High Roller Technologies: Multi-Brand Strategy Fuels Growth Amid Regulatory Hurdles

High Roller Technologies capitalizes on its scalable multi-brand platform and strategic partnerships to advance player acquisition, while managing regulatory and liquidity challenges.

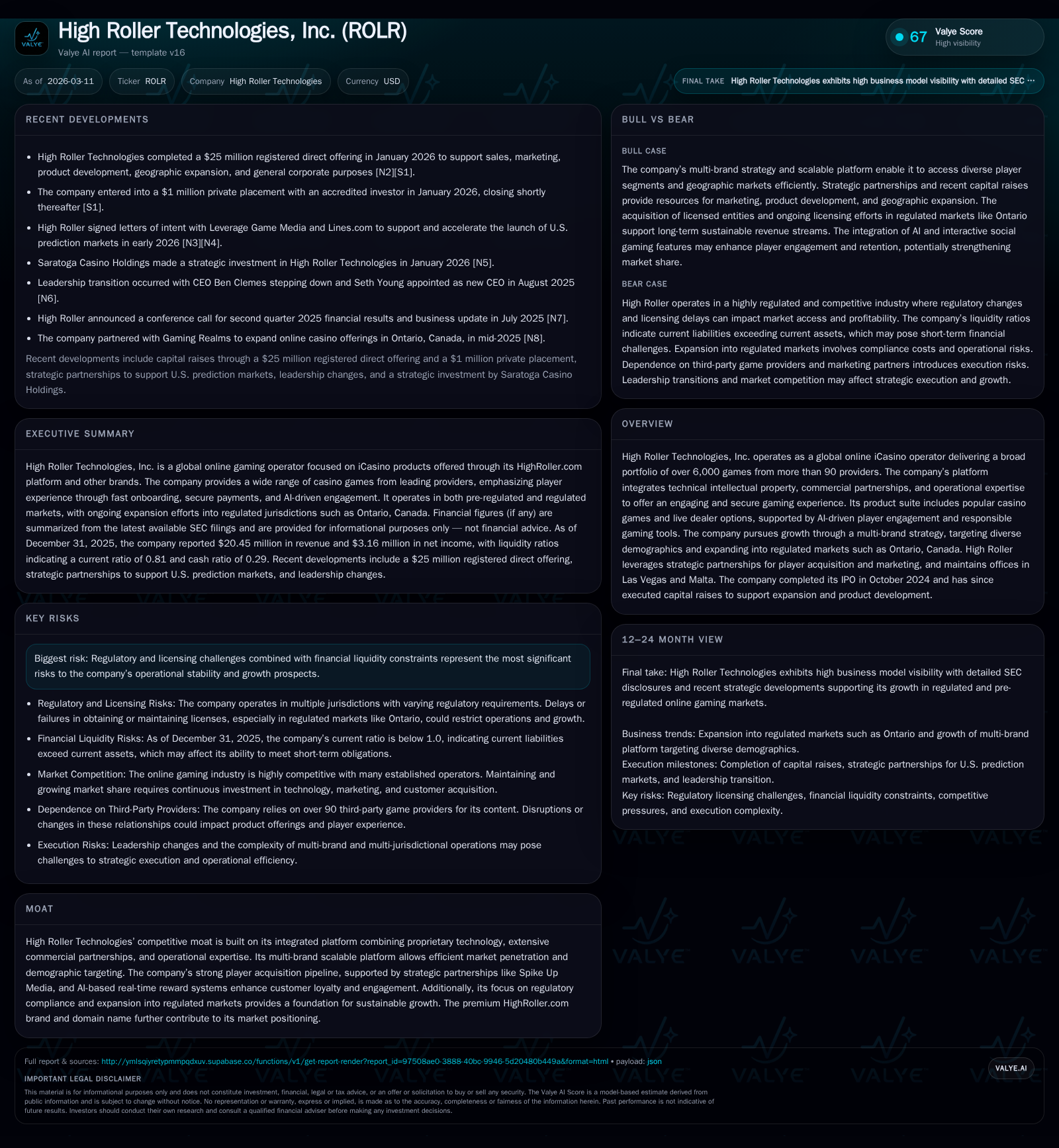

Since its October 2024 IPO, High Roller Technologies has seen revenue contract by 26.6% in 2025 but achieved a net income turnaround driven by operational adjustments and strategic acquisitions. Its multi-brand platform enables targeted demographic penetration across fragmented iCasino markets, supported by AI-driven player engagement tools and a strong marketing pipeline underpinned by partnerships like Spike Up Media. Despite these strengths, regulatory compliance costs and cash flow deficits pose growth constraints. Capital raises have funded expansion initiatives, with key market entry milestones such as Ontario’s license application underway.

From IPO to Expansion: Tracking High Roller's Recent Growth

High Roller Technologies swiftly transitioned from its October 2024 IPO into executing an aggressive multi-brand expansion, albeit against challenging top-line dynamics. The company reported a 26.6% year-over-year revenue contraction to $20.45 million for FY2025 compared to $27.88 million in FY2024 [F1]. This decline reflects the competitive pressures within highly fragmented online casino markets alongside regulatory headwinds impacting operational footprint.

However, operational recalibration yielded a positive net income of $3.16 million in FY2025 versus a $5.92 million loss in the prior year [F1], marked by improved cost discipline despite operating losses narrowing only modestly from -$5.79 million to -$6.18 million [F1]. Notably, the December 31, 2025 acquisition of Happy Hour Solutions Ltd. brought both a valuable Estonian remote gambling license and the casinoroom.com domain back into the fold—enabling broader European market access and content diversification that complement the company’s HighRoller.com premium brand positioning [S10].

The Multi-Brand Platform: Scaling in a Fragmented Online Casino Market

High Roller’s cornerstone is its scalable content management system functioning much like SaaS architecture that supports multiple distinct domains under a unified technology stack [S5]. This infrastructure facilitates rapid launches of localized brands optimized for discrete demographics, exemplified by Fruita.com (launched in 2024) and Kassuuu.com (introduced September 2025) [S5]. Such flexibility allows efficient audience segmentation affecting different player profiles without proportionate increases in fixed overhead or technology costs.

Strategically, this multi-brand approach counters the phenomenon where users maintain accounts across various operators by offering tailored gaming experiences per brand identity and regional preferences—strengthening retention potential within each segment [S7]. Management anticipates maintaining stable cost structures while leveraging existing player acquisition channels to fuel growth, implying operational leverage as brand count increases.

Capitalizing on AI: Player Engagement and Responsible Gaming Tools

The integration of AI-powered real-time reward systems stands out as an instrumental innovation amplifying customer lifetime value and engagement metrics. These internally developed algorithms dynamically tailor bonuses based on players’ activity patterning—game preferences, average bet size, frequency—thereby delivering personalized incentives aligned with behavioral segmentation models [S1][S5].

Concurrently, machine learning frameworks underpin responsible gaming tools governing play limits and flagging potentially problematic behaviors quickly within an interactive environment fostering both excitement and safety for users—a growing regulatory requirement across jurisdictions [N1][S7]. Such automation reinforces compliance postures while enhancing the user experience through seamless interactions without imposing overt restrictions.

Strategic Partnerships Driving Customer Acquisition Pipeline

High Roller benefits greatly from its affiliation with Spike Up Media LLC—a leading global affiliate specializing in online lead generation for iCasino operators which serves as one of the company’s primary sources of high-quality player leads [S7]. This partnership leverages industry-specific marketing expertise yielding superior conversion ratios and attractive payment arrangements.

Affiliate marketing remains widely utilized in B2C iGaming funnels where performance-based models optimize customer acquisition cost efficiency; High Roller’s embedded relationship uniquely positions it to extract maximum value from this channel without relying heavily on costly direct advertising campaigns [S5].

Regulatory Environment: Navigating Compliance and Market Entry

The company operates within a complex regulatory landscape that bifurcates into pre-regulated markets—where international licenses such as Malta or Estonia suffice—and more stringent regulated markets demanding local licensing regimes with accompanying compliance expenses and taxation burdens [S9][S4]. Despite the lower entry barriers of pre-regulated regions offering higher short-term margins but regulatory uncertainty long term, High Roller pursues prudent expansion into regulated markets like Ontario, Canada, where licensing approvals are pending with expected market launch slated for the second half of 2026 [S9][N1].

Balancing these differing jurisdictional demands entails elevated compliance operating costs offset by prospects for sustainable profit generation amid growing legal clarity—a critical tradeoff underscoring capital deployment decisions.

Financial Snapshot: Revenue Volatility, Profitability, and Cash Flow Trends

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 20 | 3 | -3 | -6 | -26.6% | +153.4% |

| 2024 | 28 | -6 | -4 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | 32.8 |

| 2024 | -4 | -103.5 |

Source: SEC companyfacts cache [F1].

Despite revenue contraction reflecting typical volatility early post-IPO amid shifting product offerings and geographic repositioning [F1], net income sharply turned positive driven by refined operational management combined with acquisition synergies realized from Happy Hour Solutions Ltd.[F1][S10]. Operating cash flow moderated its deficit yet remains negative at approximately -$3.23 million signaling continued working capital demands exceeding operating profits—a common scenario in scaling digital operators investing aggressively in customer growth pathways.

Capital expenditures contracted drastically to $51K as product innovation cycles focused on software enhancements over hardware or infrastructure spending during this mid-expansion phase [F1], reflecting an austere capital posture.

ROE calculated on end-of-year equity ($9.64 million) yields an impressive approximate return of nearly 33%, confirming investor capital is producing notable earnings despite ongoing cash flow volatility [F1].

Capital Allocation Priorities: Funding Growth and Managing Liquidity

The company has prioritized organic growth funding alongside select acquisitions over immediate shareholder distributions. Following the IPO in late 2024,[N1] High Roller completed strategic capital raises including a $25 million gross proceeds registered direct offering facilitated by ThinkEquity LLC closed January 21st, 2026; plus a smaller private placement raising approximately $1 million early January aimed at extending working capital runway into new product development and geographic expansion pursuits[S8][S13].

No dividends or share buybacks were declared or executed through FY2025 reflecting reinvestment focus amid ongoing cash burn consistent with early-stage technology-driven iCasino operators[S14][S18]. This allocation supports platform enhancements concurrent with necessary licensing applications such as Ontario’s regulatory process.[S9] Such financial discipline balances growth aspirations against prevailing liquidity constraints evidenced by sub-1 current ratio (0.81)[F1].

Looking Ahead: Key Milestones and Market Opportunities to Watch

While explicit forward guidance remains limited,[N1] investors should monitor the company’s progress toward critical catalysts including:

- Ontario market entry timeline: successful license procurement followed by commercial launch marks key regulated market footprint expansion[S9].

- Further launches of new localized brands leveraging platform scalability enabling incremental revenue streams without proportionate fixed cost increases[S5].

- Regulatory developments globally impacting license renewals or new market access conditions potentially affecting margins or investment cadence[S4][S6].

- Player acquisition efficacy measured through conversion rates from Spike Up Media partnership leads alongside retention improvements driven by AI engagement systems[S7][N1].

- Operating cash flow trajectory as business scales toward breakeven from an expensed investment base[F1].

Continued execution across these vectors will be essential for High Roller Technologies to solidify its position among fast-evolving global online iCasino competitors while overcoming intrinsic sectoral challenges like regulation complexity and financial resource constraints.

Disclaimer: This report is intended solely for informational purposes based on public filings and news disclosures relating to High Roller Technologies Inc., without offering investment advice or recommending securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments