Apellis Pharmaceuticals’ 2025 Profit Turnaround Highlights Royalty Deal Impact and Legal Overhang

After years of significant losses, Apellis returned to profitability in 2025, driven by operational improvements and a major royalty buy-down agreement, amid ongoing litigation risks.

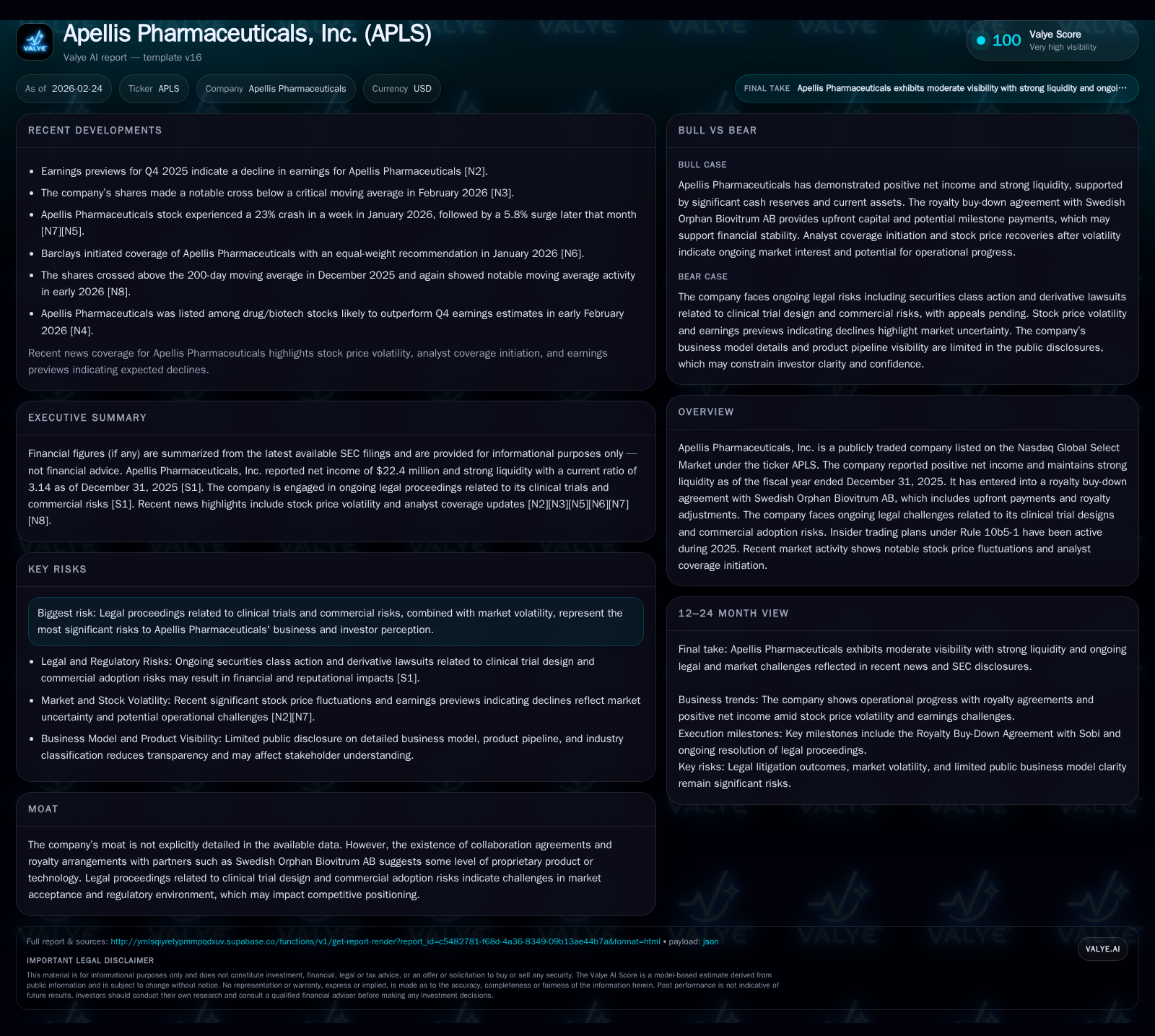

Apellis Pharmaceuticals, Inc. posted a positive net income of $22.4 million in FY 2025 after consecutive years of heavy losses, reflecting a fundamental shift in its earnings trajectory. This turnaround was supported by a $275 million upfront payment from Swedish Orphan Biovitrum AB under a royalty buy-down agreement, which reduced future royalty burdens tied to the company's lead asset Aspaveli/Syfovre. Despite the improved financials and strong liquidity (cash and equivalents exceeding $466 million), the company continues to face legal challenges related to the design of its Syfovre clinical trials and risks related to commercial adoption. Capital allocation remains focused on preserving cash with no dividends or buybacks disclosed.

Historical Performance and Financial Turnaround

For much of the last four years, Apellis Pharmaceuticals operated at substantial annual losses. From fiscal year-end (FYE) 2022 through FYE 2024, the company reported operating losses consistently above $160 million, culminating in a peak operating loss of roughly $517 million in FYE 2023. Net loss patterns mirrored these trends, reaching as deep as -$652 million in 2022 before narrowing markedly.

This sequence reversed sharply in FYE 2025 when Apellis reported an operating income of approximately $55.4 million [F1]. Correspondingly, net income swung positive for the first time in this period at roughly $22.4 million after four consecutive years of negative results.

This improvement is noteworthy given the biotech sector backdrop where extended product development cycles often pressure earnings over multiple years. The steep recovery signals successful monetization efforts combined with structural cost adjustments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 22 | 45 | 55 | 313000 | +111.3% |

| 2024 | -198 | -88 | -165 | 403000 | +62.6% |

| 2023 | -529 | -595 | -517 | 773000 | +18.9% |

| 2022 | -652 | -514 | -595 | 1524000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 45 | 6.0 |

| 2024 | -88 | -86.6 |

| 2023 | -596 | -271.8 |

| 2022 | -515 | -383.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable from tags.

Key Growth Drivers and Royalty Buy-Down Catalyst

A pivotal event supporting the company’s financial shift was the Royalty Buy-Down Agreement entered into with Swedish Orphan Biovitrum AB effective July 1, 2025 [S20]. Under this agreement, Sobi paid Apellis an upfront sum estimated at $275 million within days of closing plus up to $25 million contingent on regulatory approvals for additional indications involving Aspaveli (Syfovre).

In exchange, Apellis agreed to substantially reduce Sobi’s royalties on Aspaveli revenues by approximately 90%, subject to caps tied to sales performance milestones — initially capped at about 1.45x the upfront payment before royalties revert to standard rates [S20].

This deal materially eased Apellis’s cost burden associated with its flagship asset Aspaveli/Syfovre — a complement inhibitor therapy targeting rare diseases such as paroxysmal nocturnal hemoglobinuria (PNH), complement-mediated kidney disorders C3 glomerulopathy (C3G), and immune complex membranoproliferative glomerulonephritis (IC-MPGN).

The royalty relief enhances long-term margin prospects on synergy-driven sales growth if regulatory milestones are achieved for new indications, addressing previously high variable costs that weighed heavily on profitability.

Future Growth Outlook and Milestones

While no explicit revenue guidance was found within recent filings or news releases [N2], investors should monitor:

- Commercial uptake trends for Syfovre in PNH as well as market expansion via EMA approval potential for C3G and IC-MPGN treated by Aspaveli [N2].

- outcomes from ongoing clinical development programs that influence label expansion opportunities.

- progress resolving litigation that could affect perception or distract management resources.

- royalty milestone triggers under the buy-down agreement which could deliver incremental cash flows.

Successful capture of these prospects could sustain revenue momentum; however, drug adoption dynamics remain precarious amid competitive environment and reimbursement landscapes common in orphan drug markets.

Capital Allocation and Returns Analysis

Apellis demonstrates prudent capital stewardship evidenced by its low capital expenditure profile ($313k in FY25), conducive to cash conservation critical for clinical-stage biopharma firms geared towards R&D investments [F1].

Operating cash flows transitioned positively alongside net income improvements — reporting $45.3 million CFO in FY25 versus negative figures priorly — generating free cash flow estimated at approximately $45 million after accounting for capex [F1].

The balance sheet supports flexibility with robust liquidity—cash and cash equivalents totaling over $466 million—and a solid current ratio exceeding 3x [F1]. Equity rose from under $170 million in FY22 to above $370 million in FY25, signaling capital inflows coupled with retained earnings buildup [F1].

No dividends or stock repurchase programs were noted during filing periods analyzed; focus appears toward reinvestment or debt diligence given sizeable outstanding credit facilities consented for amendments linked with financing arrangements around the Royalty Agreement [S20][S10].

Approximate return on equity based on latest FY net income relative to equity is near 6%, indicating nascent profitability phases but below mature pharma benchmarks given the recent turnaround nature.

Legal Challenges Present Risk Considerations

Significant legal proceedings remain one of Apellis’s principal risk vectors:

- A putative class-action claim filed August 2023 alleging misstatements related to Syfovre's clinical trial design and commercial adoption risks was dismissed without prejudice but is currently under appeal before the First Circuit Court following hearings held January 2026 [S1][S4].

- Derivative lawsuits filed by stockholders against company directors allege breaches tied to fiduciary duties regarding those same issues; these cases are temporarily stayed pending the securities class action appeal outcome [S1][S4].

- Routine exposure to potential product liability claims, intellectual property disputes, commercial litigations, or regulatory challenges typical within pharma adds layers of uncertainty [S4][S27].

The resolution trajectory of these legal matters will materially affect investor confidence and may bear financial consequences beyond operational performance.

Market Sentiment & Analyst Activity

Recent trading analyses highlight price volatility: Apellis shares underwent a notable selloff early January (-23%) followed shortly by rallies (+5.8%) later that month implying shifts in investor sentiment driven possibly by news flow or technical factors [N8][N5]. State-of-the-art moving average crossover events captured attention among technical traders [N9][N4].

Brokerage institutions have begun formal coverage around early 2026 with banks like Barclays initiating equal-weight ratings and BofA upgrading sentiments on operational progress [N6][N7]. Such activity denotes growing analyst interest but incorporates balanced views acknowledging underlying risks.

Governance Updates & Insider Transactions

Corporate governance developments include appointment of biotech veteran Craig A Wheeler to Apellis’s Board mid-2025 bringing industry experience from entities like Momenta pharmaceuticals [S25]. This bolsters oversight capabilities during critical transition phases.

Multiple executives maintain Rule 10b5-1 trading plans permitting disciplined sales of stock under predetermined conditions — reflecting methodical approaches to insider liquidity without signaling opportunistic dumping [S2][S7][S12].

Industry Context Analysis

Apellis operates within the challenging yet high-reward niche of complement system therapeutics targeting orphan diseases often neglected by larger pharmas due to small patient populations but commanding premium pricing once approved. Given typical clinical complexity and payer scrutiny prevalent in rare disease markets, companies lean heavily on strategic alliances (e.g., Sobi collaboration here), patent protections, and pipeline diversification for sustainable growth—Apellis exemplifies these trends. Further expansion hinges on successful Phase III results for additional indications driving label breadth which directly correlates with hospital formulary acceptance rates—a crucial metric for penciling longer-term revenue ramps.

Conclusion

Apellis Pharmaceuticals' return to profitability marks a significant inflection point driven largely by proactive licensing deals that alleviate cost pressures while enhancing near-term cash generation capacity amidst scant operational expenditures aside from R&D investments. Nevertheless, persistent legal uncertainties remain an overhang warranting close monitoring along with commercial execution efficacy across its orphan product portfolio. Liquidity strength provides runway flexibility given industry-standard elongated timelines for drug approval cascades – positioning Apellis at a crossroads balancing innovation opportunities against litigation risks and market penetration challenges. This status merits close observation as forthcoming clinical milestones and judicial rulings unfold through mid-decade horizons.

Disclaimer: This document is an informational company analysis based strictly on provided data sources such as SEC filings and verified news articles as cited; it does not constitute investment advice or recommendations regarding buying or selling securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments