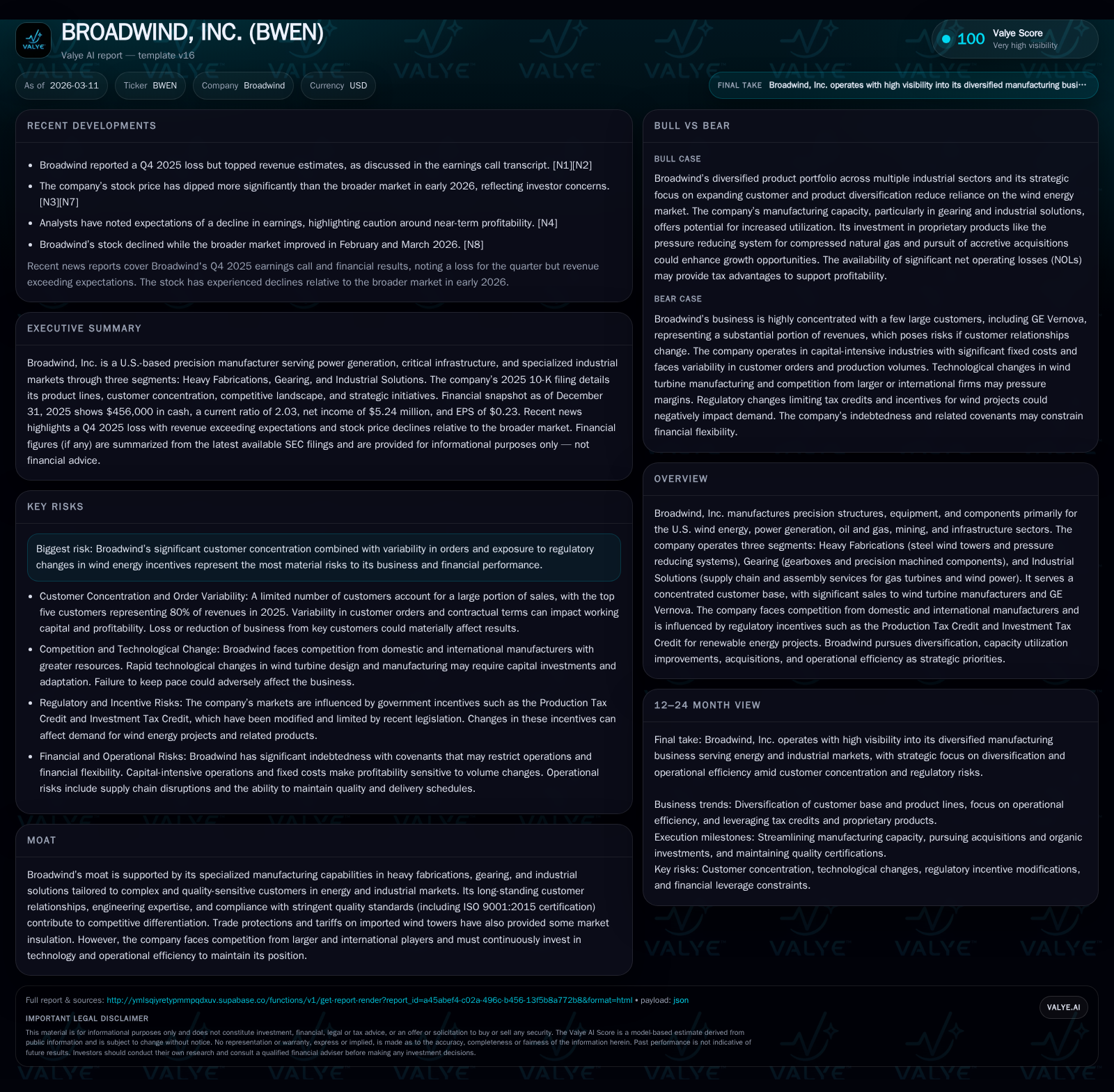

Broadwind’s Strategic Diversification and Operational Efficiency Confront Customer Concentration and Technological Shifts

Broadwind's recent financial improvement stems from operational strategies amid significant customer concentration and industry evolution.

Broadwind, Inc. demonstrated notable recovery in operating income and net income in 2025 after losses earlier in the decade, driven by focused operational improvements and streamlining of its Heavy Fabrications segment. The company remains heavily reliant on a concentrated customer base—five clients representing 80% of revenues—particularly GE Vernova, exposing it to demand variability risks. Growth opportunities are linked to capacity utilization enhancement, diversification efforts across segments, and selective acquisitions, but technological changes in wind turbine manufacturing and regulatory shifts introduce uncertainty. Despite improving profitability, Broadwind faces cash flow challenges and substantial debt that could limit financial flexibility.

Company Overview

Broadwind, Inc. is a precision manufacturer specializing in complex structures, equipment, and components primarily across U.S.-based energy sectors including wind power generation, oil & gas (O&G), mining, power generation, and critical infrastructure. Its operations are divided into three key segments: Heavy Fabrications (steel wind towers and pressure reducing systems), Gearing (gearboxes and precision-machined components), and Industrial Solutions (supply chain management and assembly services for gas turbines and wind power) [S1][S15].

Founded in 1996 as Blackfoot Enterprises before rebranding multiple times culminating in the current name change in 2020 reflecting diversified product lines beyond wind energy [S1], Broadwind has focused on building specialized advanced manufacturing capabilities delivering high-reliability products tailored to stringent quality standards mandated by a small number of large industrial clients.

Historical Performance and Past Growth Drivers

Broadwind's revenue has hovered near $147 million since at least 2017; however, precise recent revenue figures beyond this date are unavailable. Despite stable top-line indications historically, profitability surged after a multi-year downturn:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 5 | -15 | 9 | 4 | +355.0% |

| 2024 | 1 | 14 | 4 | 4 | -84.9% |

| 2023 | 8 | -7 | 2 | 6 | +178.6% |

| 2022 | -10 | 17 | -2 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -19 | 7.9 |

| 2024 | 10 | 1.9 |

| 2023 | -13 | 13.7 |

| 2022 | 14 | -21.0 |

Source: SEC companyfacts cache [F1].

Operating income more than doubled year-over-year in FY25 (+104.8%) with net income up over threefold (+355%) compared to FY24 [F1]. The prior years exhibited significant earnings volatility including losses in FY22 followed by recovery starting FY23.

This financial improvement correlates with operational streamlining measures such as divesting the Manitowoc industrial fabrications site in September 2025 to centralize production at Abilene—a facility capable of producing up to approximately 220 steel towers annually sufficient for over 800 MW of wind power capacity—which aligns with management efforts to improve capacity utilization across segments [S11][N2].

Segment Dynamics

Heavy Fabrications: Historically the core wind tower manufacturing business contributes over half of revenues but has been undergoing rationalization to optimize output quality versus volume. The proprietary mobile modular pressure reducing systems (PRS) targeting compressed natural gas distribution present niche growth channels leveraging virtual pipeline concepts [S11].

Gearing: This segment caters broadly to energy markets including natural gas turbines alongside onshore/offshore O&G drilling equipment as well as material handling sectors. It benefits from longstanding expertise spanning a century in precision gear manufacturing with aerospace-level certifications (AS9100D obtained August 2024) enhancing credibility for complex OEM applications [S1][S20].

Industrial Solutions: Primarily supports natural gas combined cycle markets as well as providing on-site integration kitting for wind power internal assemblies addressing supply chain localization trends among turbine OEMs challenged by lead times and import reliability issues [S10][S20].

Customer Concentration Risks

Broadwind operates within highly concentrated end markets often dominated by few large players. In particular:

- GE Vernova alone represented greater than 10% of consolidated revenues in both FY24 and FY25.

- Top five customers accounted for approximately 80% of revenues in fiscal year ending December 31, 2025.

- Wind turbine manufacturing itself is concentrated with two largest producers capturing approximately 88% US market share per Wood Mackenzie data [S4][S16].

The company's reliance on a narrow customer base exposes earnings to significant variability from order timing shifts or contract renegotiations leading to production inefficiencies impacting fixed cost absorption and profit margins. Certain customers retain contract provisions allowing cancellation or restructuring with limited penalty which elevates operational uncertainty [S4][S7].

Moreover, ongoing consolidation among turbine manufacturers could amplify these concentration risks or disrupt supplier relationships moving forward [S21].

Technological Evolution & Operational Challenges

The wind turbine market is undergoing rapid technological change—including scaling turbine size particularly offshore installations—that increase complexity in tower fabrication possibly requiring substantial capital expenditures for new equipment. Some manufacturers are shifting toward concrete-based towers partially or fully replacing steel structures thus potentially reducing Broadwind’s addressable market without adaptation [S8].

Broadwind is actively evaluating incorporation of cutting-edge technologies such as generative AI and machine learning aimed at improving product design insights and operational efficiencies although these impose emergent cybersecurity vulnerabilities and regulatory risks that remain difficult to quantify fully at present [S8][S25].

Strategic Growth Prospects

Management's stated priorities highlight:

- Diversification: Attempts to reduce dependence on wind sector (51% of sales in FY25 down from about 70% in FY20) via expanding product offerings across various segments targeting mining equipment manufacturers, gas turbine OEMs/aftermarkets, infrastructure markets.

- Capacity Optimization: Leveraging underutilized plant capacity especially within gearing and industrial solutions segments assuming favorable labor market conditions.

- Acquisitions & Organic Investments: Targeting bolt-on acquisitions that expand capabilities or geographic reach aligned with manufacturing competencies.

- Operational Improvements: Streamlining front-end forecasting/planning processes; employing continuous improvement/lean practices; enhanced supply chain discipline; schedulers software deployment; advanced product quality initiatives aimed at improving output consistency while reducing costs.

- Product Development Framework: Utilizing stage gate model for rigorous project evaluation accelerating commercialization of new variants like enhanced PRS units suited for compressed natural gas distribution expansion [S9][S15].

However the timing and success of these initiatives are contingent upon macro demand drivers including regulatory incentives like Production Tax Credit (PTC) or Investment Tax Credit (ITC), industry consolidation trends affecting OEM purchasing patterns plus global raw material pricing volatility especially steel inputs which Broadwind partially passes through via directed buys negotiated by customers [S21].

Financial Health & Capital Allocation

Despite improved profitability metrics,

- Operating cash flow was negative roughly -$15.4 million in FY25 contrasting previous positive inflows indicating working capital buildup predominantly due to declining customer deposits embedded in current liabilities rising slower than accounts receivable/inventory increases creating working capital drag.

- Capital expenditures remained stable around $3.6 million consistent with maintenance/reinvestment level rather than aggressive capacity expansion.

- Equity base strengthened incrementally reflecting retained earnings accrued during profitable years leading to an approximate return on equity near 7.9% in FY25 defined as net income divided by equity at period end.

- No recent share buybacks were reported since levels last noted several years ago circa FY2014.

- Liquidity position shows a current ratio just above two suggesting balanced near-term solvency but sizable debt service obligations entail risk if operating cash flows fail to stabilize or decline unexpectedly due to external shocks.[F1][S12]

The company carries material indebtedness subject to restrictive covenants affecting leverage ratios limiting strategic flexibility especially under volatile market conditions but management expresses confidence through projected internal cash flows bolstered by available financing sources sufficing currently anticipated needs.[S12][S13]

Competitive Landscape & Certification Advantages

In the domestic wind tower market Arcosa Inc. is a notable rival alongside international players such as CS Wind South Korea/Germany origin providers despite tariff protections stemming from anti-dumping duties levied on imports from China/Vietnam extended most recently through October 2029. Gearing businesses are affected by industry consolidations countered partly by trends favoring domestic suppliers due to sourcing scrutiny post-pandemic supply chain disruptions.[S16][S21]

Broadwind attained ISO9001:2015 certification across core sites with Gearing segment achieving AS9100D standard enabling aerospace-grade component production enhancing credibility for high-end custom orders while divisions passed International Traffic Arms Regulations registrations supporting defense contracts highlighting stringent IP security compliance.[S19][S20]

Risks Summary

- Customer Concentration & Order Volatility: Heavy reliance on few customers magnifies any order reduction’s impact; some contracts allow cancellations before production leading to revenue unpredictability.

- Technological Adaptation: Failure to timely invest/adapt for evolving turbine designs or new materials could render assets obsolete.

- Regulatory Dependence: Changes or phase outs of US renewable energy incentives may reduce demand pipeline.

- Labor Market Tightness: Skilled labor scarcity coupled with inflationary wage pressures may curtail margin gains or constrain capacity realization.[S17]

- Cybersecurity Threats: Increased reliance on IT systems including AI heightens exposure risk potentially disrupting operations or leaking IP.[S23]

- Environmental Compliance Costs: Stricter health/safety/environmental laws may increase operating expenses.[S26]

- Legal Disputes & Warranty Exposure: Potential litigation related to intellectual property infringement claims or warranty matters could impose unpredictable costs.[S14][S23]

- Leverage Constraints: Debt covenants restrict maneuvering room impacting ability to respond tactically amid unforeseen challenges.[S12][S13]

Analysis: What to Watch Going Forward

Absent explicit forward guidance disclosed publicly,[N1] monitoring will center around:

- Quarterly order backlogs trends particularly from top wind OEMs like GE Vernova as bellwethers for near-term revenue visibility.

- Progress reports on diversification efforts reducing percentage revenue dependence on top five customers.

- Operational efficiency metrics including capacity utilization rates at Abilene fabrications plant post-restructuring.

- Adoption milestones related to new technologies integration such as AI-driven manufacturing analytics or supply chain automation upgrades.

- Free cash flow evolution reflecting working capital normalization necessary for debt servicing sustainability given negative CFO backdrop despite profits.

- Macroeconomic/regulatory developments influencing renewable energy project pipelines along with steel commodity price trajectories impacting input costs/pass-through abilities.

- Labor dispute developments given union contracts covering ~20% workforce extend through late decade reinforcing operational stability assumptions.[S17]

- Potential accretive acquisitions announcements aligned with stated strategic criteria expanding product breadth without over-leveraging balance sheet.[N2]

Conclusion

Broadwind stands at an inflection juncture characterized by recovering profits after years marked by volatility while contending simultaneously with structural industry shifts and persistent concentration risks. Its strategic emphasis on diversification coupled with operational discipline aims to cement sustainability though execution risk remains nontrivial given market dependencies. Financially cautious allocation amidst debt headwinds continues necessitating close scrutiny of cash flow trends relative to capex commitments reinforcing need for balanced growth versus liquidity preservation trade-offs. Ongoing investments in technology compliance certifications reinforce competitive differentiation yet maintaining pace within evolving turbine technology ecosystems remains critical. Overall Broadwind embodies a niche specialty manufacturer embedded within dynamic renewable energy transition forces where winning requires agile adaptation alongside prudent management of concentrated client relationships.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments