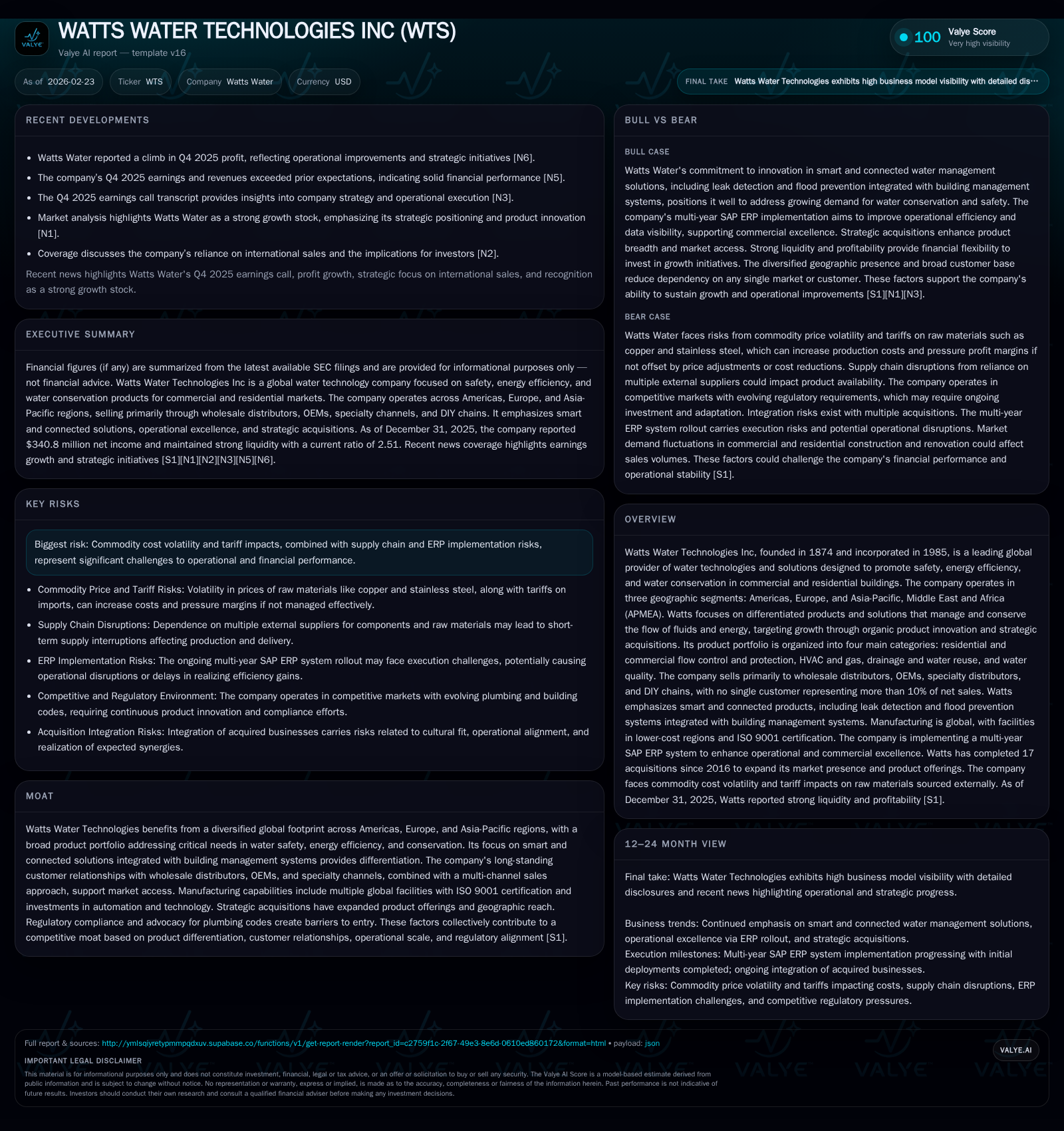

Watts Water Technologies' Strategic Evolution and Growth Outlook

Watts Water Technologies demonstrates robust financial growth supported by innovation in smart water solutions and ERP modernization, while navigating commodity and supply chain risks.

Founded in 1874, Watts Water Technologies has solidified its position as a global leader in water technologies, emphasizing safety, energy efficiency, and conservation. The company’s recent fiscal year 2025 results reveal meaningful gains in operating income (+14.8%), net income (+17%), and operating cash flow (+11.3%), driven by product innovation and geographic diversification. Strategic ERP system deployment aims to bolster operational efficiency amid challenges from commodity price volatility and tariff pressures. Capital allocation policy balances investment in manufacturing capabilities with steady share repurchases and healthy returns on equity near 17%. Monitoring of future ERP rollouts and continuation of smart connected product initiatives remain key metrics for assessing growth momentum.

Historical Performance and Growth Drivers

Watts Water Technologies completed fiscal year (FY) 2025 exhibiting a clear trajectory of financial strength underscored by healthy operating leverage and expanding profitability. Operating income reached $448.1 million for the year ended December 31, 2025—a notable increase of 14.8% compared with $390.4 million in FY2024 [F1]. This gain signals effective absorption of inflationary pressures alongside revenue growth likely propelled by new product introductions and geographic market penetration.

Net income expanded even more markedly to $340.8 million, up 17% year-over-year from $291.2 million in FY2024 [F1], illustrating solid net margin expansion achieved through disciplined cost management coupled with pricing actions amidst raw material cost shifts.

Operating cash flow (CFO) advanced from $361.1 million to $402 million (+11.3%) [F1], delivering robust internal liquidity that supported an elevated capital expenditure (capex) level of approximately $45.7 million, marking a strong capex increase of nearly 30% year-on-year aimed at enhancing production capability and automation investments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 341 | 402 | 448 | 46 | +17.0% |

| 2024 | 291 | 361 | 390 | 35 | +11.1% |

| 2023 | 262 | 311 | 351 | 30 | +4.2% |

| 2022 | 252 | 224 | 315 | 28 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 16 | 356 | 16.8 |

| 2024 | 17 | 326 | 17.1 |

| 2023 | 16 | 281 | 17.3 |

| 2022 | 69 | 196 | 19.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable; buyback data discussed separately.

This progression affirms Watts’ ability to marry organic product innovation with scaling efficiencies across its global footprint to drive sustained earnings growth.

Product Innovation and Smart Solutions Integration

Watts is channeling considerable R&D into evolving its portfolio towards increasingly intelligent water management solutions deeply integrated with building ecosystem technologies [S8][S16][S18]. Core offering categories encompass residential/commercial flow control & protection products, HVAC/gas heating solutions, drainage & water reuse systems, plus water quality devices.

Among their technological advances are smart sensors embedded in critical flow control products that detect leaks, floods, or freezing conditions—alerting building management systems (BMS) or personal devices thereby enabling rapid mitigation responses before damage escalates [S8][S18]. These capabilities significantly enhance water safety while conserving resources.

The incorporation of Nexa—a proprietary intelligent water management platform—marks a strategic impetus consolidating hardware integrations with software controls focused on operational efficiency, user experience enhancements, and regulatory compliance mandates relating to plumbing codes worldwide [S18]. The company’s commitment manifests through expansions in electronics development capabilities alongside enduring emphasis on ISO 9001-certified manufacturing precision ensuring product reliability.

Leak detection products servicing both residential units and multifamily or commercial properties represent particularly high-value segments given rising awareness around water damage costs and sustainability priorities.

This smart enabling approach not only differentiates Watts amid competing legacy mechanical-only suppliers but positions it as a preferred solutions provider encompassing end-to-end fluid regulation through digital connectivity.

Geographic Segments and Customer Channels Overview

Watts operates across three global geographic divisions: Americas; Europe; Asia-Pacific, Middle East & Africa (APMEA), leveraging diversified sales channels that support robust market coverage [S4][S5][S7][S15].

- Americas segment consistently contributes a significant majority (~62-66%) of net sales annually.

- Europe provides a stable mid-tier contribution with specialized OEM relationships particularly around boilers, radiant heat systems.

- APMEA targets emergent market penetration focusing on HVAC-related OEMs for water heating and air conditioning applications.

The company’s multi-channel sales strategy encompasses:

- Wholesale distributors, approximately two-thirds of total net sales (~66%), serving plumbing/heating contractors; this channel ensures deep commercial market penetration for both residential and commercial project needs.

- Specialty distributors capturing roughly one-fifth (~21%) of revenues focused on high-efficiency boilers, leak detection solutions, specialty flooring/tile products.

- Original Equipment Manufacturers (OEMs) comprise about ~10%, supplying branded components integrated by manufacturers primarily in HVAC equipment sectors across all regions.

- DIY retail chains, although a smaller portion (~3%), provide consumer access channels for valves and certain water quality products vital for residential replacement markets.

No single customer accounted for more than 10% of total net sales affirming diversified risk exposure while top ten customers represented about one-quarter (23%-24%) indicating broad base reliance rather than concentration risk [S4][S5][S15]. Sales shifts by channel remain low single-digit percent changes year-over-year signaling resilient demand amid ongoing global macro uncertainties.

ERP Implementation as a Catalyst for Operational Excellence

In pursuit of streamlined operations supporting its growth initiatives, Watts embarked on a multi-year phased implementation of the SAP Enterprise Resource Planning (ERP) system spanning Americas and APMEA regions starting in calendar year 2024 [S4].

By the end of FY2025, the company successfully deployed the platform at key manufacturing and distribution facilities within the Americas segment establishing operational blueprints encompassing inventory management, production scheduling articulation, procurement automation, and data analytics convergence.

This ERP backbone upgrade is critical not only for unlocking productivity but also enhancing enterprise-wide data visibility facilitating tighter commercial alignment with customers alongside Lean manufacturing continuous improvement initiatives already underway at ISO-certified plants globally [S8].

Future rollouts scheduled for execution throughout FY2026 will extend these efficiencies into APMEA locations enabling standardized processes that underpin Watts’ aspirations for scale economies balanced with agility in supply chain responsiveness.

Such enterprise systems modernization is a recognized value inflection point within industrial manufacturing verticals where disparate legacy systems traditionally impede rapid decision-making or introduce costly redundancies.

Risks from Commodity Volatility and Tariffs

Commodity price fluctuations pose material risk vectors especially given Watts’ dependence on copper, brass, cast iron, stainless steel among other raw materials sourced internationally [S9][S28]. Recent tariff impositions on imports originating mainly from Canada, China, Mexico further exacerbate cost inflation dynamics impacting gross margins notably within North American operations.

The company acknowledged that component cost spikes are challenging to immediately offset due to time lag effects between raw material cost changes passing through procurement pipelines versus ability to implement selling price adjustments satisfactorily without dampening demand elasticity [S9].

Additionally, supply chain complexity amplified by geopolitical tensions or public health events raises further risk regarding availability or pricing stability requiring inventory buffers that increase working capital intensity.

Mitigation strategies include multiple qualified suppliers worldwide facilitating sourcing flexibility although alternative suppliers may not always be immediately accessible at competitive prices presenting short-term disruption potential [S20].

Effective tariff pass-through remains dependent on strong distributor relationships along with code-driven regulatory requirements supporting necessity demand rather than discretionary purchase behavior.[S6]

Capital Allocation: Cash Flow, Buybacks, and Return on Equity

Watts Water maintains disciplined capital stewardship prioritizing reinvestment into core manufacturing assets alongside shareholder returns via stock buybacks balanced against prudent liquidity management.

Operating cash flow generation has exhibited consistent upward momentum over the last four years growing from $224 million in FY2022 to an impressive $402 million in FY2025 (+79%) highlighting excellent internal funding capacity versus external financing reliance [F1].

Capex spend correspondingly rose nearly 30% last fiscal year reaching approximately $46 million indicative of targeted investments designed to boost plant automation capabilities supporting product innovation pipeline ramp-ups.[F1]

Stock repurchases occurred moderately totaling around $16 million last fiscal year following similar levels previously conserved given macroeconomic uncertainties; prior larger-scale buyback activity notably receded post-2022 reflecting cautious capital preservation stance amidst volatile input costs.[F1]

Balance sheet strength is evidenced by a current ratio near 2.5x underscoring ample short-term liquidity alongside equity base growth elevating from roughly $1.3 billion at FY2022 end to over $2 billion at FY2025 close.[F1]

Return on equity measured approximately at 16.8%, consistent with efficient capital use translating earnings power into shareholder value creation despite industry cyclicality.[F1]

Dividend payout information was not disclosed explicitly within filings necessitating closer examination by investors focused on yield profiles.[F1]

| FY | CFO ($M) | Capex ($M) | Buybacks ($M) | Equity ($B) | ROE (%)* |

|---|---|---|---|---|---|

| 2022 | 224 | 28 | 69 | 1.30 | - |

| 2023 | 310 | 30 | 16 | 1.51 | - |

| 2024 | 361 | 35 | 17 | 1.71 | - |

| 2025* | 402 | 46 | 16 | >2 ~16.8 | |

| *ROE approximate based on Net Income/Equity for FY25; dividends unavailable from dataset. |

Investor Considerations and What To Watch Next

Looking forward after successful Q4/FY2025 earnings reporting beat expectations underpinning confidence in strategic direction ([N1],[N3]), investors should track several pivotal developments shaping Watts Water's trajectory:

- ERP System Expansion: Execution pace during calendar year 2026 across APMEA sites will reveal tangible progress toward operational excellence goals impacting margin recovery potential amid inflationary headwinds [S4],[N12].

- Innovation Pipeline Delivery: Market reception to newly launched IoT-enabled products within Nexa ecosystem integrating advanced sensors for leak mitigation presents clear catalyst potential widening addressable market share domestically & internationally ([N12],[S18]).

- Input Cost Management: Raw material expense trends along with tariff policy evolutions require scrutiny as these factors materially influence gross margin stability—increased pass-through success correlates with sustained profitability resilience ([S9],[S28]).

- Regulatory Advocacy: Continued engagement fostering stringent plumbing codes enforcement supports competitive moat protecting proprietary technology adoption over commoditized alternatives ([S21]).

- Capital Deployment Decisions: Share repurchase programs vs increased dividend initiation could affect shareholder return perceptions given strong free cash flow profile (> $350 million approx.) providing balance sheet flexibility ([F1]).

In sum, Watts Water Technologies blends traditional manufacturing excellence with modern digital solution integration backed by steady financial performance—monitoring execution consistency against these strategic pillars will be essential for understanding future growth sustainability.

Disclaimer: This report is provided solely for informational purposes based on publicly available data as of February 23, 2026 and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments