuring production volume meets growing demand,

- Investing in sales force growth necessary for broader geographic penetration,

- Continuing R&D for product enhancements supporting future regulatory submissions,

- Navigating reimbursement expansions critical for sustainable sales growth.

Investors should monitor cash burn trends closely alongside progress resolving FDA quality concerns as indicators influencing capital requirements beyond current liquidity positions ($31.6 million cash/equivalents end-2025).[F1][S16]

Industry Context Analysis

Automated insulin delivery remains one of the most dynamic subsegments within diabetes technology due to innovation like hybrid closed-loop systems that reduce hypoglycemic events while improving glycemic control metrics critical for patient outcomes.

Competition includes established medtech giants intensifying investment into algorithm enhancements and sensor integrations leading to incremental feature differentiation—raising bar on continuous innovation cycles.

Reimbursement models vary widely across U.S. insurers impacting patient out-of-pocket exposure significantly; firms pioneering multi-channel coverage options stand better poised to capture share especially given increased payer emphasis on value-based care programs.

Manufacturing scalability remains pivotal due to high regulation stringency plus complex supply chains involving disposable components—Beta Bionics’ capacity investments track industry trends emphasizing process automation and quality control sophistication.

What To Watch Next: Key Milestones & Catalysts

- FDA resolution status regarding current Warning Letter issues; adverse audit findings could delay new product launches or trigger recalls impacting reputation.

- Reported quarterly revenue progress versus guide—sustained acceleration would validate go-to-market effectiveness.

- Expansion of payer contracts especially under PBP pathways enhancing affordability perception among patients.

- Progress toward Mint commercialization anticipated by end-2027 remains crucial pipeline checkpoint signaling future growth sustainability.

- Development of secondary products or features broadening addressable population within T1D management spectrum.

- Cash flow/burn rate trajectory indicating financial health sufficiency reducing dilution or refinance risks.

Conclusion

Beta Bionics exhibits classic characteristics of an emerging medtech innovator striving to translate pioneering automated insulin delivery technology into scalable commercial success amid inherent risks associated with regulatory scrutiny, evolving reimbursement landscapes, operational expansion challenges, and competitive pressures.

While recent financials indicate accelerating sales momentum validating early market acceptance of the iLet system, ongoing operating losses highlight sizable execution risks before achieving profitability thresholds expected by investors long-term.

Regulatory developments including the recent FDA Warning Letter introduce notable uncertainty requiring close monitoring as they impact both short-term operational continuity and future growth vectors linked with pipeline product introductions like Mint.

Strong liquidity backed by prior capital raises provides runway flexibility allowing continued investments essential for capturing diabetes technology market opportunities characterized by rapid innovation cycles coupled with complex medical device commercialization dynamics.

As such, Beta Bionics represents a high-risk/high-reward profile typical for early-stage medtech companies transitioning toward sustainable commercial footing while contending with rigorous external scrutiny governing product safety and efficacy standards.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations regarding Beta Bionics stock or securities related thereto. It is prepared solely from publicly available information without endorsement or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments