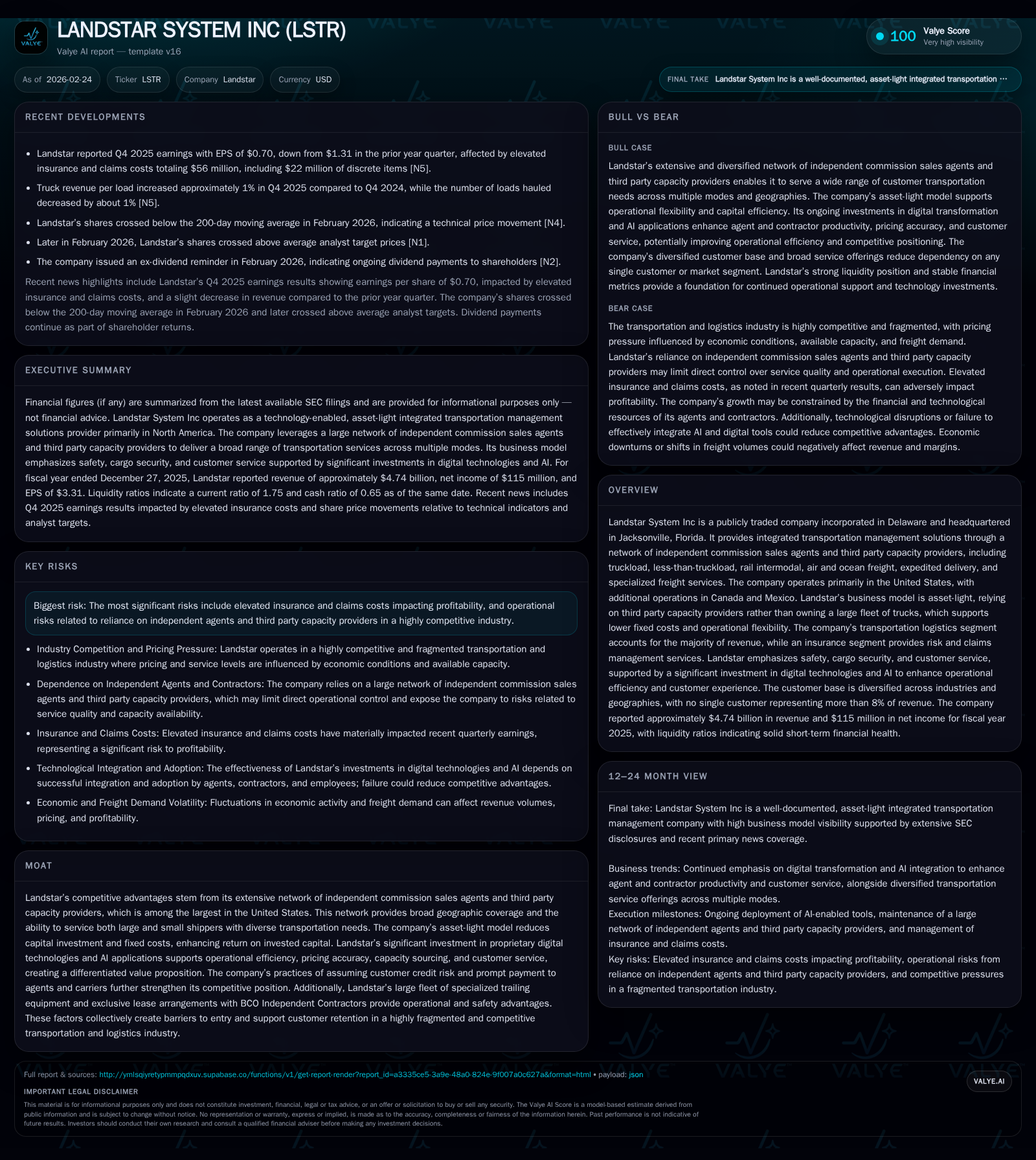

Landstar System’s Revenue Decline and Margin Compression Signal Shifting Market Dynamics

Landstar System’s asset-light freight logistics model faces pressure from slower revenue growth, rising insurance costs, and margin contraction in FY2025.

Landstar System Inc, an integrated transportation management company leveraging a vast network of independent commission sales agents and third-party capacity providers, reported a 1.6% revenue decline in fiscal 2025 following prior years of robust expansion. Operating income fell by nearly 40%, reflecting rising insurance claims costs and operational leverage challenges amid a softening freight demand environment. While Landstar's proprietary AI tools and large specialized trailer fleet continue to underpin efficiency and service differentiation, escalating commercial auto liability claims and legal exposures pose profit headwinds. Capital returns remain a priority despite compressing free cash flow, with increased share repurchases complementing stable dividends.

Landstar’s Historical Performance: Recent Softening After Peak Levels

Landstar System Inc experienced peak revenues of approximately $7.44 billion in fiscal year (FY) 2022 before a notable decline through FY2025. Revenues fell to $5.30 billion in FY2023, then to $4.82 billion in FY2024, followed by a further 1.6% decline to $4.74 billion in FY2025[F1]. Operating income exhibited sharper contraction, dropping from $571 million in FY2022 to $344 million in FY2023, $249 million in FY2024, and down nearly 40% year-over-year to $152 million in FY2025[F1]. Net income declined similarly from $431 million in FY2022 to $115 million in FY2025—a decrease exceeding 41% year-over-year[F1].

Operating cash flow also contracted substantially from $623 million in FY2022 to $225 million in FY2025[F1]. Capital expenditures sharply decreased by over two-thirds in FY2025 to roughly $9.9 million compared to prior years’ ~$25–31 million[F1], reflecting cautious investment amid earnings pressure.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4.7 | 115 | 225 | 152 | -1.6% | -41.3% |

| 2024 | 4.8 | 196 | 287 | 249 | -9.1% | -25.9% |

| 2023 | 5.3 | 264 | 394 | 344 | -28.7% | -38.6% |

| 2022 | 7.4 | 431 | 623 | 571 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 125 | 180 | 215 |

| 2024 | 120 | 81 | 256 |

| 2023 | 117 | 54 | 368 |

| 2022 | 116 | 286 | 597 |

Source: SEC companyfacts cache [F1].

Note: Dividend payments (~$125M annually) and share repurchases are excluded from this table but are material components of capital allocation.

Factors Driving the Revenue and Earnings Contraction

Landstar faced multiple headwinds during FY2025 including softer freight demand across diverse sectors such as consumer durables, heavy machinery, electronics, automotive parts, and building products[N1][N2][N3][S1]. This macroeconomic slowdown affected shipment volumes broadly.

Rising insurance expenses were a significant margin drag as escalating premiums for excess commercial auto liability coverage combined with increased self-insured retention exposures pressured profitability[S11][S17][S18]. The transport sector’s exposure to "Nuclear Verdicts"—catastrophic jury awards exceeding prior norms—has intensified claims cost volatility[S14].

Operational leverage constraints emerged due to fixed administrative costs supporting Business Capacity Owner (BCO) Independent Contractors under exclusive lease agreements[S7]. A shift toward lower-margin Truck Brokerage Carriers also compressed overall profitability.

Together these factors drove an approximate $96 million reduction in operating income despite only modest revenue decline.

Asset-Light Network Model: Strengths and Challenges

At Landstar’s core is its asset-light integrated transportation management model relying on ~960 independent commission sales agents connected with over 70,000 third-party capacity providers—primarily BCO Independent Contractors operating under exclusive leases[S7]. This structure enables scalability with limited fixed capital investment.

The Company owns or leases a substantial trailing equipment fleet (~17,426 trailers as of December 27, 2025), including specialized platform trailers for heavy haul loads[S13]. This equipment supports differentiated service offerings such as expedited shipments and power-only loads.

While this model offers operational flexibility and geographic breadth across North America[S6][S10][S13], it also introduces complexity managing quality control across independent agents amid intensifying competition from digital freight brokers employing dynamic pricing platforms[S11][S14][S18]. Regulatory compliance regarding driver licensing and safety remains critical given FMCSA tightening since mid-2025[S11][S23].

Technology Investments: Enhancing Efficiency Amid Cost Pressures

Landstar has invested over $220 million cumulatively into proprietary technology since launching its "Landstar 2020" initiative[S21]. These systems incorporate AI-powered pricing models that dynamically adjust rates based on market conditions; automated capacity sourcing algorithms assisting agents; AI-enhanced customer contact centers; and fraud detection tools.

Despite driving operational efficiencies internally[N2], these technology advances have not fully mitigated rising insurance costs or margin pressures resulting from volume softness[N3].

Insurance Segment: Limited Revenue but Significant Profit Impact

The insurance segment operates primarily through Signature Insurance Company—a wholly owned offshore reinsurer—and Risk Management Claim Services providing risk management for internal capacity providers[S8]. It accounts for roughly ~1% of consolidated revenue[F1][S8] but significantly influences profitability due to rising claim severity nationally.

Landstar maintains self-insured retention limits up to $5 million per claim before excess insurance layers apply[S17]. Recent policy changes shifted coverage periods from May-April to June-May cycles starting in 2026[S17].

Increased broker liability claims alleging negligent motor carrier selection present legal uncertainties with pending U.S Supreme Court rulings potentially altering risk exposure[S14][S18][S24]. The Company manages exposure through multi-layer reinsurance arrangements with aggregate deductibles up to $18 million but remains vulnerable amid rising "Nuclear Verdicts"[S17][S18].

Cargo theft losses have also contributed to claims cost pressures[S23].

Customer Base: Diversified Large Shippers and Third-Party Logistics Partnerships

Landstar's customer base is highly diversified with the top 100 customers contributing approximately ~46% of consolidated revenues consistently over recent years[S4]. Customers include the U.S Department of Defense, numerous Fortune 500 companies, and eight transportation providers including major third-party logistics firms within the top twenty-five clients.

This mix demonstrates Landstar’s dual role as primary carrier for large shippers and as provider of supplemental capacity within outsourced supply chains.

The Company serves broad industries via multiple transportation modes including truckload, rail intermodal, air/ocean freight enabling responsiveness even for smaller shippers typically underserved by larger carriers[S4].

Capital Allocation: Balancing Returns Amid Cash Flow Pressure

Despite earnings softness impacting free cash flow (operating cash flow minus capex declined from ~$596 million in FY22 to ~$215 million in FY25), Landstar maintained disciplined shareholder returns policies[F1]. Dividends remained steady near $125 million annually while share repurchases accelerated from approximately $54 million in FY23 to nearly $180 million in FY25[F1], reflecting prioritization of capital recycling aimed at enhancing equity returns amid margin pressures.

Return on equity approximated ~14.5% based on latest fiscal net income relative to equity base indicating moderate capital efficiency given challenging performance[F1].

Outlook & Milestones: Monitoring Growth Drivers & Risks

Management commentary during recent earnings calls stresses caution due to macro uncertainties restraining freight demand[N7][N2]. Key growth drivers will include improved capacity utilization rates among contract carriers; successful rollout of AI-enabled pricing platforms; ability to pass inflation-driven costs such as fuel surcharges; and containment of increasing insurance expenses.

Investors should watch quarterly shipment volumes against rate recovery progress alongside regulatory developments affecting broker liability exposure pending Supreme Court decisions which could materially affect risk profiles[S24]. Tracking commercial auto insurance premium trends is critical given their outsized influence on margins per company disclosures[S17][N3].

Operational & Legal Risks Amid Competitive Intensity

Landstar’s reliance on commissioned independent agents affords broad reach but limits direct operational control potentially impacting service consistency[S11][S24]. The U.S transportation logistics sector remains highly fragmented with vigorous competition from asset-heavy fleets as well as digital-first brokers offering agile spot market pricing exerting constant margin pressure[S11][S14].

Compliance with safety standards monitored by regulatory agencies is essential given potential operational disruptions if standards slip[S23]. Legal uncertainties surrounding emerging broker liability claims pose risks that claim-related expenses may exceed existing excess coverage caps creating financial volatility[S24].

Disclaimer: Analysis based solely on publicly filed financial statements [F1], SEC filings [S#], and news reports [N#]; does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments