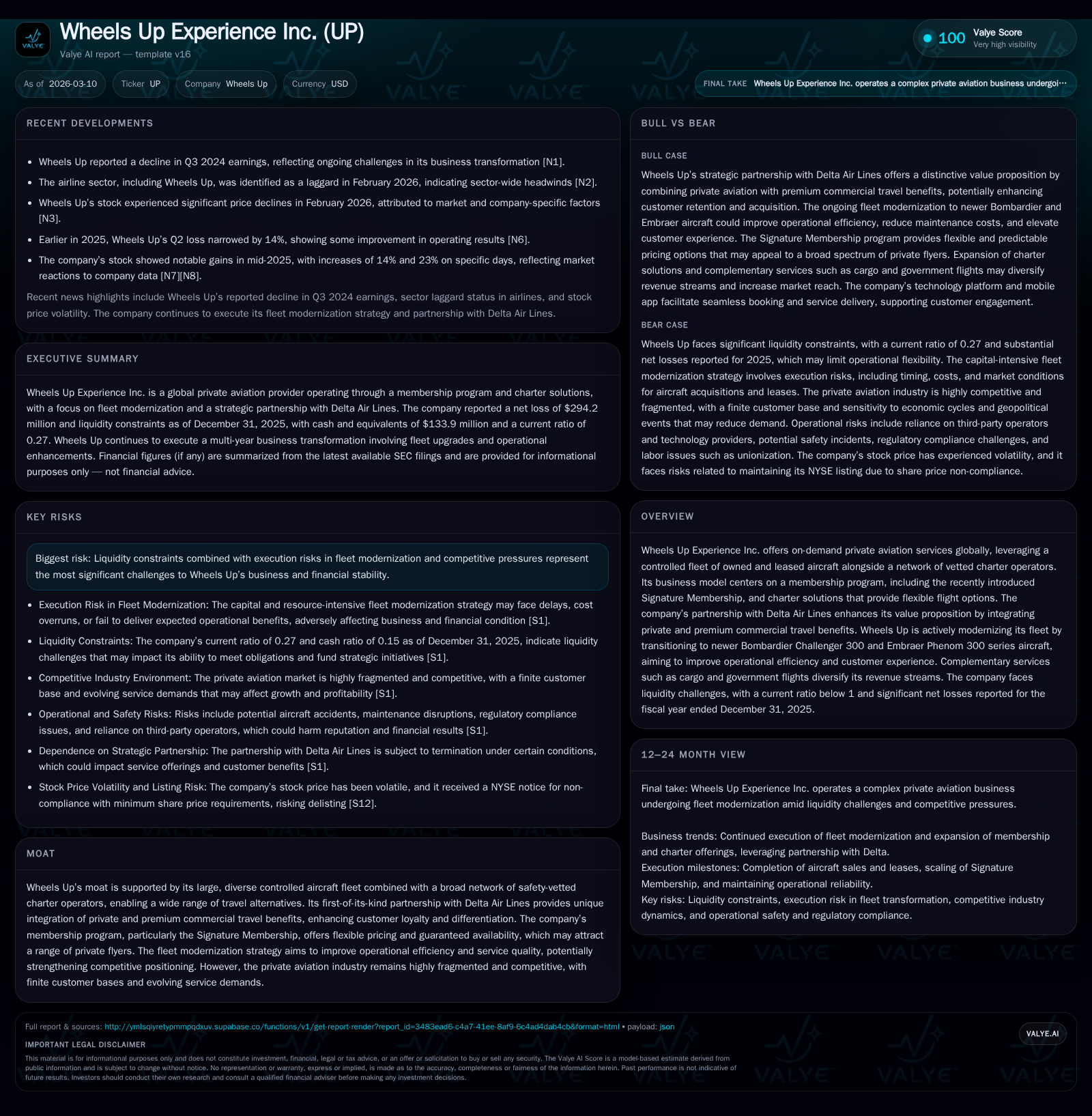

Wheels Up's Transition: Fleet Modernization and Membership Refresh Shape Future Prospects

Wheels Up Experience Inc.'s ambitious fleet and membership revamps face financial headwinds, testing the balance between growth aspirations and liquidity constraints.

Wheels Up Experience Inc. has embarked on a significant transformation involving its controlled aircraft fleet modernization and the launch of a new Signature Membership program. This strategy aims to expand its member base while enhancing operational efficiency and customer experience, notably through integration with Delta Air Lines’ premium offering. Despite roughly 21% year-over-year improvement in operating income by fiscal year 2025, the company continues to realize substantial net losses and negative operating cash flows, reflected in a precariously low current ratio of 0.27. Capital allocation priorities remain focused on fleet investment, with minimal share repurchases and no dividends, reflecting a defensive stance amid persistent liquidity pressures. The company’s future hinges on successful execution of its modernization plan, deeper member engagement, and maintaining strategic partnerships within an intensely competitive private aviation market.

Strong Growth Trajectory Tempered by Persistent Operating Losses

Wheels Up Experience Inc.’s recent history reflects steady improvement in operating performance alongside ongoing net losses and liquidity challenges inherent to its multi-year business transformation. From fiscal year (FY) 2023 through FY2025, operating income losses narrowed from approximately -$444 million to -$203 million—a roughly 21% year-over-year improvement reflecting operational efficiencies or revenue mix shifts [F1]. Nevertheless, net income remained negative at about -$294 million for FY2025 amid high fixed costs associated with fleet operations and partnership arrangements.

Operating cash flow (CFO) was negative $166 million for FY2025 as the company continued heavy investments alongside working capital needs linked to prepaid membership funds and charter services [F1]. This sustained cash burn highlights ongoing capital intensity and pressure on liquidity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -294 | -166 | -203 | 94 | +13.4% |

| 2024 | -340 | -78 | -259 | 123 | +30.3% |

| 2023 | -487 | -665 | -444 | 20 | -116.7% |

| 2022 | -225 | -231 | -222 | 84 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 2 | -260 | 75.0 |

| 2024 | 0 | -201 | 168.0 |

| 2023 | 0 | -685 | -500.4 |

| 2022 | 8 | -314 | -89.3 |

Source: SEC companyfacts cache [F1].

Table: Wheels Up Annual Financial Performance illustrating gradual margin improvements offset by continued net losses and heavy cash usage [F1]

Equity declined sharply from positive $252 million in FY2022 to negative $392 million by end-2025 due to accumulated losses and balance sheet pressures [F1]. Liquidity remains constrained with current assets of approximately $249 million against current liabilities exceeding $907 million resulting in a low current ratio of about 0.27—indicating significant short-term funding stress that could affect operational flexibility [F1][S5][S8].

Signature Membership Launch and Fleet Modernization Drive Growth Strategy

A key strategic initiative is the September 2025 launch of the Signature Membership program coinciding with the ongoing fleet modernization effort featuring Bombardier Challenger 300 and Embraer Phenom 300 aircraft series [S1][N1]. This membership model introduces two access plans—Dynamic Access Plan with discounted hourly rates based on dynamic pricing, and Fixed Access Plan offering predictable hourly rates—both designed to enhance flexibility while guaranteeing aircraft availability across contiguous U.S., border areas of Canada/Mexico, plus select international destinations such as the Bahamas [S1].

This revamped membership approach aims to simplify private flying cost structures while maintaining premium service levels and leveraging newer aircraft that promise improved reliability and operational efficiency compared to legacy jets [S1][N1]. The transition includes pilot retraining for newer fleets which increases near-term labor costs but targets long-term savings.

Delta Partnership Strengthens Competitive Positioning

Wheels Up’s partnership with Delta Air Lines integrates private aviation access with commercial airline premium benefits—a unique value proposition among private aviation providers [S1][N1]. Through this alliance, members can earn Delta Diamond Medallion status based on flight spend thresholds enhancing loyalty by bridging private jet travel with commercial upgrades and lounge access.

Joint marketing initiatives amplify customer acquisition efforts while Wheels Up’s controlled fleet ensures service reliability complementing Delta’s network reach—creating a competitive moat amidst fragmented industry players reliant on variable third-party charter capacity [S14].

Financial Health Under Strain Amid Capital Structure Constraints

Despite strategic advances, Wheels Up confronts significant financial headwinds including tight liquidity conditions and capital structure restrictions.[F1][S5]

The company faces substantial working capital pressure given current liabilities exceed current assets by over $650 million as of December 31, 2025, limiting operational flexibility [F1]. Debt agreements impose covenants restricting equity issuance without lender approval, share repurchases, dividend payments, asset disposals, debt incurrence limits, all curbing financial maneuverability [S5][S8]. Non-compliance risks triggering defaults that could accelerate debt repayment demands or collateral repossession primarily involving owned aircraft critical for revenue generation [S8].

Raising additional financing under favorable terms is challenged by volatile earnings forecasts combined with negative equity position which raises dilution concerns given prior usage of at-the-market equity offerings as funding sources [S13].

Capital Allocation Prioritizes Fleet Investment Over Shareholder Returns

Capital expenditures remained focused on fleet renewal totaling approximately $93.6 million in FY2025—down from $122.8 million in FY2024 but still substantial—primarily dedicated to Bombardier Challenger and Embraer Phenom aircraft acquisitions aligned with modernization objectives [F1].

Conversely, share repurchases were negligible at around $1.6 million for FY2025 while no dividends were declared consistent with a strategy emphasizing reinvestment into operational capabilities rather than shareholder payouts under current loss-making conditions [F1][S22].

Operational Risks Amid Market Competition

The company faces multiple execution risks including the complexity of fleet modernization requiring significant capital outlays and pilot retraining amidst industry-wide pilot scarcity affecting labor costs [S15]. Dependence on third-party charter operators exposes Wheels Up to service disruption risks if counterparties fail or terminate agreements unexpectedly during periods of constrained aircraft supply [S7].

Technology infrastructure relies heavily on third-party cloud services critical for flight management systems posing cybersecurity risk exposures that could impair member experiences if incidents occur [S20]. Additionally, competition from ultra-high-net-worth bespoke operators alongside fractional ownership models intensifies market pressure challenging Wheels Up’s membership-based approach [N3]. Macroeconomic uncertainties further threaten discretionary travel demand volatility as learned during pandemic disruptions warranting cautious outlooks [S18].

Key Milestones To Monitor Execution Progress

Several upcoming events will provide insight into the company’s ability to execute its transformation:[N1][N2][S3]

- Delivery timeliness for new Bombardier Challenger 300 and Embraer Phenom jets impacting capacity expansion.

- Member adoption rates for Signature Membership plans reflecting market acceptance.

- Quarterly earnings results signaling margin trajectory towards break-even or continued losses.

- Changes in liquidity profile including refinancing efforts alleviating covenant pressures.

- Stability or evolution within Delta partnership agreements supporting retention.

- Resolution progress on legal matters such as the Fleet Guaranteed Revenue Program litigation influencing deposit recoveries.[S9]

Monitoring these factors will clarify management effectiveness navigating growth ambitions amid persistent challenges.

This analysis synthesizes publicly available filings, disclosures, news reports, and financial data without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments