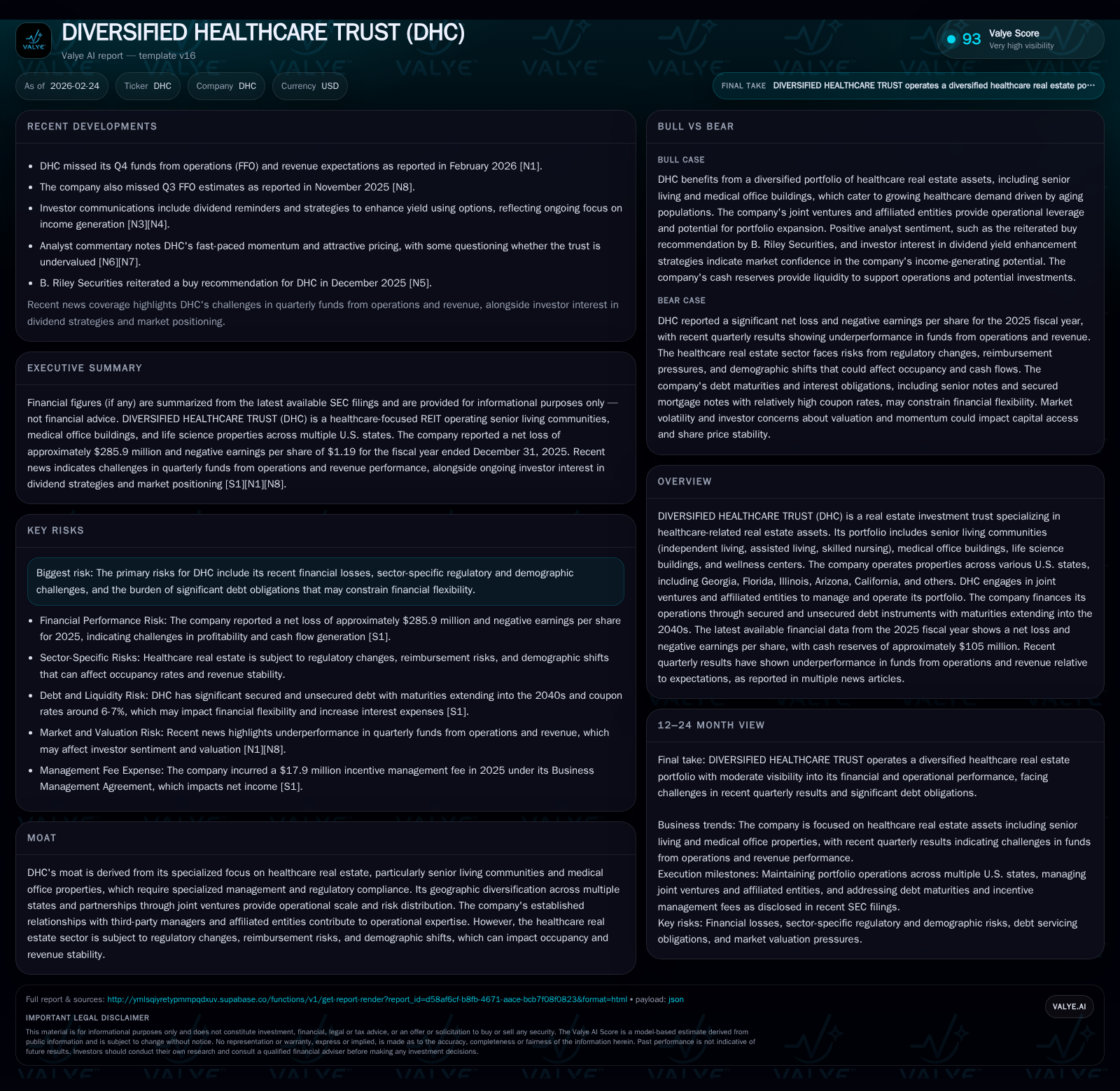

Diversified Healthcare Trust Confronts Debt Pressures Amid Declining FFO and Net Losses

Healthcare real estate investment trust faces financial stress despite stable revenues and diversified assets portfolio.

Diversified Healthcare Trust (DHC) operates a broad portfolio of healthcare-related real estate across multiple U.S. states, including senior living communities and medical office buildings. Despite modest revenue growth, the company posted significant net losses in recent years driven by operating challenges and high leverage. DHC’s capital structure reflects substantial debt maturing in the near term, intensifying liquidity concerns. Its future growth hinges on navigating sector-specific risks such as regulatory changes and demographic trends impacting occupancy and rents.

Company Overview

Diversified Healthcare Trust (DHC) is a specialized Real Estate Investment Trust (REIT) focusing on healthcare-related properties including senior living communities with independent living, assisted living, and skilled nursing components, alongside medical office buildings, life science facilities, and wellness centers.[S1] The company’s geographic footprint spans many U.S. states such as Georgia, Florida, Illinois, Arizona, California among others,[S11][S14] providing some diversification benefits against regional economic variances.

The firm's operational model incorporates joint ventures and affiliated entities,[S1] allowing DHC to distribute risk and leverage third-party expertise for property management in a specialized field that demands compliance with complex healthcare regulations. This specialization forms the moat that underpins its business model, although it introduces vulnerabilities tied to sector-specific regulatory shifts and demographic trends affecting senior housing demand.

Historical Financial Performance

DHC has experienced relatively flat revenue growth over recent years alongside increasingly challenging profitability dynamics. The following table summarizes key financial metrics for recent fiscal years drawn from its SEC filings[F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -286 | -20 | +22.8% |

| 2024 | -370 | 112 | -26.1% |

| 2023 | -294 | 10 | -1761.1% |

| 2022 | -16 | -40 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | ROE% |

|---|---|---|---|

| 2025 | 10 | 1145000 | -17.2 |

| 2024 | 10 | 904000 | -18.9 |

| 2023 | 10 | 393000 | -12.6 |

| 2022 | 10 | 171000 |

Source: SEC companyfacts cache [F1].

Note: Operating income data past FY2018 unavailable; figures derived from the latest reliable periods.[F1]

Revenue has shown slight gains year-over-year but remains essentially stagnant when considering inflationary pressures within healthcare real estate costs. Operating income declined notably by approximately 9%, while net income sharply deteriorated into significant losses due largely to non-cash impairment charges or mark-to-market valuations often seen in REITs managing specialty healthcare assets.[S1]

Operating cash flows also reversed into negative territory after previous improvement, indicating operational difficulties converting ledger revenues into actual liquidity—an important distress signal for a capital-intensive REIT dependent on steady cash generation for servicing debt.[F1]

Dividend distributions have been maintained around $9–10 million annually,[F1] reflecting cautious capital allocation given persistent losses and liquidity constraints. Share repurchases are minimal but indicate some degree of opportunism or shareholder return policy adherence despite financial strain.[F1]

Capital Structure and Debt Profile

DHC’s balance sheet reveals substantial reliance on both secured and unsecured debt instruments,[S4] with maturities extending well into the mid-2040s but pressing near-term maturities looming in the next couple of years (e.g., Senior Unsecured Notes due in 2025).[S4][S6][S10]

The company has mortgage notes bearing coupon rates ranging from approximately 6.2% to over 7%, floating-rate mortgage notes at ~6.8%, as well as zero-coupon secured notes due around 2026,[S4][S6]. This layered debt structure presents refinancing risk especially as operating cash flow turned negative recently.[F1]

Liquidity management remains a critical concern with cash reserves around $105 million at year-end 2025,[F1] which must be balanced against debt service requirements and redevelopment capital needs within the portfolio.

Portfolio Composition and Operational Strategy

DHC’s core asset base comprises specialized senior living facilities alongside medical office buildings and life science campuses.[S11][S14] This diversification across healthcare real estate classes reduces concentration risk but also requires tailored operational oversight.

By engaging third-party managers and entering joint ventures,[S1][S22] DHC leverages external expertise vital for navigating regulatory complexity inherent in Medicaid/Medicare reimbursement environments central to senior housing viability.[S22]

Occupancy trends have been pressured partly by demographic shifts affecting skilled nursing demand and increasing competition from alternative care models—factors that cap rental growth potential.[N1]

Notably, the wellness center segment represents a newer diversification angle targeting preventive health trends but currently constitutes a smaller portion of total assets.[S14]

Industry Context Analysis

Healthcare REITs occupy a unique niche combining real estate expertise with healthcare sector dynamics—including regulatory oversight such as reimbursement rate changes, licensure requirements for senior living operators, and evolving patient care models.

Given that many leases incorporate structured escalators tied to resident fees or rent subsidies, flat-to-declining occupancy directly weighs on funds from operations (FFO), the REIT standard metric more predictive than GAAP net income.

Interest coverage ratios can be volatile depending on valuation revisitations of long-lived assets amid changing healthcare paradigms—intensifying importance of strong capital discipline.

Growth Drivers and Risks

Growth Opportunities:

- Incremental leasing activity in medical office buildings benefiting from outpatient care expansion.

- Selective redevelopment or repositioning of underperforming senior living assets to higher-margin models (e.g., memory care).

- Partnerships increasing scale via joint ventures providing access to new markets without full capital commitment.

- Expansion into life science properties aligning with biotech industry strength.

- Potential rent escalations tied to inflation or operator contract renewal terms.

Growth Constraints:

- Continued erosion in skilled nursing demand driven by Medicare/Medicaid reimbursement adjustments reducing resident intake.

- Regulatory changes imposing operational cost burdens on healthcare operators affecting occupancy sustainability.

- High leverage increasing vulnerability to rising interest rates or tightening credit markets.

- Negative operating cash flow impairing ability to internally fund growth or capital improvements.

- Demographic shifts potentially flattening future addressable market size for certain types of senior housing.

Forward Outlook & Key Milestones to Monitor [N1][S3]

While explicit guidance was not detailed,[N1][S3], investors should watch quarterly funds from operations (FFO) closely given recurring shortfalls relative to consensus estimates recently reported.[N1]

Milestones include:

- Debt refinancing outcomes ahead of key maturities in late 2025–2026.

- Occupancy rate trends across senior living formats post-pandemic recovery.

- Updates on joint venture expansions or asset sales aimed at deleveraging.[N1]

- Changes in dividend policy reflecting sustained earnings capabilities.

- Cash flow stabilization signaling operational turnaround potential.

Returns & Capital Allocation [F1]

Return on equity remains elusive: approximated at negative ~17% based on last reported net loss versus equity base of roughly $1.67 billion.[F1] Such negative returns underscore ongoing challenges locking in positive shareholder value creation.

Dividend payouts continue albeit modestly relative to net losses, suggesting prioritization of distribution consistency possibly to maintain REIT status or investor relations goals.[F1]

Share buybacks have been limited yet ongoing at low volumes potentially representing tactical management moves rather than structured capital return programs.[F1]

Capital expenditures appear restrained relative to earlier peak investments absent clear contemporary line items,[F1] likely impacted by liquidity preservation amid financial stress.

Summary Commentary

DHC's position within the healthcare real estate sector affords structural advantages from specialized asset focus yet also exposes it acutely to sector-specific risks compounded by high leverage levels constraining flexibility.[S1][F1]

Recent financial results highlight persistent operational headwinds manifesting through widening net losses and negative operating cash flows despite steady revenue streams supported by diversified property types across multiple states.[F1][N1]

Debt maturity concentrations over the coming years paired with weak cash generation elevate refinancing risks that management must navigate carefully lest liquidity tighten further.[S4][F1]

Growth drivers exist primarily through selective portfolio optimization and partnerships enhancing market penetration; however, overarching reimbursement volatility and demographic evolutions temper outlook optimism.[N1]

Market participants should monitor quarterly performance metrics around FFO trends, occupancy shifts within senior living sectors, and capital structure adjustments closely for signs of stabilization or further deterioration.

Disclaimer: This analysis is intended solely for informational purposes referencing public data sources without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments