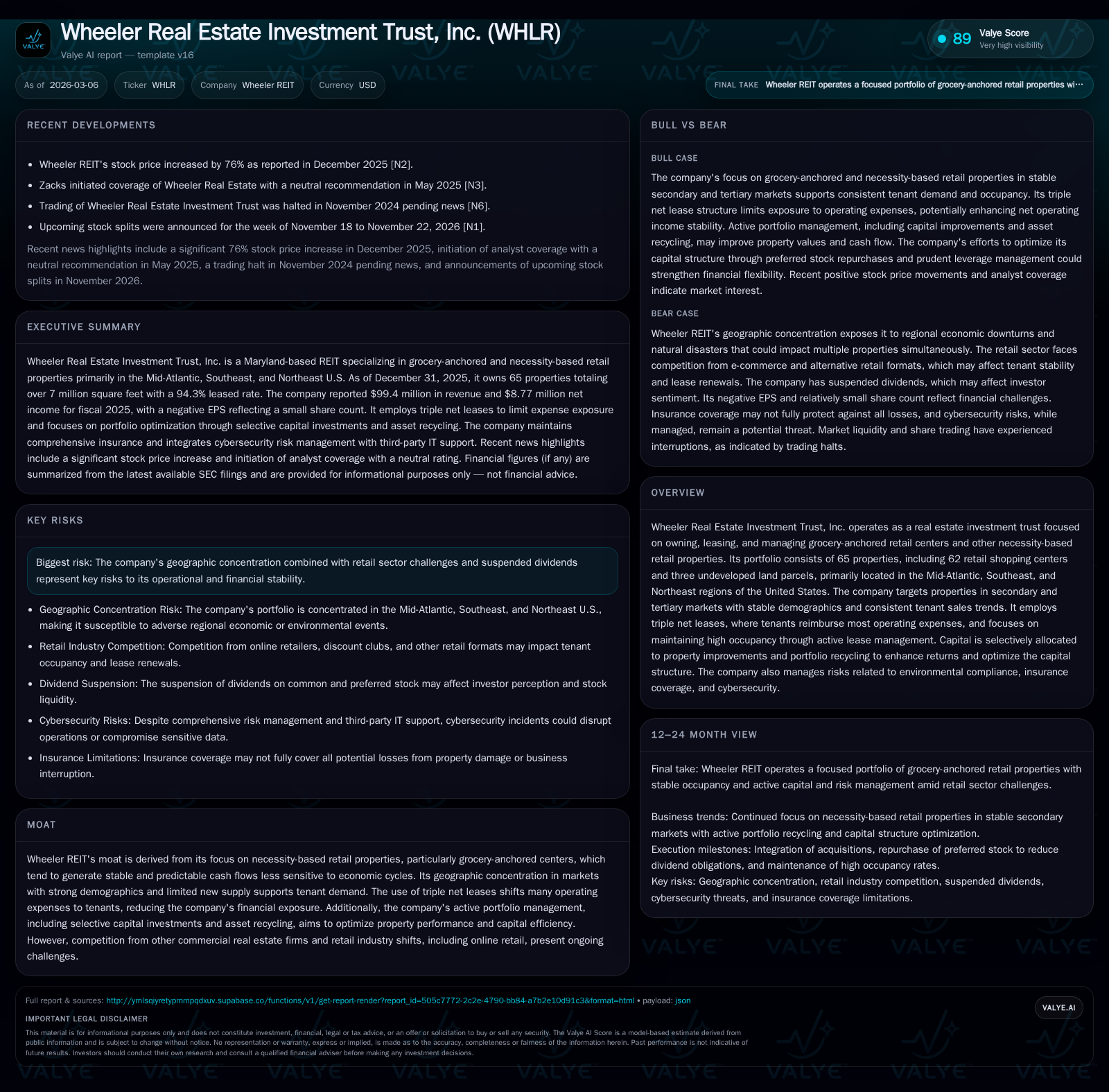

Wheeler REIT's Balanced Approach Amid Retail Sector Challenges

Wheeler Real Estate Investment Trust focuses on grocery-anchored retail centers in stable secondary markets using strategic leasing and capital management to offset sector headwinds.

Wheeler REIT operates a portfolio of 65 grocery-anchored and necessity-based retail properties predominantly in Mid-Atlantic, Southeast, and Northeast U.S. secondary markets. Despite a near 5% decline in revenue in 2025, the company improved operating income by over 15%, driven by enhanced lease management and expense controls via triple net leases. Wheeler actively recycles assets and prudently manages its $483 million debt with staggered maturities, while suspending dividends to preserve liquidity. Going forward, growth hinges on occupancy maintenance, refinancing success, and selective capital expenditures aimed at accretive property enhancements amid ongoing retail real estate volatility.

Portfolio Evolution and Past Financial Growth

Wheeler REIT's recent financial trajectory paints a nuanced picture of a retail-focused REIT navigating a challenging real estate environment with strategic operational adjustments. The company's revenue peaked at approximately $104.6 million in FY2024 before retreating by about 4.9% to $99.4 million in FY2025 [F1]. This top-line contraction largely reflects asset dispositions as Wheeler actively recycles its portfolio rather than organic revenue loss.

However, operating income told a different story: rising from $37.5 million in FY2024 to $43.2 million in FY2025—a robust improvement of 15.2% [F1]. Enhanced leasing strategies, coupled with stringent expense management—especially leveraging triple net leases where tenants bear property tax, insurance, and maintenance expenses—boosted profitability even as revenue softened [S1].

Net income also swung meaningfully into positive territory at $8.8 million for FY2025 versus losses exceeding $9.5 million the previous year [F1]. This turnaround underscores effective portfolio repositioning alongside operational efficiency gains.

Operating cash flow (CFO) showed some deceleration—from roughly $25.9 million in FY2024 down to $21.1 million in FY2025—reflecting lower NOI contributions from disposed assets despite incremental gains in same-property NOI [F1][S23]. Capital expenditures increased by over 32% year-over-year to support targeted property improvements aligned with enhancing long-term rent potential [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 99 | 9 | 21 | 43 | -4.9% | +191.6% |

| 2024 | 105 | -10 | 26 | 38 | +2.2% | -104.3% |

| 2023 | 102 | -5 | 21 | 29 | +33.5% | +62.4% |

| 2022 | 77 | -12 | 31 | 25 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 7 | 3747.9 |

| 2024 | 10 | 37.7 |

| 2023 | 11 | 22.0 |

| 2022 | 3 | 82.1 |

Source: SEC companyfacts cache [F1].

Source: Wheeler REIT Annual Reports [F1]

Wheeler’s Grocer-Centered Market Focus and Operating Model

The cornerstone of Wheeler’s moat lies in its focus on necessity-based retail centers anchored by grocery tenants that attract stable shopper traffic irrespective of the economic cycle [S1]. Concentrated primarily across Mid-Atlantic (47%), Southeast (45%), and Northeast (8%) U.S., these secondary and tertiary markets are characterized by stable demographics: steady population growth and consistent household income levels that offer demand durability.

Wheeler’s portfolio includes 62 retail shopping centers spanning over seven million rentable square feet at a high occupancy rate of approximately 94.3%, complemented by three undeveloped land parcels [S1]. No individual tenant accounts for more than around 6% of annualized base rent or gross leasable square footage; the top ten tenants collectively contribute just under a quarter of rents—mitigating tenant concentration risk.

The company employs predominantly triple net leases—a hallmark in commercial real estate whereby tenants assume responsibility for property taxes, insurance premiums, common area maintenance costs including repairs—thereby materially insulating Wheeler from cost volatility while stabilizing cash flows [S15]. Active leasing strategies include managing lease expirations meticulously to optimize occupancy levels and negotiating renewals or replacements swiftly for vacated anchor spaces.

Tenant diversification spans national and regional retailers providing essential consumer goods less sensitive to consumer disposable income fluctuations—helping Wheeler maintain predictable property-level cash flows despite broader retail disruptions like e-commerce growth [S1].

Navigating Capital Structure and Debt Maturities

As of December 31st, 2025 Wheeler held approximately $482.8 million in total indebtedness across various secured loans [S4][F1]. The bulk of this financing adopts fixed interest rates averaging about 5.5%, supported by an average maturity horizon extending roughly six-and-a-half years—a testament to prudent liability management amid capital market uncertainties.

Key facilities include:

- June 2024 Term Loan: $25.5 million fixed at 6.80%, collateralized by multiple shopping centers; amortizing principal commencing August 2029 over a thirty-year schedule [S6][S28]

- August 2025 Cedar Credit Facility: up to $20 million revolving credit line with options between base rate or SOFR plus margin; collateral initially includes several properties later released following asset dispositions [S4][S9]

- April 2025 Cedar Bridge Loan: bridge financing totaling $10 million maturing February 2028 aimed at temporary liquidity support during asset sales phase [S9]

- Various other term loans balanced between fixed-rate notes ($476M) and variable-rate lines (~$6M) reflecting blended costs optimized through refinancing activities conducted over recent years [S6][S7]

Liquidity buffers were bolstered by approximately $23.7 million cash plus nearly equal sums reserved within lender-controlled funds dedicated toward tenant improvement allowances and financing covenants compliance [S8]. Scheduled principal repayments aggregate about $6.45 million for fiscal year ending December 31st ,2026 followed by manageable amortization schedules extending over subsequent years enabling measured refinancing risk exposure [S4].

Additionally the company has demonstrated repayment discipline via accelerated paydowns connected to specific asset sales such as Tri-County Plaza reducing principal balances proactively alongside loan prepayment premiums incurred which collectively enhance balance sheet resilience [S6][S7].

Capital Allocation: Redeployment, Buybacks, and Dividend Policy

Wheeler pursues active capital recycling whereby non-core or undeveloped parcels are sold with net proceeds directed toward deleveraging the balance sheet or investing into higher yield real estate opportunities within its core strategy framework [S15]. Capital expenditures surged approximately one-third year-over-year to about $8.5 million reflecting accretive investments aimed at tenant retention via mall upgrades or extending anchor leases to sustain occupancy profiles [F1][S23].

Notably the Company repurchased substantial amounts of preferred stock trading below liquidation value as part of an opportunistic deleveraging initiative—retiring shares worth roughly $84 million liquidation value for about $53 million actual cash outlay—which is expected to reduce future dividend obligations substantially by approximately $5.6 million annually [S10][S11][S14]. This illustrates Wheeler’s intent on optimizing capital structure via buybacks while reinforcing financial stability amidst earnings pressures.

Since March 2018 common stock dividends have been suspended along with cumulative preferred distributions due to accumulated unpaid dividends elevating Series D Preferred Stock dividend rates up toward the maximum contractual threshold of sixteen percent per annum as unpaid balances accrue compounded penalties until settled or refinanced [S14]. Dividends thus remain discretionary based on available cash flow after operational needs alongside REIT-compliance requirements balancing shareholder return expectations against liquidity preservation priorities.

Operating Income Growth Drivers and Expense Management

Wheeler's reported operating income escalation (+15%) amid softening revenue signals execution strength powered largely through focused lease operations optimizing occupancy rates notwithstanding broader retail headwinds which include shifting consumer patterns towards online channels [F1][S1]. Lease commissions remain controlled while leveraging tenant reimbursements embedded within triple net agreements allows significant pass-through of property-related expenses which reduces Wheeler's direct exposure to fluctuating carrying costs [S15].

The portfolio’s tenant mix featuring non-cyclical consumer goods providers aligns well with supporting steady rental collections generating recurring base rent revenues supplemented by regular escalations as per long-term lease contracts enhancing operating margin profiles further [S1][F1].

Future Growth Outlook and Near-Term Milestones to Monitor

While Wheeler does not provide formal forward-looking guidance publicly within filings or releases explicitly as of early March ’26 reviews indicate management’s focus remains centered on several pivotal areas:

- Refinancing upcoming debt maturities prudently mitigating market risk through accommodative lender relations backed by collateral quality [N1][S4]

- Backfilling vacant anchor spaces promptly while renewing existing leases maintaining high occupancy critical for sustaining funds from operations (FFO) momentum given concentrated regional exposure [S11]

- Executing ongoing asset disposition plans for non-income producing land parcels contributing toward deleveraging objectives freeing capital for reinvestment into core assets yielding higher returns [S15]

- Monitoring KPI trends such as lease renewal rates above historical benchmarks indicating tenant sales strength supporting rental rate stability or growth potential analyzed internally for proactive leasing decisions.

Collectively these milestones frame near-term expectations where sustained performance will be contingent upon macroeconomic retail trends balancing necessity goods demand amid evolving consumer preferences across their target secondary/tertiary geographies.

Risk Factors: Geographic Concentration and Sector Challenges

Wheeler’s geographic concentration across Mid-Atlantic/Northeast/Southeast regional corridors inherently concentrates exposure to localized economic cycles affecting retailer health thus creating risk clusters particularly when tied to specific tenants despite diversified tenant roster underlining roughly one-fifth annualized rent concentration among top ten renters only [S1].

The suspension of dividends since early last decade underscores ongoing liquidity constraints potentially influencing equity valuation perceptions unfavorably among market participants given yield expectations associated generally with REITs paying stable distributions regularly [S14].

Retail real estate continues facing structural challenges: omnichannel competition diminishes foot traffic threatening brick-and-mortar tenancy impacts notwithstanding necessity-based anchors somewhat insulated but not immune from shifts that could pressure renewal rents or occupancy negatively thereby impairing net operating income sustainability on individual assets.

Environmental regulations requiring compliance also remain scrutinized variables but so far have not materialized into material financial liabilities suggesting reasonable risk control mechanisms are employed architecturally at properties managed subscription wide [S16].

Employee Engagement and Governance Practices

Supporting operational resilience is Wheeler's human capital strategy encompassing competitive wages aligned with regional labor markets alongside broad employee benefits structured around wellness – including disability coverage benefits free gym memberships plus tuition assistance including language acquisition programs catering toward diverse tenant communities served illustrating a workforce culture attuned to stakeholder value creation beyond immediate financial KPIs [S1].

Compliance culture is reinforced through mandatory annual certifications upholding corporate ethics codes ensuring integrity standards sustain governance frameworks vital for regulatory trust especially given REIT status requisites underpinning tax-efficient organizational structure stability.

This analysis synthesizes information from SEC filings dated March 2026 alongside consolidated financial data without offering investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments