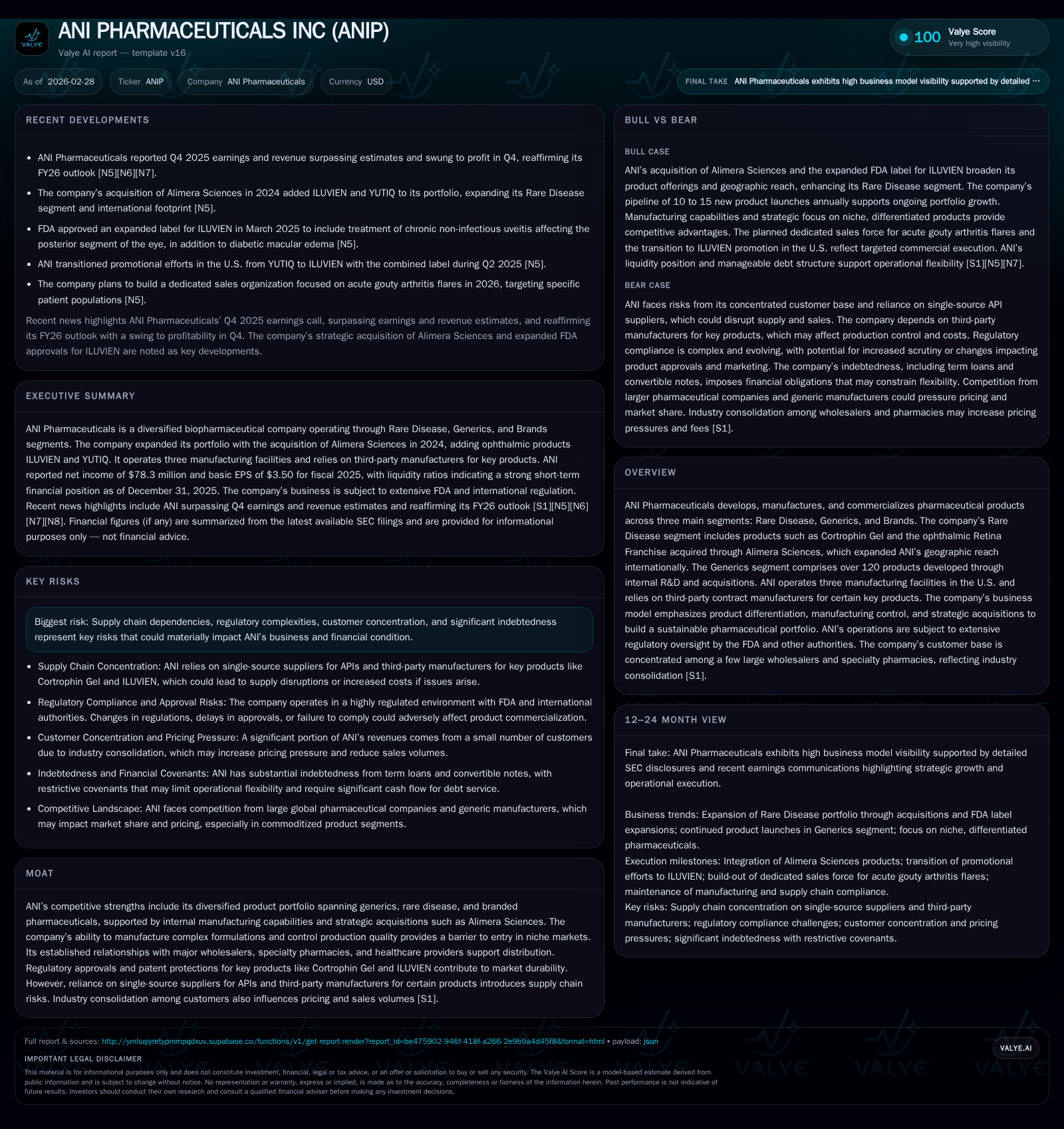

ANI Pharmaceuticals' Turnaround: From Operational Struggles to Strategic Growth

ANI Pharmaceuticals reversed years of financial difficulties through a strategic acquisition and operational realignment, delivering strong profit growth in 2025.

After navigating several years marked by losses and narrow operating margins, ANI Pharmaceuticals delivered a remarkable turnaround in 2025, driven largely by the transformative acquisition of Alimera Sciences. The expanded portfolio, especially in rare diseases with products like ILUVIEN and YUTIQ, combined with enhanced manufacturing control and selective marketing shifts, underpins this shift. Despite significant supply chain and regulatory risks inherent to its complex product mix, ANI’s robust cash flow generation and prudent capital allocation signal a more sustainable growth phase ahead.

Financial Performance Overview

ANI Pharmaceuticals experienced a volatile financial trajectory over recent years culminating in a notable resurgence in fiscal year 2025. Revenue peaked at $57.12 million in 2018 before declining to $47.97 million in 2019 [F1]. The company faced significant headwinds with net losses of $47.90 million and operating losses of $35.28 million in 2022. However, by 2023 net income returned to positive territory at $18.78 million alongside an operating income of $46.97 million, followed by a substantial increase in 2025 with net income reaching $78.34 million and operating income soaring to $111.09 million [F1].

Operating cash flow also reflected this recovery trend, rising from negative $31.20 million in 2022 to positive $185.23 million in 2025, demonstrating improved earnings quality and working capital management [F1]. Capital expenditures moderated slightly from $16.24 million in 2024 to $13.84 million in 2025 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 78 | 185 | 111 | 14 | +522.9% |

| 2024 | -19 | 64 | 1 | 16 | -198.6% |

| 2023 | 19 | 119 | 47 | 9 | +139.2% |

| 2022 | -48 | -31 | -35 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 1157000 | 12 | 171 |

| 2024 | 1625000 | 11 | 48 |

| 2023 | 1625000 | 5 | 110 |

| 2022 | 1625000 | 2 | -40 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are reported for years available; revenue declined approximately 16% YoY comparing latest available data points [F1].

Strategic Acquisition and Portfolio Expansion

A pivotal milestone was ANI's acquisition of Alimera Sciences on September 16, 2024 [S1], which added two proprietary branded ophthalmic products—ILUVIEN® and YUTIQ®—to its rare disease segment portfolio [S1],[S6]. These corticosteroid-based therapies have FDA approvals for diabetic macular edema (DME) and chronic non-infectious uveitis affecting the posterior segment (NIU-PS), with ILUVIEN also approved across seventeen European countries [S1]. This acquisition facilitated a strategic shift toward specialty branded products alongside ANI's traditional generics business.

The acquisition was financed through a fully drawn $325 million senior secured delayed-draw term loan facility and approximately $316 million aggregate principal amount of convertible senior notes issued earlier in August 2024 [S1],[S5]. This capital structure supports ANI's growth ambitions while introducing fixed interest obligations.

Manufacturing Capabilities and Operational Focus

ANI operates three pharmaceutical manufacturing facilities located in Baudette, Minnesota (two sites), and East Windsor, New Jersey [S1]. These sites enable production across multiple dosage forms including oral solids, semi-solids, liquids, topicals, controlled substances requiring fully-contained environments, and potent products [S1]. The company ceased operations at its Oakville, Ontario facility as part of restructuring efforts completed by March 31, 2023 [S1].

This manufacturing footprint positions ANI favorably for producing complex formulations under stringent regulatory oversight [S7],[S8]. Nonetheless, reliance on single-source active pharmaceutical ingredient suppliers for key products such as Cortrophin Gel presents supply chain risks exacerbated by regulatory constraints including DEA oversight [S1],[S7]. Additionally, certain acquired products depend on third-party contract manufacturers requiring ongoing compliance vigilance.

Revenue Composition and Customer Dynamics

ANI segments its revenues into Rare Disease—including Cortrophin Gel and the ophthalmic franchise from Alimera—Generics comprising over 120 products developed or acquired through ANDAs/NDAs, and Brands primarily resulting from acquisitions [S1],[S6]. Distribution channels include major wholesalers such as Cencora Inc., Cardinal Health, McKesson, as well as specialty pharmacies like CVS Specialty Pharmacy and Accredo Specialty Pharmacy catering to rare disease treatments [S6].

Customer concentration remains elevated though somewhat reduced compared to prior years: approximately three customers accounted for around 53% of total revenues as of December 31, 2025 compared with four customers contributing about 64% previously [S6],[F1]. This concentration reflects industry-wide wholesaler consolidation impacting pricing dynamics.

Return policies allow product returns from six months prior up to one year post expiration date affecting accruals for chargebacks, rebates, returns, and other allowances factored into working capital management [S6],[F1]. Medicaid rebate liabilities have increased due to acquisitions involving branded products introducing additional government pricing complexities [S4],[S9],[S19].

Regulatory Environment and Associated Risks

ANI operates within a complex regulatory framework encompassing FDA approvals for marketed products including label expansions such as ILUVIEN’s indication for NIU-PS approved in March 2025 [S1]. Compliance extends to federal anti-kickback statutes (AKS), false claims acts (FCA), data privacy laws including HIPAA provisions, reporting obligations under Medicaid Drug Rebate Programs, Medicare Manufacturer Discount Program compliance, as well as supply chain security requirements under DSCSA serialization mandates effective since November 2018 [S4],[S7],[S10],[S19],[S24],[S8].

Risks include potential supply disruptions from single-source API suppliers subject to DEA regulation, contract manufacturer compliance failures leading to product shortages or recalls, penalty exposures related to inaccurate rebate accruals or governmental audits, evolving interpretations of healthcare laws post-Loper Bright Enterprises v Raimondo Supreme Court decision limiting agency deference that may increase regulatory uncertainty [S1],[S4],[S7],[S9],[S13],[S14].[N13]

Capital Structure and Cash Flow Utilization

ANI’s capital structure as of December 31, 2025 includes a $325 million senior secured term loan fully drawn at acquisition closing plus a revolving credit facility with approximately $75 million committed capacity partially available for borrowing subject to conditions [S5],[S12]. The company also issued approximately $316 million aggregate principal convertible senior notes due September 2029 bearing a coupon rate of about 2.25% per annum payable semi-annually starting March 2025 [S5],[S12].

Financial position evidences strong liquidity with cash & equivalents totaling approximately $286 million alongside current assets of roughly $753 million exceeding current liabilities near $278 million yielding a current ratio around 2.7x supportive of short-term solvency [F1].

Strong operating cash flow generation amounted to approximately $185 million for fiscal year ending December 31, 2025 supporting ongoing capital expenditures near $13.8 million resulting in free cash flow estimated around $171 million [F1]. This robust cash flow enabled modest dividends paid totaling about $1.16 million alongside an acceleration in share repurchases increasing to roughly $12.2 million from prior years reflecting confidence in capital return strategies amid improving profitability [F1].

Outlook: Pipeline Development and Market Considerations

ANI anticipates sustaining innovation momentum through launching approximately ten to fifteen new generic products annually leveraging internal R&D capabilities combined with selective acquisitions enhancing portfolio breadth particularly within generics and specialty brands segments [S5],[S6]. The Rare Disease ophthalmic franchise continues to be a key growth vector supported by international market penetration.

Medium-term challenges include managing patent expirations on key branded products such as ILUVIEN and YUTIQ which could pressure exclusivity-derived margins absent successful lifecycle management or replacement therapies [S1],[S13]. Furthermore, ongoing industry trends toward wholesaler consolidation may compress pricing power necessitating agile commercial strategies.

Regulatory uncertainties remain elevated following the mid-2024 U.S. Supreme Court ruling restricting agency deference potentially affecting FDA/CMS rulemaking processes impacting approval timelines or reimbursement policies unpredictably [S13],[S14].[N13] ANI maintains cautious optimism balancing growth opportunities against these risks.

Supply chain resilience remains critical given concentrated API sourcing risks coupled with complex Medicaid rebate program compliance requiring continuous enhancement amidst tightening healthcare regulatory environments domestically and abroad [F1],[S14],[S22].

This analysis is based exclusively on publicly filed SEC disclosures ([F1], [S#]) complemented by recent earnings call transcripts ([N#]). It avoids speculative forecasts unsupported by cited data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments