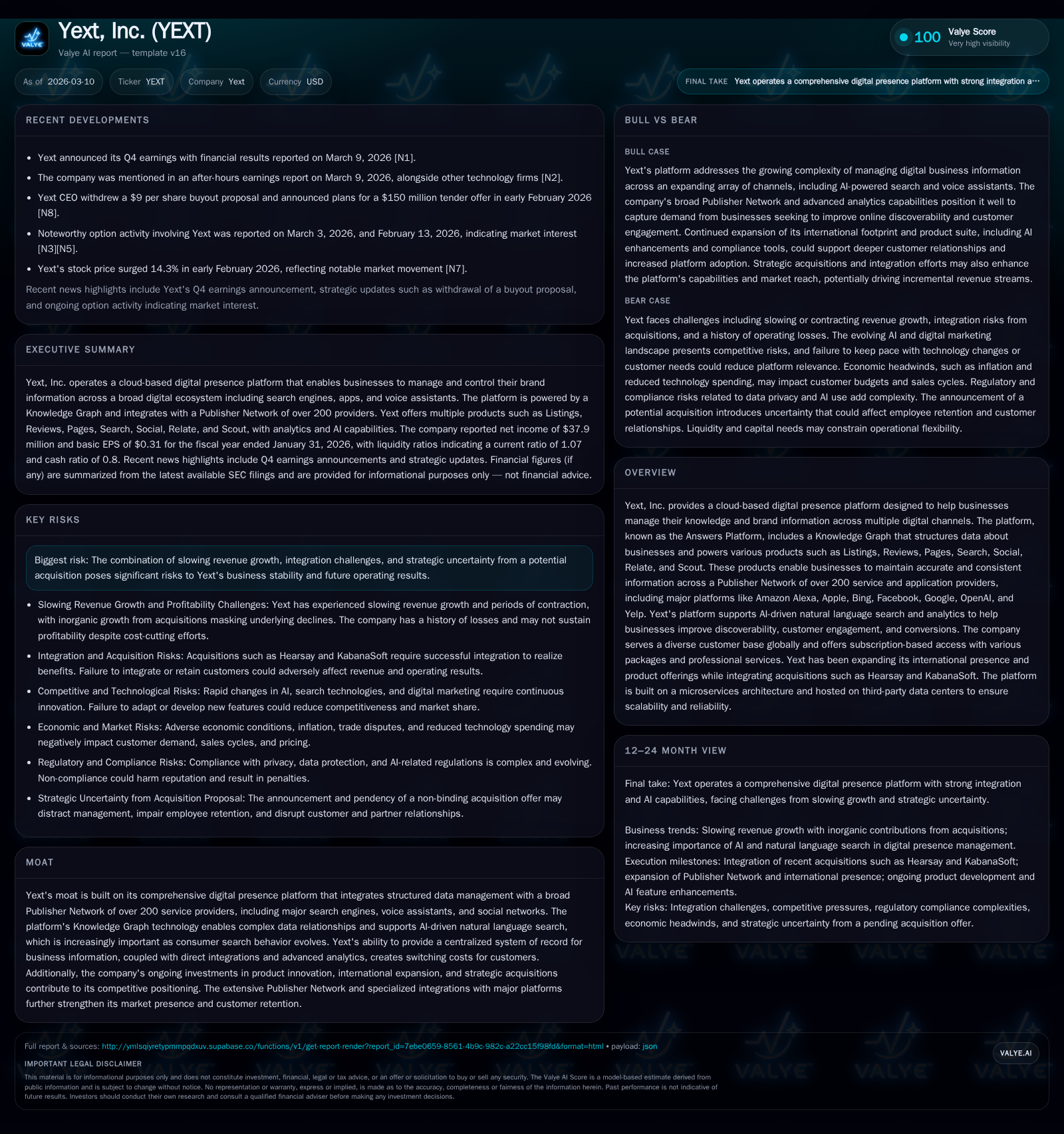

Yext's Rebound: From Prolonged Losses to Operating Profit on AI-Driven Digital Presence

Yext achieved operating profitability in fiscal 2026, pivoting from years of losses amid a transforming digital search landscape powered by AI.

Yext, Inc. has transformed its financial trajectory by turning profitable in the latest fiscal year after successive years of operating losses. The company’s cloud-based Answers Platform leverages a Knowledge Graph and a broad Publisher Network enabling businesses to maintain accurate digital presence across over 200 platforms, including major voice assistants and AI search engines. Increasing reliance on AI, natural language search, and consumer demand for actionable, consistent business information underpin Yext’s growth prospects. However, challenges remain from slowing revenue growth, complex sales cycles, regulatory risks around AI and data privacy, and the need to continuously innovate against entrenched competitors. Capital allocation has increasingly favored buybacks alongside positive cash flows.

Historical Financial Performance

Yext’s financial journey over the past four years illustrates a dramatic turnaround in profitability metrics after enduring recurring losses. The company swung from an operating loss of nearly $65 million in fiscal year 2023 to generating $44.5 million in operating income in fiscal 2026. Similarly, net income improved from a sizable negative $65.9 million to a positive $37.9 million over the same span [F1]. This turnaround is complemented by steadily increasing operating cash flow (from $17.9 million in FY2023 to $55.8 million in FY2026) alongside modest capital expenditures below $3 million annually since FY2024.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 38 | 56 | 45 | 3 | +235.5% |

| 2025 | -28 | 50 | -32 | 2 | -962.7% |

| 2024 | -3 | 46 | -6 | 3 | +96.0% |

| 2023 | -66 | 18 | -65 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 67 | 53 | 23.8 |

| 2025 | 18 | 48 | -18.2 |

| 2024 | 23 | 43 | -1.8 |

| 2023 | 77 | 12 | -51.5 |

Source: SEC companyfacts cache [F1].

Table reflects operating income turnaround primarily driven by expanding efficiencies and product traction [F1].

While top-line revenue figures are unavailable for recent years in [F1], SEC filings note that revenue growth has slowed or contracted recently due to subscription revenue recognition timing and challenging market conditions [S1][S2]. This dynamic leads to volatility between bookings and reported revenue.

Business Model and Competitive Positioning

Yext operates a cloud-based Answers Platform centered on its structured Knowledge Graph—a centralized database organizing detailed business information such as locations, hours of operation, services offered and FAQs [S4][S5]. This data is propagated across an extensive Publisher Network comprising over 200 service providers including Amazon Alexa, Apple Maps & Siri, Bing, Facebook, Google Search/Maps/AI (Gemini), Yelp and OpenAI-powered chat interfaces [S4][S5].

Core platform functionalities include:

- Listings Management: Ensures consistent business profiles with instant updates across multiple external sites.

- Review Management: Aggregates and facilitates response to consumer reviews.

- Pages: Creates scalable landing pages dynamically updated from core business data.

- Search & AI Integration: Supports natural language queries reflecting evolving consumer search behavior.

- Analytics (Scout): Benchmarks performance against competitors at granular geographic levels for actionable insights.

The rise of AI-driven natural language search reshapes how consumers discover businesses; Yext’s multi-algorithm approach combined with schema.org-compliant structured markup supports this shift better than many competitors reliant on fragmented manual updates or legacy systems [S10][S14][S16][S23].

Competitive pressures persist from established digital marketing players offering local listings or reputation management solutions alongside emerging enterprise search providers targeting AI-powered discovery [S14][S23]. Yext distinguishes itself through ease of integration via APIs and continuous innovation delivered multiple times per year by its global R&D teams [S16][S17]. Strong direct relationships with platform providers foster proprietary workflows that enhance switching costs.

Growth Prospects

Key growth avenues include:

- Customer Base Expansion: Targeting broader penetration beyond U.S. markets where localized integrations exist but can be deepened [S6].

- Cross-Selling Additional Products: Upselling complementary modules like Pages or Social engagement technology following initial product adoption [S6].

- International Scaling: Established presence in countries including U.K., Germany France and Japan with plans for further expansion [S6].

- Publisher Network Extension: Ongoing addition of industry vertical-specific platforms captures niche discovery needs [S7].

- Technology Innovation: Incorporating generative AI/chatbot capabilities into offerings supports emerging digital touchpoints such as conversational commerce or automated support [S4][S6][S24].

Growth is moderated by risks including subscription renewal pressure amid pricing dynamics and economic headwinds impacting tech budgets [S1][S2]; complexity integrating acquisitions as M&A continues [S12]; lengthening sales cycles for enterprise deployments causing revenue lumpiness [S1]; plus regulatory uncertainties around expanding global AI governance frameworks potentially increasing compliance costs or constraining product rollouts [S18][S20][F1].

Milestones & Outlook Considerations

Yext has not provided explicit forward guidance recently but key investor focus areas include:

- Renewal rates among major customers given dependency on subscription models.

- New customer additions especially outside North America.

- Progress toward expanding the Publisher Network beyond ~200 partners.

- Product launches embedding enhanced AI capabilities into natural language responses.

- Outcomes of acquisition attempts or strategic partnerships impacting scale economics.

- Effects of evolving regulations such as the EU AI Act or U.S. state-level data privacy laws on operational flexibility [N1][N5][S18][S20].

Quarterly disclosures will be important to track incremental bookings trends relative to recognized revenue due to subscription accounting impacts.

Capital Allocation & Financial Returns

With restored profitability in FY26 after years of losses [F1], Yext generated approximately $53 million in free cash flow (operating cash flow minus capital expenditures), signaling improved financial discipline [F1]. The company held cash & equivalents near $154 million at fiscal year-end with current assets slightly exceeding liabilities (current ratio ~1.07), indicating sound liquidity [F1].

Share repurchases accelerated significantly to about $67 million in FY26 compared to roughly $18 million the prior year—a potential indicator of management confidence or shareholder value enhancement amid muted organic revenue growth prospects [F1]. Dividends are not reported; capital returns currently emphasize buybacks.

Return on equity approximated near 24% for FY26 reflecting earnings momentum combined with balance sheet strength [F1]. The company appears balancing historical investment into platform development against newly profitable operations with disciplined spending.

Strategic Risks & Industry Challenges

Risks impacting Yext's outlook include:

- Potential ongoing revenue growth deceleration due to subscription recognition timing coupled with macroeconomic factors affecting marketing spend [S1][S2].

- Integration challenges from acquisitions risking innovation pace or organizational focus as noted historically [S12].

- Regulatory constraints related to personal data handling (HIPAA for health sector clients), privacy regimes (GDPR), and emerging AI content regulation may increase compliance costs or legal exposures [S12][S18][F1].

- Intensifying competition from entrenched ecosystem players investing heavily in similar capabilities could pressure margins or erode customer bases [S14][S23].

- Economic uncertainties leading enterprise buyers to exercise caution given long sales cycles typical for multi-location software platforms servicing distributed clients [S1][N5].

Conclusion & What To Watch

Yext showcases a transition from sustained losses into operational profitability driven by advanced technology leveraging shifting consumer preferences toward AI-enabled search across fragmented digital ecosystems. The company benefits from network effects linked to deep publisher integrations combined with flexible SaaS offerings addressing complex knowledge management needs.

Future success depends on navigating sector competition; compliance with evolving global AI/data privacy regulations; managing economic cyclicality impacting subscription renewals; plus continuously upgrading products—especially integrating generative AI—to avoid commoditization.

Key metrics for investors include renewal rates among large customers; new contract wins outside North America; velocity of Publisher Network expansion; plus cost control preserving healthy free cash flow alongside investments into R&D.

Upcoming quarterly results will be crucial gauges of whether Yext can sustain profitable growth amid shifting technology standards and evolving client demands within competitive digital marketing landscapes.

DISCLAIMER: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding any security. It reflects information available as of March 10th, 2026 derived from public filings and news sources without speculative assumptions beyond disclosed facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments