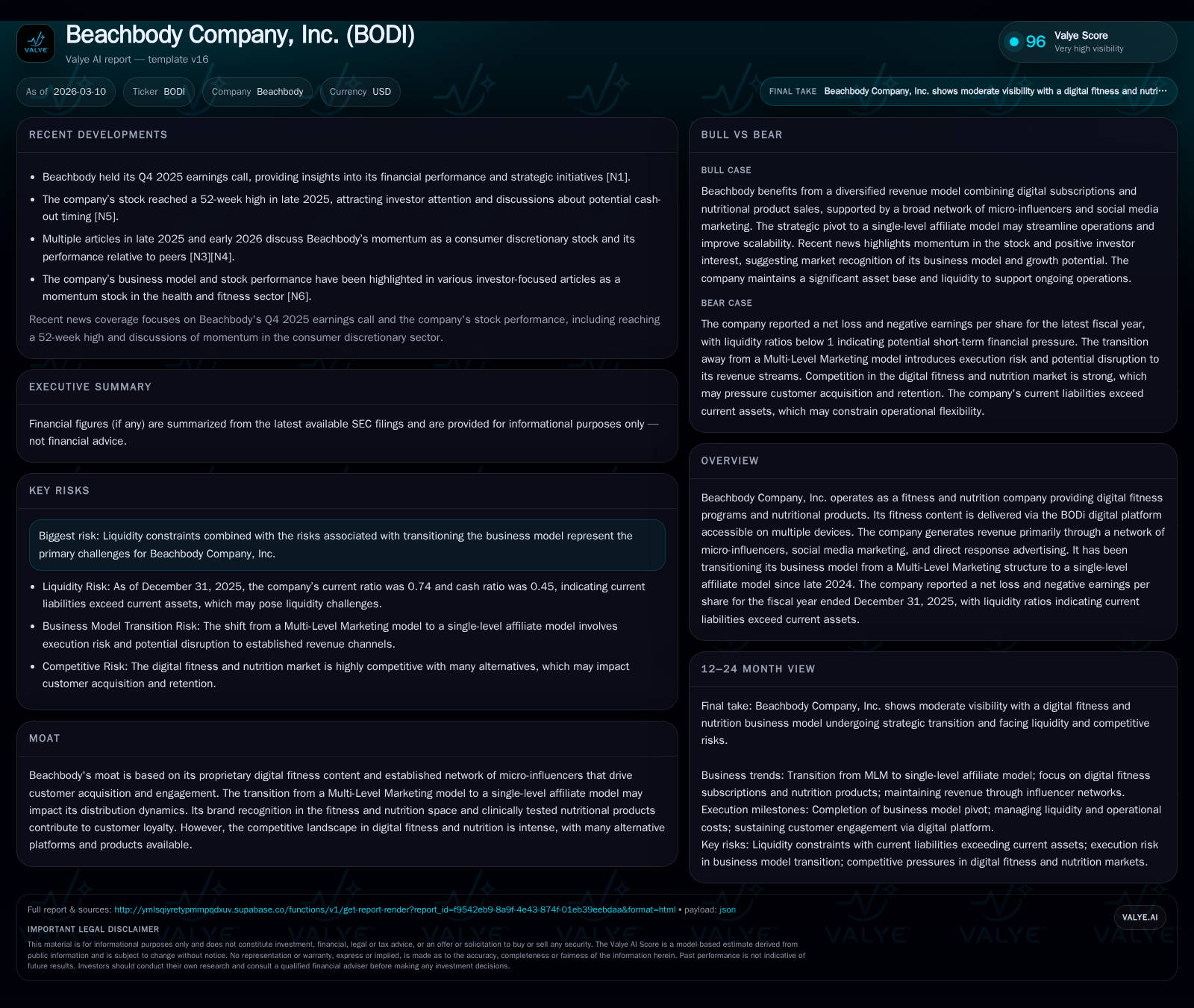

Beachbody's Turnaround: From Multi-Level Marketing to Digital Fitness Growth

Beachbody Company, Inc. has achieved a remarkable operational turnaround transitioning its business model while grappling with tight liquidity and market competition.

Beachbody's fiscal year 2025 results mark a substantial shift from multi-year operating losses to positive operating income, underscoring improved operational leverage amid an ongoing net loss. The company is executing a strategic pivot from a multi-level marketing model to a single-level affiliate structure, aiming to reshape its revenue channels that heavily rely on micro-influencers and digital engagement. Despite the progress, liquidity ratios highlight stress with current liabilities exceeding current assets, while the company anticipates potential debt covenant violations requiring lender negotiations. Going forward, growth depends on successful subscription retention and affiliate program execution amidst intense digital fitness competition.

Historic Performance Shift: From Steep Losses to Modest Operating Income

Beachbody Company, Inc.'s financial trajectory over recent years demonstrates a striking operational turnaround culminating in fiscal year (FY) 2025. After enduring significant operating losses—$203.2 million in FY2022, narrowing sequentially to $66.2 million in FY2024—the company reported a positive operating income of $5.53 million for FY2025 according to the latest filings [F1]. This equates to an over 108% year-over-year improvement in operational profitability.

Despite this positive shift in operating income, Beachbody's net income remained negative at approximately -$2.86 million in FY2025. The sustained net losses suggest that non-operating expenses or one-time restructuring charges related to the ongoing business model transition continue to weigh on bottom-line results [F1].

Operating cash flow paints an encouraging picture with a recovery from negative flows in prior years (-$47.17 million in FY2022 and -$22.54 million in FY2023) to a solid positive inflow of $21.75 million in FY2025. This recovery underscores enhanced operational efficiency and working capital management during this period [F1]. Capital expenditures (capex) have been tightly managed post prior peak investments in earlier years ($26.49 million in FY2022), holding relatively steady near $4.4 million in FY2025 [F1].

This financial evolution reflects Beachbody’s move to extract leverage from its digital fitness content and platform investments amidst structural changes.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | 22 | 6 | 4 | +96.0% |

| 2024 | -72 | 3 | -66 | 5 | +53.1% |

| 2023 | -153 | -23 | -141 | 7 | +21.4% |

| 2022 | -194 | -47 | -203 | 26 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 17 | -9.1 |

| 2024 | -2 | -254.3 |

| 2023 | -29 | -184.4 |

| 2022 | -74 | -91.8 |

Source: SEC companyfacts cache [F1].

The above table summarizes Beachbody’s key annual financial metrics illustrating the multi-year progression.

Revenue Drivers and the Role of the Micro-Influencer Network Pivot

Beachbody’s revenue generation historically pivots around its proprietary digital fitness platform BODi combined with nutritional products such as Shakeology shakes and supplements clinically tested to support customer goals [S1]. Central to its go-to-market strategy is an established network of micro-influencers or “Partners,” who utilize social media channels and engage in direct response advertising campaigns aimed at acquiring and retaining customers [N1][S1].

This influencer network acts as both brand ambassadors and customer conversion engines within the digital fitness ecosystem—a critical factor given the crowded competitive landscape populated by numerous alternative connected fitness platforms.

However, transitioning from Multi-Level Marketing (MLM) incentivization structures toward a streamlined single-level affiliate model necessitates restructuring these partner relationships significantly [N1]. In typical digital fitness affiliate marketing parlance—multi-tier commissions give way to linear commission schemes reducing channel complexity but increasing pressure on partner loyalty.

Success here relies not just on reach expansion but balancing customer lifetime value retention through subscription renewals amid evolving affiliate dynamics.

Business Model Transformation: Navigating the MLM to Affiliate Shift

On September 30, 2024 Beachbody announced strategic initiatives targeting a pivot away from MLM's hierarchical structure toward a more straightforward single-level affiliate model [S7][N1]. Key motivations include minimizing channel conflicts intrinsic to MLMs where incentives drive recruitment proliferation over direct consumer sales.

This reconfiguration entails realigning commission schemes away from overrides inherent in MLM tiers toward direct commissions on sales volume attributable solely to individual affiliates [S7].

Operationally this raises partner churn risk as traditional MLM stakeholders recalibrate earnings expectations or exit the program.

From an industry context standpoint, affiliate models tend to streamline performance tracking and can enhance marketing ROI transparency but require bolstering partner motivation via differentiated digital tools or exclusive offers.

Beachbody’s pivot timing coincides with intensifying market competition from entrenched streaming fitness services compelling innovative distribution tactics.

Liquidity Landscape and Covenant Challenges

Beachbody's liquidity profile reveals tight working capital conditions: as of December 31, 2025 current assets stood at approximately $63.8 million against current liabilities of $86.6 million yielding a current ratio near 0.74—a suboptimal ratio signaling liquidity strain [F1].

The company carries a $35 million asset-based lending (ABL) facility with $25 million drawn as of Q3 2025 subject to financial covenants anchored primarily on minimum digital subscriber counts and billings thresholds [S7][S4]. Though compliant as of September 30th Q3 close ([S7]), Beachbody anticipates covenant violations at December quarter end due to transitional market impacts.

Management is actively engaged in discussions with lenders aiming for amendments expected by February 28th, 2026; absent successful waiver or amendment execution acceleration clauses potentially trigger debt repayment acceleration which would further pressure liquidity [S7].

Mitigation plans include cash preservation measures such as curtailing discretionary expenditures and optimizing operating cost structures within management control scope [S7]. This delicate dance underscores risk that capital constraints could impair operational freedom before business model stabilization completes.

Capital Allocation Focus: Cash Flow Recovery and Returns

Capital spending discipline has been apparent with capex reduced markedly since pre-transition years; maintaining around $4.4 million annually with no indication yet of aggressive expansion push post-pivot [F1]. Enhanced free cash flow generation ability is reflected by estimated free cash flow—operating cash flow minus capex—near $17.35 million for FY2025 signifying improving internal funding capability even amidst restructuring costs [F1].

Equity base contracted substantially since FY2022 peak ($211.5 million) down to about $31.3 million at FY25-end consistent with equity depletion driven by cumulative net losses [F1]. Estimated return on equity calculated from available metrics stands negative at approximately -9.1%, illustrating ongoing profitability challenges relative to shareholder capital employed despite turnaround strides [F1].

No dividends or share buybacks are indicated reflecting management priority on deleveraging and stabilizing operations before embarking on shareholder returns.

Future Outlook: Growth Prospects Amid Transition Risks

Looking ahead Beachbody aims to capitalize on its brand recognition coupled with clinically validated nutritional lines while deepening subscriber engagement across its BODi streaming platform—a recognized growth avenue leveraging scalable digital content delivery [N1][S7].

However success heavily depends on managing affiliate conversion effectiveness post-MLM disruption—a critical inflection impacting both topline growth and cost efficiency.

Competitive pressures are notable from both legacy gym operators adopting hybrid models plus fully digital native platforms boasting vast content libraries.

Furthermore liquidity uncertainties tied to covenant risks may impair agility required for investment in product innovation or customer acquisition scale-ups until balance sheet health improves.

Indicators and Milestones to Monitor Post-Transition

Key performance indicators for market participants tracking Beachbody include:

- Digital subscription growth rate reflecting user adoption momentum post-affiliate pivot;

- Affiliate partner retention metrics indicating success mitigating churn attributable to structural incentive changes;

- Billings compliance against ABL covenants closely monitoring impending lender renegotiations;

- Free cash flow trajectory validating operational self-sufficiency without external funding reliance;

- Operating margin improvements signaling scalable economics beyond pivot-related restructuring costs.

Monitoring quarterly updates especially around covenant amendments execution timelines alongside subscription cohort analyses will provide critical signals gauging whether Beachbody’s transformation secures durable profitability footing within hypercompetitive wellness space.

This analysis synthesizes publicly disclosed SEC filings ([S#]), earnings call transcripts ([N#]), and validated numeric data ([F1]) without speculative extrapolations. It intends solely for informational purposes reflecting corporate fundamentals and sector contextualization without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments