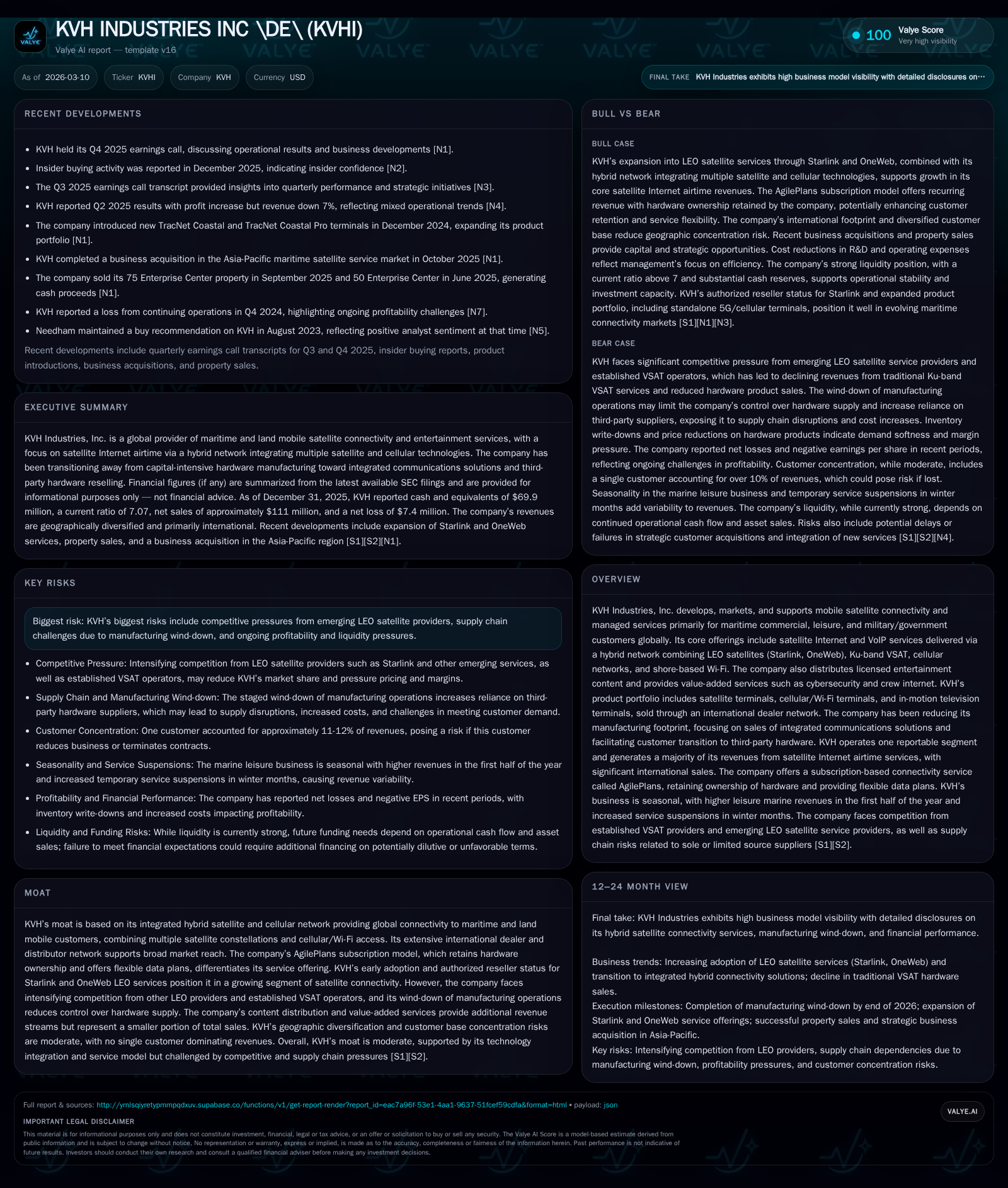

KVH Industries’ Shift from Manufacturing to Hybrid Satellite Services

KVH Industries has transitioned from a hardware-centric model to an integrated hybrid satellite connectivity provider, reshaping its growth drivers and competitive stance.

KVH Industries has been transforming its business by winding down manufacturing and pivoting towards hybrid satellite and cellular service offerings that leverage LEO constellations like Starlink and OneWeb. This shift has stabilized revenue growth amid declining product sales and intensified competition. Despite ongoing operating losses, improved cash flow and strategic acquisitions underpin the company’s capital discipline. The company remains exposed to supply chain risks, competitive pressures from emerging LEO networks, and customer concentration in key geographies. Future growth hinges on scaling hybrid airtime subscriptions and expanding partnerships within a complex multi-constellation maritime market.

Historical Revenue Trends and Shifting Growth Drivers

KVH Industries’ financial trajectory over recent years reflects a clear transition away from hardware manufacturing toward service-oriented revenue streams anchored in advanced satellite connectivity solutions. In fiscal year 2025, total net sales rose moderately by approximately 3.8% over the prior year [F1], reaching service sales dominance at nearly 89% of total revenue compared with roughly 85% in 2024 [S1]. In stark contrast, product sales shrank as a percentage of total revenue—from around 15% in 2024 down to about 11% in 2025—echoing the company's deliberate strategy to wind down manufacturing activities initiated in early 2024 [S1][S20]. This strategic pivot is further evidenced by the decrease in inventories from $22.9 million at end-2024 to approximately $13.4 million mid-2025 [S2].

Service revenue growth was chiefly fueled by the rapid uptake of LEO satellite services through authorized reseller relationships with Starlink since September 2023 and Eutelsat OneWeb maritime offerings launched early 2025 [S1][S21]. These emerging satellite constellations have incrementally displaced legacy Ku-band VSAT services historically responsible for much of KVH’s growth but now declining due to market saturation and increasing competition [S1]. The gradual erosion of Ku-band VSAT subscribers is reported alongside intensifying price-based competition encountered particularly during late 2023 into 2025 [S9][S11].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -7 | 17 | -11 | 7 | +33.2% |

| 2024 | -11 | -13 | -12 | 7 | +28.4% |

| 2023 | -15 | 3 | -17 | 11 | -164.0% |

| 2022 | 24 | 9 | -6 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1743000 | 10 | -5.6 |

| 2024 | 0 | -21 | -8.0 |

| 2023 | 239000 | -8 | -10.5 |

| 2022 | -5 | 15.4 |

Source: SEC companyfacts cache [F1].

Note: Financial figures for recent years sourced directly from [F1]; YoY values calculated between reported periods.

Products shifted away from terminals that KVH once manufactured internally; service contracts now predominantly recurred via subscription models bundling airtime and value-added services [S1][S6]. This swing also reflects the partial divestiture of the Middletown manufacturing footprint contributing to reduced fixed costs but increasing reliance on external hardware suppliers [S20].

Integration and Expansion of Hybrid Satellite Connectivity Services

KVH’s core differentiation lies in its "KVH ONE" hybrid network architecture integrating multiple satellite constellations—including Starlink’s LEO system under Global Priority data plans (authorized reseller since late 2023), SES’s Ku-band high-throughput satellites (HTS), Eutelsat OneWeb LEO network launched January 2025—and Iridium’s LEO constellation for voice services [S1][S21]. Layered atop satellite links are KVH-provided cellular services spanning more than 130 countries via its proprietary cellular/Wi-Fi terminals like TracNet Coastal introduced in late 2024 [S1][S6][S21].

This multi-channel mosaic offers maritime customers fluid transitions across networks depending on signal availability and bandwidth requirements — leveraging sector-specific network management complexities such as latency optimization between geostationary Ku-band VSAT paths versus low-earth orbit intermittent coverage windows with differential throughput profiles [S21][S6]. Such sophisticated constellation juggling is vital for uninterrupted onboard broadband Internet access for commercial vessels sailing remote ocean routes.

Crucially, KVH’s subscription-based AgilePlans retain ownership of terminals supplied to customers rather than outright sale; this locked-in hardware control facilitates recurring monthly fees tied directly to data usage tiers [S1][S21]. This model contrasts traditional one-off terminal purchase with airtime contracts and fosters customer retention amid non-committal monthly agreements prevalent across this sector.

Moreover, value-added services such as crew internet portals with cybersecurity features augment KMV’s content distribution business providing licensed entertainment programming across maritime customers globally—a modest but stable revenue contributor representing roughly 4% of total sales [S1].

Competitive Dynamics from Emerging LEO Providers and Market Risks

Despite technological advances rescuing revenue growth prospects, KVH faces formidable threats from escalating competition notably among LEO constellation operators expanding their maritime outreach including SpaceX’s Starlink portfolio extension beyond Global Priority offers towards localized terrestrial priority plans on inland waterways launched October 2024 [S1]. Other potential entrants such as Amazon's Kuiper or Canadian Telesat could intensify spectrum licensing challenges limiting throughput or forcing bandwidth rationing which could erode margins [S9][S19].

Concurrently, discontinuation of internal manufacturing exacerbates dependency on third-party terminal suppliers subject to supply chain volatility risking delivery delays or quality control issues impacting service activation schedules [S20][S9]. Supplier single-source dependencies underscore operational risks inherent in tightly integrated satellite communication products.

Market pricing pressure manifests through ongoing discounting cycles designed to fend off subscriber churn; notable example includes major client US Coast Guard reducing planned service commitment by ~95%, reflecting broader contract renewal unpredictability inherent within flexible month-to-month subscriber arrangements [S9]. Low barriers to switching highlight vulnerability despite integrated multi-network offerings.

Capital Structure, Cash Flow Recovery, and Shareholder Returns

Financially KVH demonstrated substantive improvements on liquidity fronts in FY25—operating cash flows turned positive at about $17.1 million versus a negative $13.2 million outflow prior year; this turnaround delivered free cash flow near $9.8 million after nearly flat capital expenditures approximating $7.4 million emphasizing disciplined capex management post-manufacturing sunset [F1].

Net loss narrowed to $7.4 million compared with $11 million loss the prior year reflecting operating loss reduction driven primarily by cost rationalization and contribution margin improvement from hybrid airtime product mix enhancements [F1]. Despite continued unprofitability generating negative return on equity near -5.6%, these trends signal a firm stabilizing cash generation profile supporting incremental capital deployment strategies.

In December 2024 KVH gained board authorization for a $10 million stock repurchase program under which it executed selective buybacks totaling roughly $1.74 million through three quarters of FY25—an indication of calibrated shareholder capital return amidst ongoing restructuring efforts focused on investment prioritization aligned with core connectivity business expansion ambitions [S8][F1][S17][S27]. No dividends have been issued reflecting internal reinvestment priorities.

Geographic Revenue Distribution and Customer Concentration Insights

KVH maintains a broadly international footprint: approximately 78% of consolidated revenues originate outside the U.S., concentrated geographically with Singapore accounting for about 21% consistently between FY24–FY25—the largest single foreign country exposure—while no other foreign country surpassed the 10% threshold individually [S4][S6][S7]. This geographic diversification attenuates geopolitical risks but subjects operations to layered regulatory compliance across numerous jurisdictions complicating licensing and service continuity efforts.

Customer concentration is pronounced yet manageable: one large customer contributed roughly 11% of sales in both FY24 and FY25; this entity also accounted for approximately one-fifth of trade accounts receivable though diversified receivables reduce credit risk somewhat through dispersion across smaller counterparties [S4][S7]. Aggregate concentration metrics warrant ongoing monitoring given potential impacts on working capital turnover where contract terminations or renewals can notably sway quarterly results.

Strategic Outlook: Innovation, Partnerships, and Market Positioning

Looking ahead via commentary derived from Q4 FY25 earnings call transcript highlights that KVH intends to deepen its collaboration footprint further with additional LEO partners beyond Starlink and OneWeb while iteratively refining AgilePlans subscription attributes targeting expanded maritime vessel segments including commercial fleets transitioning off legacy VSAT platforms [N1]. Incremental acquisitions like the October 2025 Asia-Pacific maritime satellite customer base purchase consolidate market positioning regionally offering greater scale efficiencies albeit exposing integration challenges around agreement consent transfers by counterparties warranting careful execution management [S17][S25].

Operationally success will hinge on preserving quality service levels within this intricate multi-constellation environment while balancing competitive pricing imperatives against margin sustainability prospects amidst evolving spectrum regulation backdrops internationally [N1][S9]. Monitoring shifts in subscriber mix towards higher ARPU accounts or longer contract tenors could serve as tangible forward indicators prior to formal guidance issuance.

This report leverages publicly available filings including KVH's Form 10-Ks, quarterly reports (10-Q), earnings calls transcripts as well as consolidated financial statements captured through authoritative SEC XBRL datasets reflecting figures accurate as of March 10th, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments