NCS Multistage Displays Strong Profit Recovery Driven by Proprietary Technology and Market Expansion

NCSM’s 2025 financials highlight revenue growth and enhanced profitability amid intensified competition and evolving oilfield service demands.

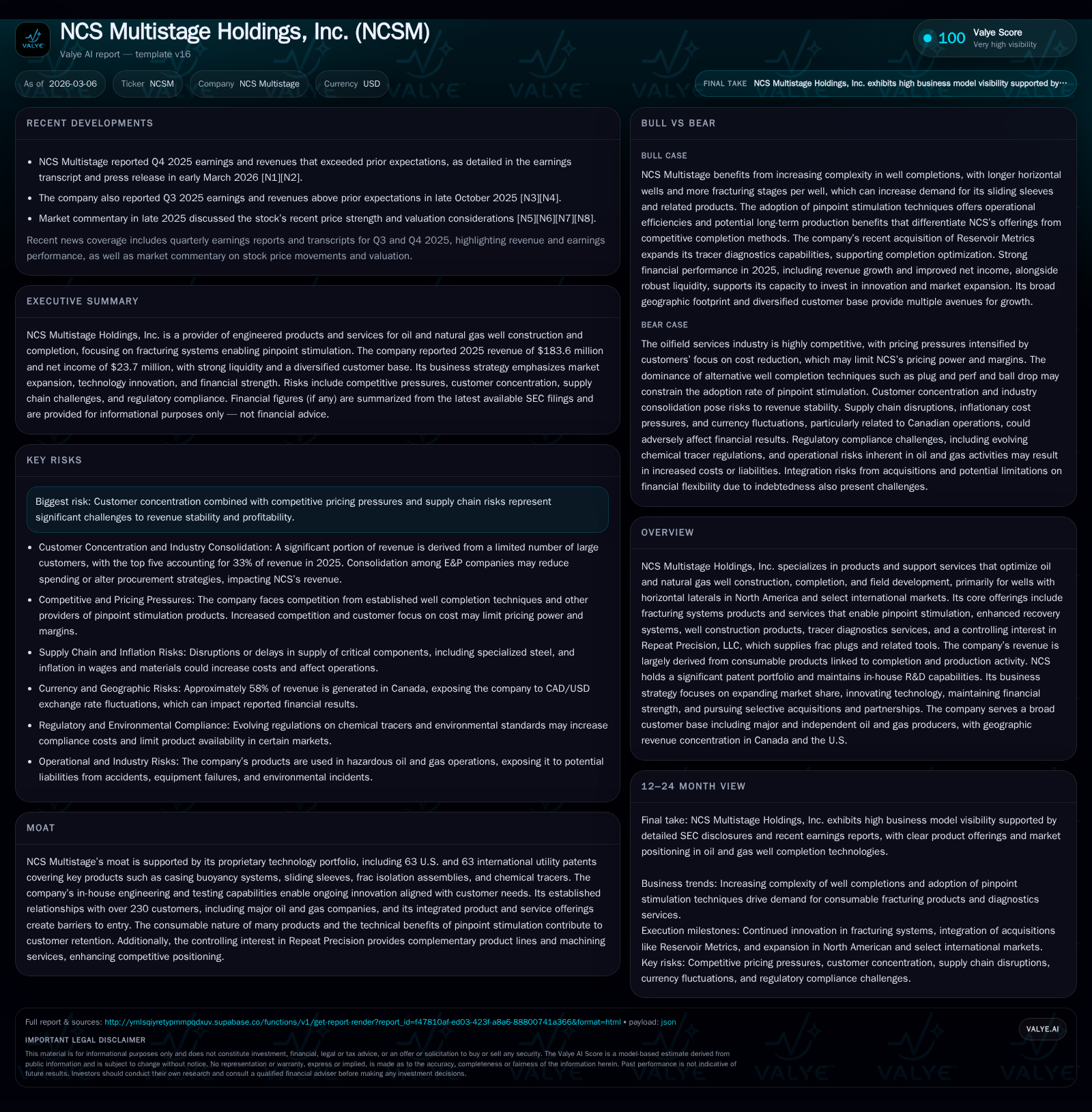

NCS Multistage Holdings, Inc. executed a robust financial turnaround in 2025 with revenues increasing to $183.6 million and net income surging to $23.7 million, supported by expanding market penetration of its proprietary fracturing systems and strategic acquisitions. Despite facing customer concentration risks, pricing pressures, and geopolitical challenges, the company leverages its extensive patent portfolio and integrated product offerings to maintain competitive advantages primarily in North America, Canada, and select international regions. Future growth hinges on broader adoption of pinpoint stimulation technology, continued product innovation, and navigating supply chain complexities alongside regulatory environments.

Company Overview and Business Model

NCS Multistage Holdings, Inc. is a specialized oilfield services provider focusing on products and services that optimize well construction, completion, and development — largely for horizontal wells prevalent in unconventional reservoirs across North America plus selective international areas like the North Sea, Middle East, and Argentina [S1][S14][S19]. Its primary offering is fracturing systems enabling pinpoint stimulation where individual entry points are stimulated precisely during well completions. This technique enhances recovery efficiency when compared with conventional plug-and-perf or ball-drop techniques [S1][S5].

The company’s product suite also spans enhanced recovery systems facilitating controlled injection of fluids or gases to augment hydrocarbon production; well construction equipment such as casing buoyancy components; tracer diagnostics leveraging downhole chemical tracers to evaluate fluid flow and production profiles; and a controlling interest (50%) in Repeat Precision LLC that adds composite/dissolvable frac plugs plus machining services [S1][S19].

Historical Financial Performance

Over the last four years through fiscal 2023 (latest full year XBRL data), NCS Multistage exhibited substantial revenue growth recovering from pandemic lows but with profitability volatility:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 24 | 22 | 11 | +260.2% | ||

| 2024 | 7 | 13 | 4 | +309.1% | ||

| 2023 | 142 | -3 | 5 | -6 | -8.5% | -186.1% |

| 2022 | 156 | -1 | -1 | -2 | +31.3% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 21 | 18.8 |

| 2024 | 11 | 6.7 |

| 2023 | 3 | -3.4 |

| 2022 | -2 | -1.2 |

Source: SEC companyfacts cache [F1].

Revenue rebounded sharply during this period reflecting expanding activity in horizontal completions across North America post-2020 downturn [F1]. Operating income was negative until turning positive again recently as efficiencies improved.

The annual report released March 2026 states revenue reached $183.6 million for fiscal year ended December 31, 2025, up around +13% from $162.6 million in the prior year with net income markedly improving to $23.7 million versus just $6.6 million in 2024 [S5][F1]. Operating income was $10.54 million in FY2025 compared to only $4.33 million in FY2024 signaling better operating leverage [F1].

Operating cash flow rose strongly to $22.2 million in FY2025 from $12.7 million in FY2024 while capital spending remained prudent near $1.2 million resulting in free cash flow exceeding $20 million — a healthy cash generation profile for reinvestment or deleveraging [F1]. Equity capital stood at about $126 million at year-end.

Revenue Mix and Customer Dynamics

Approximately 60% of revenue stems from fracturing systems products/services including sliding sleeves which are consumables cemented inside well casings during completions alongside supervision services during hydraulic fracturing stages [S19]. Repeat Precision contributes about one-fifth of consolidated sales via frac plugs and ancillary tools [S19]. Well construction products like casing buoyancy systems account for around 10%, with tracer diagnostics making up the remaining approximately 10% after acquiring Reservoir Metrics LLC mid-2025 [S19].

Customer count expanded modestly to more than 230 clients in fiscal year 2025 from over 200 previously; however revenue concentration remains meaningful with the top five customers contributing close to one-third of total sales [S5][S11]. Following mergers among major E&P clients during the year, a single combined customer accounted for roughly 18% of revenue highlighting persistent customer concentration risks which could cause earnings volatility if spending patterns shift [S11].

Competitive Positioning & Moat

The company’s competitive differentiation rests heavily on proprietary technology protected by an extensive portfolio of patents — stated as comprising approximately 63 U.S. utility patents plus an equal number internationally covering core products such as sliding sleeves, frac isolation assemblies, casing buoyancy devices, and chemical tracers .[S7][S25]

Its R&D-led approach underpins ongoing innovation aligned with customer needs supporting operational benefits over more commoditized competitor offerings especially within Canada where it enjoys established presence [S25]. Additionally, controlling Repeat Precision leverages manufacturing expertise enhancing product integration.

Despite this moat foundation, NCS faces intense competition from larger multinational oilfield service firms that possess deeper pockets for R&D spending including AI-driven digital solutions alongside smaller local vendors who may have stronger regional ties or lower pricing models [S25]. The industry shift towards cost containment among E&P companies limits pricing power pressuring margins [S21].

Ongoing patent disputes notably in Canadian courts against Kobold Corporation introduce execution risk related to intellectual property enforcement which could affect market share or prompt royalty liabilities if adverse judgments materialize [S17].

Growth Opportunities & Constraints

Growth is linked largely to increased adoption of pinpoint stimulation techniques viewed as providing productivity enhancements on longer horizontal wells featuring more fracture stages—a trend continuing across North American shale plays [S21]. These complex wells require multiple consumables per well sequentially driving higher revenue per completion.

The firm also seeks expansion internationally targeting technically demanding hydrocarbon basins though faces elevated compliance hurdles including API/ISO certification demands plus operational risk factors like export controls and fluctuating regulatory regimes [S18].

Acquisitions serve as strategic levers evidenced by the purchase of Reservoir Metrics burgeoning tracer diagnostics capabilities for formation evaluation—an increasingly critical value-add amid field development optimization initiatives [S19].

Conversely, market constraints arise from capital expenditure volatility among customers due to commodity price swings; consolidation reducing overall vendor count; pricing pressures compounded by competitors’ discounted bids; tariff impacts affecting steel component sourcing; plus supply chain disruptions risking inventory imbalances or delayed deliveries [S26][S24].[N2]

Regulatory matters around environmental compliance particularly concerning fracturing fluids chemistry add complexity along with evolving safety requirements impacting operating costs [S23]. Cybersecurity threats represent additional emerging operational risks.[S9]

Capital Allocation & Financial Health

NCSM maintains a solid liquidity position supported by approximately $36.7 million cash/equivalents against current liabilities near $28.5 million yielding a strong current ratio above four-fold reflecting prudent working capital management at fiscal year-end December 31, 2025 [F1][S4].

Capital investments remain modest relative to operating cash flow generated: FY2025 capex was roughly $1.2 million versus operating cash flows above $22 million yielding substantial free cash flow approximating $20.97 million indicating disciplined reinvestment strategy focused on R&D rather than heavy fixed asset additions [F1].

Equity capital increased materially reaching about $126 million reflecting retained earnings accumulation alongside positive net income performance delivering an approximate return on equity near 18.8%, highlighting effective profit generation relative to shareholder base [F1].

Debt facilities described encompass an asset-based line of credit capped at $35 million imposing covenants restricting additional indebtedness or dividends potentially constraining financial flexibility especially if commodity market fluctuations strain customer spend or receivables quality [S4][S16]. The controlling interest entity Repeat Precision also has a promissory note facility expiring May 2026 adding refinancing considerations.[S15]

NCS historically executed minor share repurchases last noted before FY2018 indicating limited emphasis on buybacks within current capital allocation framework emphasizing balance sheet strength instead [F1]. Dividend payments are not prominently disclosed suggesting retention focus.

What to Watch Forward (Analysis)

Without explicit forward guidance publicly issued for post-2025 periods per filings, key monitorables will include:

- Market uptake rates for pinpoint stimulation amidst competitive well completion practices.

- Progress integrating ResMetrics tracer diagnostics into broader solution sets providing completion design optimization data benefits.

- Resolution outcomes of ongoing patent infringement litigation impacting Canadian operations potentially affecting intellectual property leverage.

- Supply chain developments especially raw material tariffs impacting cost structure plus potential inflationary pressures.

- Customer capital expenditure trends reflecting oil/gas price environment influencing demand visibility.

- Regulatory responses regarding hydraulic fracturing chemicals safety standards impacting tracer services.

- Covenant compliance under credit facilities given concentrated receivables base coupled with cyclicality inherent to upstream resource plays.

- Potential new acquisitions or partnership announcements expanding technological or geographic reach.

- Technological innovation velocity sustaining differentiation versus large integrated oilfield service competitors deploying AI/machine learning tools accompanying broader service packages.

Conclusion (Compliance Note)

This analysis summarizes NCS Multistage Holdings’ recent financial trajectory underscored by revenue growth and profitability improvements attributable to proprietary tech offerings within evolving oilfield services markets primarily centered around unconventional well completions across North America plus selected global regions.[F1] However it faces risks ranging from competitive intensity through patent disputes to supply chain vulnerabilities amplified by heavy revenue concentration among few customers.[S8][S11][S17] Watching adoption pacing of pinpoint stimulation technologies alongside operational execution managing regulatory/cost challenges are key bellwethers for sustaining earnings momentum going forward.

This report is prepared solely for informational purposes referencing publicly filed data and recent disclosures without provision of investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments