Medallion Financial Corp’s Diversified Lending Strategy Balances Growth and Funding Risks

Medallion Financial leverages its diversified loan portfolio and multi-source funding to sustain growth, while managing interest rate and liquidity pressures.

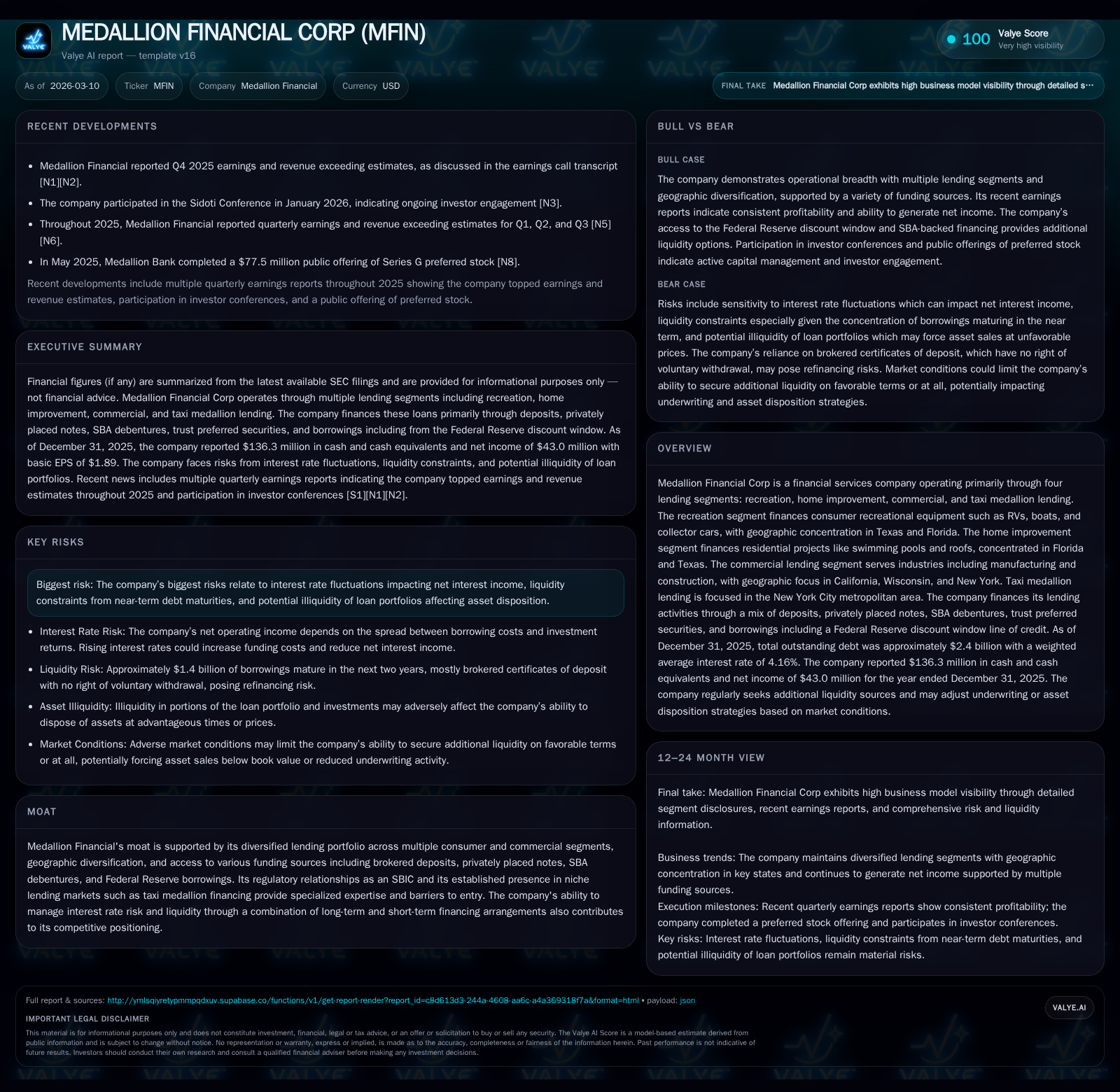

Medallion Financial Corp operates primarily in four lending segments spanning recreation, home improvement, commercial, and taxi medallion loans with geographic focus in key U.S. regions. The company’s revenue growth has been steady with a notable 20% net income increase in 2025 driven by segment diversification and effective funding mix. Despite sizable brokered deposits forming the bulk of funding and some debt maturities near term, strategic use of Federal Reserve discount window borrowings supports liquidity. Risks remain around interest rate volatility impacting net interest income and potential asset illiquidity. Close monitoring of loan portfolio performance and refinancing options will be critical for sustaining capital returns and operational flexibility.

Company Overview

Medallion Financial Corp is a specialized financial services firm operating four distinct lending segments: recreation equipment financing (RVs, boats, collector cars), home improvement loans (swimming pools, roofs, windows), commercial lending focused on manufacturing and construction industries, and taxi medallion lending concentrated in the New York City metropolitan area [S6][S9]. The company structures its funding through a diverse set of sources including brokered retail certificates of deposit (CDs), privately placed senior notes, SBA debentures via SBIC subsidiaries, trust preferred securities issued through a financing trust subsidiary, and Federal Reserve Discount Window borrowings secured by loan collateral [S1][S4][S14]. This diversified portfolio both stabilizes revenue streams by spreading credit concentration risk across consumer and commercial domains and geographically across major U.S. states where each segment demonstrates local specialization.

Historical Performance

Medallion Financial’s financial performance over recent years reflects stable growth amidst a complex operating environment characterized by regulatory scrutiny and evolving funding conditions:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 43 | 126 | +20.0% |

| 2024 | 36 | 116 | -34.9% |

| 2023 | 55 | 114 | +25.6% |

| 2022 | 44 | 109 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 1 | 10.5 |

| 2024 | 5 | 9.7 |

| 2023 | 0 | 16.1 |

| 2022 | 21 | 14.5 |

Source: SEC companyfacts cache [F1].

Net income recovered after a dip in 2024 driven partially by elevated provisioning needs amidst sector-specific stress but rebounded strongly (+20%) in 2025 as operational efficiencies improved alongside disciplined credit risk management [F1]. Operating cash flows rose steadily year-over-year indicating solid underlying loan collections; equity grew consistent with retained earnings supporting organic growth.

Segment Breakdown & Geographic Concentration

- Recreation Lending: Constitutes largest portion of consumer loans financing RVs (54%), boats (21%), collector cars (13%). Top states are Texas (17%) and Florida (10%) [S6][S9].

- Home Improvement: Primarily residential projects: swimming pools (32%), roofs (28%), windows (11%). Concentrated also in Florida (14%) and Texas (12%) [S6][S9].

- Commercial Lending: Focuses on manufacturing (63%), wholesale trade (11%), construction (10%). Predominantly allocated across California (20%), Wisconsin (12%), New York (11%) [S6][S9].

- Taxi Medallion Lending: Legacy niche operation centered on financing taxi medallions/assets mostly in the NYC metro area reflecting historical expertise but constrained by asset illiquidity risk since medallions have lost market value post-ride-sharing disruption [S6][S9].

Funding Profile & Liquidity

The company’s total outstanding debt stood at approx $2.4 billion as of end-FY25 comprised mainly of brokered deposits accounting for nearly $2.08 billion at an average cost of ~3.87% alongside privately placed notes ($146 million at ~8.12%), SBA-backed debentures ($85 million at ~3.98%), trust preferred securities ($33 million at ~6.12%), and Federal Reserve discount window borrowing ($50 million at ~3.75%) [S1][S4][S14].

Brokered CDs form the backbone of deposit funding — drawn nationally via brokerage arrangements that package smaller insured denominations — ensuring some stability given the absence of voluntary withdrawal rights even though they react sensitively to market rate changes . The Bank maintains additional unused credit lines up to $75 million with commercial banks providing contingency liquidity.

Notably, Medallion uses loan collateral pledging to the Federal Reserve discount window: initially utilizing home improvement loans as collateral providing nearly $293 million borrowing capacity with partial utilization at $50 million as of FY25-end; recently expanded embodiment includes $1 billion recreation loans pledged enhancing secured borrowing scope while managing cost-efficient liquidity access amid tightening credit markets [N1][N2][S1][S26].

Contractual obligations sketch out a notable debt maturity profile with approximately $1.4 billion due within two years predominantly tied to brokered CDs limiting rollover risk somewhat but highlighting refinance need over medium term without complete certainty on terms given macroeconomic volatility [S16].

Profitability & Returns

With reported net income hitting $43 million in FY25 against equity base around $409 million yields an approximate return on equity of about 10.5%, aligning with mid-tier specialty finance sector benchmarks prioritizing risk-adjusted returns over aggressive leverage plays [F1]. Operating cash flows remained robust above $120 million although buybacks shrunk back below $1 million after higher repurchase activity historically signaling cautious capital deployment strategies tuned to balance sheet strength preservation.

Dividend payments have been negligible or absent since before FY2018 reflecting reinvestment focus rather than shareholder distributions amidst regulatory settlement costs incurred earlier and evolving business model realignments [F1][S5]. The July 2025 redemption of Series F Preferred Stock totaling $46 million induced a one-time earnings charge yet improved capital efficiency dynamics over subsequent periods [S14].

Regulatory & Litigation Considerations

The company settled longstanding SEC litigation related to disclosures arising during its period as a business development company between 2015-2017 culminating in final judgment in May 2025 entailing a civil penalty expense previously accrued ($3 million) plus compliance undertakings without admission of fault or adverse financial impact beyond recognized reserves [S5]. Ongoing regulatory scrutiny remains part of operational risk but management views no material pending legal threats that could impact financial condition materially.

Future Growth Prospects & Risks

Medallion Financial’s future revenue trajectory will hinge critically on loan origination volumes across its specialized segments leveraging established dealer/contractor relationships particularly in rebound markets like residential improvements fueled partly by demographic trends favoring home refurbishment cycles nationwide especially in Sun Belt states with warmer climates driving pool installation activity [N2]. Growth levers also include modest expansion or evolving product mix within the commercial segment plus incremental fintech partnerships expanding borrower outreach.

However risks loom large including:

- Interest rate volatility could pressure net interest margins given rising cost of funds; immediate rate hikes may cause short-term income compression though modeled impacts imply manageable sensitivities assuming steady portfolio composition [S15].

- Refinancing sizable upcoming debt maturities requires favorable market access; any disruption could force higher costs or asset sales potentially below book value impairing earnings and liquidity buffers [S4].

- Asset illiquidity especially lingering taxi medallion loans constrains flexibility; adverse economic events might exacerbate loss provisions requiring careful portfolio surveillance.

- Regulatory changes or new compliance mandates could increase operational overheads or capital requirements impacting profitability metrics.

Absent explicit forward guidance from filings or recent earnings calls around exact milestones or forecast ranges ([N1],[N2]), watchpoints should concentrate on:

- Quarterly loan origination volumes by segment,

- Deposit cost trends amid competing regional banking wage pressures,

- Asset quality indicators including delinquencies/charge-offs,

- Capital raising initiatives such as preferred stock issuances or repo programs,

- Any changes to FDIC insurance rules impacting brokered deposit sourcing.

Conclusion

Medallion Financial Corp balances its unique niche lending expertise with comprehensive funding strategies that provide resilience yet expose it to typical specialty finance cyclical headwinds related to rising rates and liquidity management complexities. The firm’s methodical capital approach reflected in moderate buybacks coupled with incremental deposit diversification showcases prudence while incremental pledging of collateralized loan portfolios unlocks innovative secured borrowing avenues supporting operational agility under pressure scenarios.

Increasingly important will be strategic judgment around refinancing sizable near-term maturities as well as continued navigation of legacy risks from taxicab medallion assets alongside seizing growth opportunities from expanding consumer discretionary lending sectors concentrated geographically where demand fundamentals remain favorable.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments