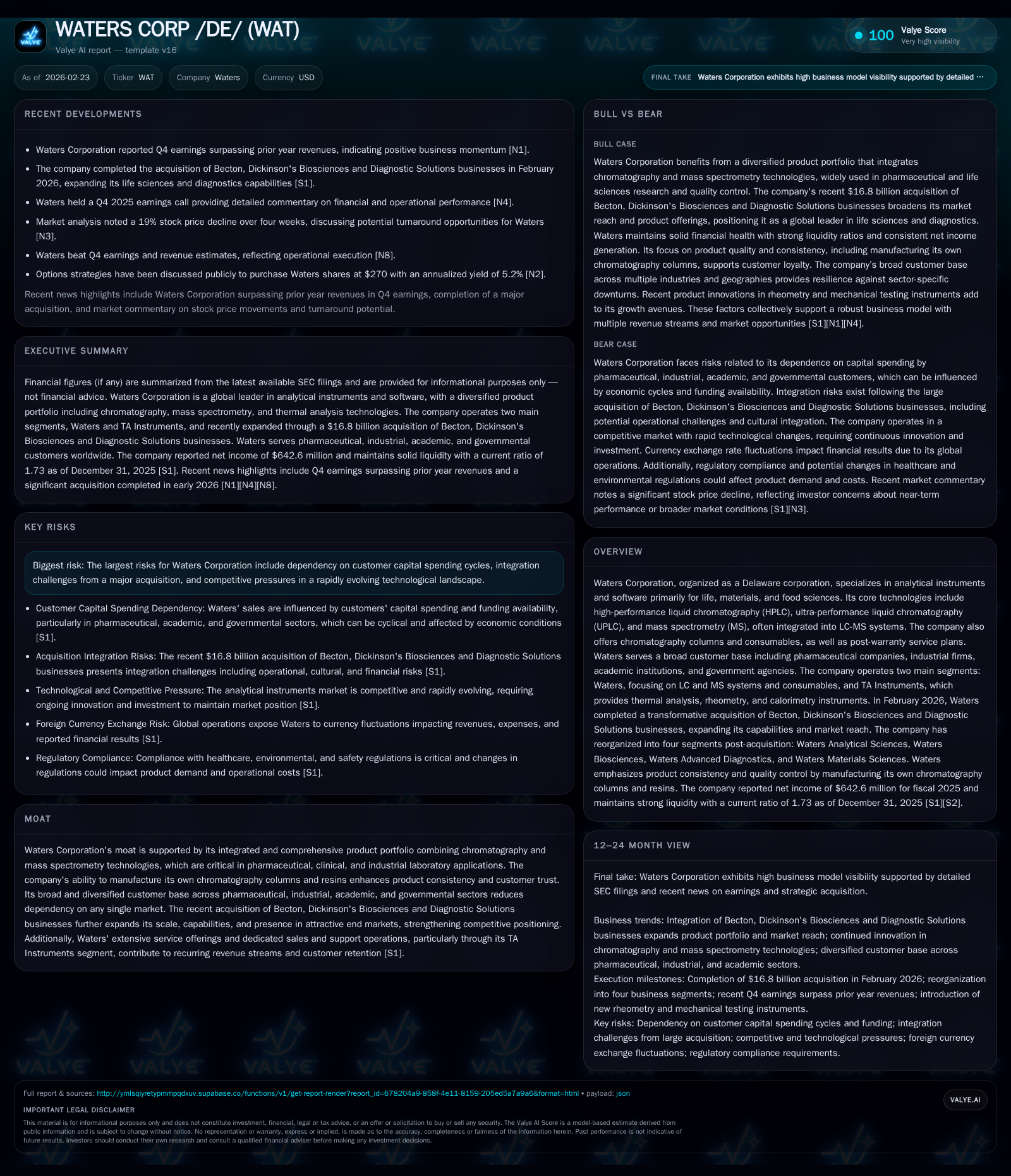

Waters Corporation Expands Scientific Instrumentation with Strategic Acquisition and Innovation

Waters Corporation’s acquisition of Becton Dickinson’s Biosciences and Diagnostic Solutions businesses marks a pivotal expansion in its analytical instrumentation portfolio, reshaping its operating segments and growth prospects.

Waters Corporation demonstrated solid financial performance through 2025 despite modest operating income headwinds, underpinned by its integrated chromatography and mass spectrometry systems. The 2026 acquisition of Becton Dickinson’s Biosciences and Diagnostic Solutions businesses broadens Waters’ technological scope and customer base, prompting a reorganization from two to four business segments to better capture diversified end-market opportunities. Operating cash flows remain robust, supporting measured buyback activity amid increased equity from acquisition-related transactions. Key risks include integration complexities, fluctuations in customer capital spending—particularly from pharmaceutical clients—and intense innovation competition. Monitoring upcoming segment disclosures and consumables revenue dynamics will be crucial as Waters seeks to leverage its expanded footprint for sustained growth.

Waters’ Legacy Business Model and Historical Financial Performance

Waters Corporation has historically anchored its business on analytical instruments combining liquid chromatography (LC), ultra-performance liquid chromatography (UPLC), and mass spectrometry (MS) technologies—often integrated as LC-MS systems. These systems are complemented by proprietary chromatography columns and chemical consumables that enhance repeatability and customer loyalty. Service revenues constitute roughly a quarter of overall sales for both Waters’ LC-MS business and the TA Instruments thermal analysis segment [S4][S5].

Reviewing recent financials reveals mixed trends: Operating income declined by 7.4% year-over-year to approximately $271 million in FY2025, contrasting with a marginal net income increase of 0.8% to around $643 million [F1]. This dichotomy implies that while core operational profitability softened possibly due to pricing pressures or rising costs including acquisition-related amortization, non-operating factors like tax benefits or foreign exchange translation mitigated impact on bottom line [S1].

Operating cash flow remained healthy at $653 million though down 14.4% YoY, which alongside continued capital expenditures ($113 million) underscored sustained investment in product development. Notably, Waters maintains a favorable current ratio near 1.7 reflecting liquidity adequacy amid ongoing capital deployment [F1][S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 643 | 653 | 271 | +0.8% |

| 2024 | 638 | 762 | 292 | |

| 2023 | 603 | 264 | ||

| 2022 | 612 | 286 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 15 | 25.1 |

| 2024 | 14 | 34.9 |

| 2023 | 70 | |

| 2022 | 626 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is not available from provided tags; dividends paid are also not disclosed.

Impact of Becton Dickinson’s Biosciences and Diagnostic Solutions Acquisition

In February 2026 Waters completed a transformative acquisition of Becton Dickinson's Biosciences and Diagnostic Solutions businesses [N1][S3]. Strategically this move significantly expands Waters' scale into complementary life sciences domains beyond chromatography and mass spectrometry—incorporating cellular analysis tools and diagnostic platforms.

The acquisition enhances the competitive moat by integrating integrated solutions spanning drug discovery to clinical diagnostics with the company's robust installed base. It diversifies end-market exposure towards bioscience research entities and clinical labs previously outside Waters' core customer base dominated by pharmaceutical firms [S4].

Integration challenges present near-term constraints on operational efficiency gains; however management's plan encompasses leveraged cross-selling opportunities across newly combined technologies while driving recurring revenues through enhanced service contracts.

Evolving Segment Architecture: From Two to Four Reporting Segments

Prior to the acquisition Waters reported results under two segments: 'Waters' consisting mainly of LC-MS systems plus consumables/services and 'TA Instruments', providing thermal analysis equipment such as rheometers and calorimeters [S4]. Post-acquisition the company restructured reporting into four segments:

- Waters Analytical Sciences

- Waters Biosciences

- Waters Advanced Diagnostics

- Waters Materials Sciences

This granularity reflects strategic segmentation where Analytical Sciences focuses on classic LC-MS platforms; Biosciences integrates cellular analysis tools acquired from BD; Advanced Diagnostics includes emerging diagnostic instruments; Materials Sciences incorporates thermal analysis via TA Instruments [S5][S6]. This segmentation aligns with differentiated customer workflows ranging from pharma R&D labs requiring high throughput UPLC-MS instruments to manufacturing quality control relying on rheometry.

Drivers Behind Recent Operating Income and Cash Flow Trends

The decline in FY2025 operating income contrasts with stable net income due in part to amortization expenses related to intangible assets from prior acquisitions impacting operating margins [S1]. Meanwhile robust operating cash flow reflects effective working capital management leveraging instrument consumable sales resilience.

Purchases of high-cost instrument systems from pharmaceutical clients remain subject to capital spending cycles—often tied to R&D budget fluctuations—whereas consumables such as chromatography columns enjoy steadier demand given recurring use patterns [N2][S6]. This dynamic emphasizes the strategic importance of balanced revenue streams.

Depreciation/amortization charges likely increased preceding the BD acquisition closing date; these non-cash costs pressure operating income though not immediate cash flows [S1].

Outlook and Market Dynamics in Pharmaceutical and Industrial Analytical Technologies

Pharmaceutical customers accounted for approximately 59% of sales in 2025; industrial clients about 30%, with academic/governmental agencies comprising the remainder [S6]. This mix underscores pharma’s centrality as a demand driver given their extensive use of LC-MS for drug discovery through clinical trial testing.

Company guidance for FY26 signals expectations for incremental growth supported by new segment synergies post-BD acquisition alongside ongoing innovation investments in UPLC-MS technologies targeting speed improvements and sensitivity enhancements [N4].

Analysis: The cyclicality inherent in pharmaceutical R&D budgets creates variability particularly impacting capital instrument purchases whereas durable consumables/maintenance contracts offer more predictable revenue streams—especially critical during economic uncertainty.

Capital Allocation Priorities: Equity Growth, Buybacks, and Investment in Innovation

Stockholders’ equity swelled from roughly $1.15 billion at year-end FY23 to over $2.56 billion by end-FY25—a reflection of both retained earnings accumulation and equity appendages associated with M&A activities [F1].

Despite strong cash generation (~$653 million CFO in FY25), buybacks were modest at approximately $14.7 million reflecting prudent capital deployment priorities amid integration expenditures and targeted capex ($113 million).

ROE approximates an efficient ~25%, illustrating disciplined profit generation relative to equity base expansion [F1]. Dividend payments are not disclosed within the available data indicating a potential area for further disclosure.

Risks Around Integration, Customer Spending Cycles, and Competitive Pressures

Key risks explicitly cited include complexities surrounding assimilation of BD bioscience operations potentially disrupting near-term productivity; dependency on often volatile customer capital spending cycles which affect large instrument purchase timing; plus technological innovation demands requiring ongoing R&D investment sustain market leadership [N1][S1].

Further foreign currency translation impacts emerge notably on tax provisions causing earnings fluctuation partially mitigated through hedging strategies given multinational footprint encompassing over thirty-five countries [S1][S9].

Competitive pressures from established players innovating rapidly within LC-MS as well as emerging life science instrumentation intensify the need for continuous portfolio evolution.

Key Metrics to Monitor in Upcoming Quarters

Attention should focus on quarterly segment-level disclosures aimed at illuminating contributions from newly formed Biosciences and Advanced Diagnostics units post-acquisition [N4][N2]. Shifts toward higher proportions of service revenues or consumables would suggest strengthening recurring income streams buffering against instrument order cyclicality.

Capital expenditure trends among major pharma customers will continue serving as leading indicators for base instrument system demand momentum.

Margin trends post-integration will reveal efficiency gains or challenges inherent in merging complex technology platforms.

Disclaimer: This document is intended solely for informational purposes based on publicly available data as of February 23rd, 2026. It does not constitute investment advice or recommendations regarding any securities or companies mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments