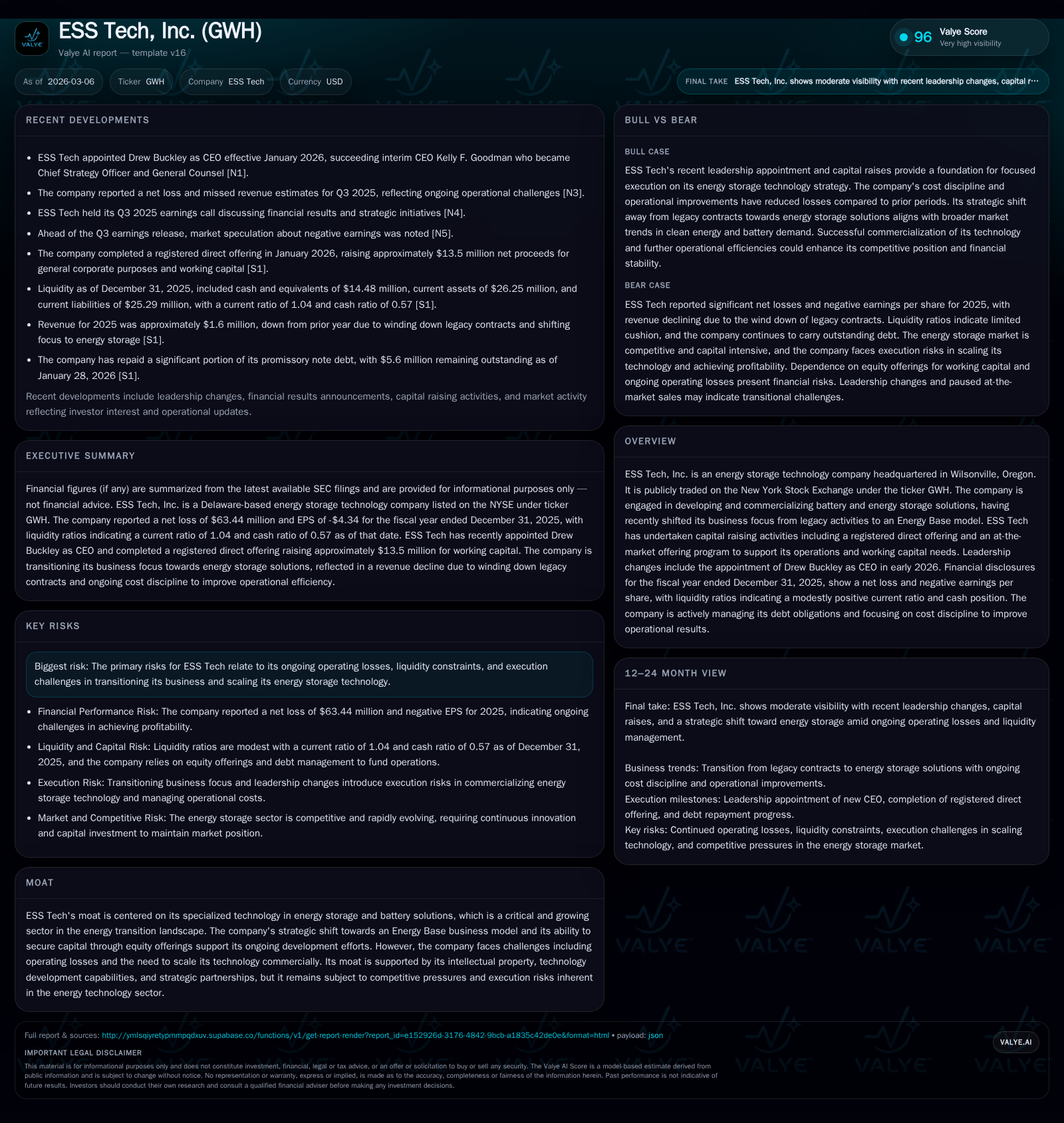

ESS Tech Shifts Gears with Iron Flow Battery Tech as Operating Losses Narrow

ESS Tech’s pivot towards scalable iron flow batteries aligns with policy support and capital management, yet execution risks remain.

ESS Tech, Inc. has steadily narrowed its operating losses from $105.5M in FY2022 to $57.4M in FY2025 while transitioning away from legacy offerings towards its Energy Base model grounded in iron flow battery technology. This shift leverages the advantages of earth-abundant materials, non-flammable electrolytes, and long duration cycling suited for grid-scale storage beyond lithium-ion capabilities. Federal legislative incentives under the Inflation Reduction Act and subsequent modifications bolster demand visibility and credit monetization prospects. Under new CEO Drew Buckley’s leadership, the company executed equity raises and debt repayments to preserve liquidity despite modest cash reserves. Profitability hinges on scaling production to unleash cost reductions, but challenges around commercial ramp timing, regulatory clarity, and supply chain robustness persist. Cash flow remains negative with an approximate -736% ROE, underscoring the need for disciplined capital allocation amid growth efforts.

From Legacy to Leadership: ESS Tech’s Historical Growth Trajectory

Between fiscal years 2022 through 2025, ESS Tech exhibited a notable trajectory of narrowing operating losses albeit still remaining deeply unprofitable. The company reduced its operating loss from approximately $105.5 million in FY2022 to $57.4 million by FY2025 — a substantial improvement of roughly 36% year-over-year versus FY2024's $89.8 million loss [F1]. Net income followed a similar pattern with a decline in net loss magnitude from -$77.97 million in FY2022 to -$63.44 million in FY2025.

Operating cash flow losses improved as well from -$81.62 million in FY2022 to approximately -$50.28 million in FY2025 [F1]. This tightening aligns with the company’s strategic pivot toward its Energy Base platform centering on iron flow battery technology while winding down legacy products like Energy Warehouse and Energy Center [S1]. Capex spending also contracted significantly over this period—from ~$14.2 million in FY2022 down to roughly $3.4 million in FY2025—indicating a disciplined approach to capital deployment amid transition [F1].

Despite this progress, equity reserves declined sharply from ~$137 million in FY2022 to just $8.6 million by year-end 2025—partly reflecting dilution effects from capital raises needed to fund operations [F1]. Overall, these dynamics portray a company still navigating the challenge of converting innovation into sustainable earnings while leveraging incremental improvements in cost control and investment prioritization.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -63 | -50 | -57 | 3 | +26.4% |

| 2024 | -86 | -72 | -90 | 7 | -11.1% |

| 2023 | -78 | -55 | -86 | 6 | +0.5% |

| 2022 | -78 | -82 | -105 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -54 | -736.1 |

| 2024 | -80 | -298.5 |

| 2023 | -61 | -75.1 |

| 2022 | -96 | -56.9 |

Source: SEC companyfacts cache [F1].

Iron Flow Batteries: Technology Advantages and Market Positioning

Central to ESS Tech's transformation is its proprietary iron flow battery technology based on non-flammable electrolyte chemistry composed chiefly of saltwater infused with iron—an abundant earth resource [S1]. Laboratory data indicate cycle-life durability exceeding 20,000 cycles without capacity fade—a stark contrast with lithium-ion chemistry which faces degradation challenges limiting effective cycle counts.

This aqueous electrolyte enables safer operation across a broad thermal window (-15°C to +50°C) and allows siting flexibility absent the fire risk lithium-ion batteries may pose at scale — critical for utility-scale grid applications and commercial-industrial energy assurance markets [S1]. The architecture is modular and scalable beyond eight-hour durations where levelized cost advantages versus lithium-ion compounds due to electrolyte volume-driven energy capacity gains rather than constrained cathode/anode designs.

ESS offers configurable Energy Base units at gigawatt-hour scales integrating battery stacks with advanced electrolyte health management systems—a feature enhancing operational longevity and performance consistency key for grid-storage reliability mandates [S1]. Such capability addresses the emerging market niche requiring long-duration energy storage (LDES) solutions supportive of renewable intermittency mitigation.

Legislative Incentives Supporting Future Demand for Long-Duration Storage

Legislative frameworks materially underpin ESS Tech’s market opportunity outlook. The Inflation Reduction Act (IRA), enacted August 16, 2022, extended Investment Tax Credits (ITCs) and Production Tax Credits (PTCs) inclusively for stand-alone battery storage projects through at least 2033 [S1]. This expansion underpins greater demand visibility for long-duration storage systems by improving project economic viability.

Further enhancements stem from the Inflation Reduction Optimization bill (OBBB) signed July 4, 2025 that modifies eligibility criteria including detailed Framework for Energy Original Components (FEOC) requirements affecting manufacturing localization and component sourcing thresholds [S1]. Section 45X PTCs offer battery manufacturers up to tens of dollars per kWh produced domestically—credits which can be refundable or sold on secondary markets providing margin uplift tailwinds.

The IRS finalized manufacturing definitions for these credits on October 28, 2024 clarifying qualification rules and enabling companies like ESS who maintain a domestic supply chain footprint to monetize these incentives robustly [S1]. These regulatory backstops support ESS's strategy positioning within U.S.-based clean energy infrastructure supply chains.

Capital Structure Tactics and Liquidity Management Under CEO Buckley

In early 2026 leadership changes culminated with Drew Buckley’s appointment as CEO tasked with solidifying financial footing alongside strategic execution [S7][S18][S24]. To bolster liquidity amid persistent operating losses (~$55M expected loss in FY2025), ESS Tech executed multiple equity raises including a January registered direct transaction yielding net proceeds near $13.5 million alongside an at-the-market offering program started November 2025 that was later paused after raising approximately $8.6 million [S16][S7].

Debt management efforts accompanied equity strategies; repaying ~$24.4 million or about 81% of a $30 million promissory note facilitated de-risking capital structure burdens though $5.6 million still remained outstanding as of late January 2026 [S16][S11]. Liquidity ratios reflected a modest current ratio near parity at approximately 1.04 driven by current assets ($26 million) marginally exceeding current liabilities ($25 million) as of December-end fiscal reporting [F1][S16].

Restrictions tied to recent financing include share ownership thresholds embedded within pre-funded warrant exercise terms limiting major stakeholder concentration while preserving capital raising optionality [S6][S16]. Despite cautious optimism over runway extension measures under Buckley’s tenure cash balances were limited (~$14.48 million at fiscal year-end), emphasizing close monitoring of burn rates relative to funding cadence [F1].

Assessing Profitability Pathways: Cost Reduction and Scale Efforts

Achieving competitive lifetime LCOS relative to incumbent lithium-ion technologies drives ESS’s operational playbook going forward [S1]. The scalable nature of iron flow batteries favors extended-duration applications where lithium-ion costs escalate non-linearly beyond ~8 hours due primarily to cathode limitations and safety system costs.

Ongoing scale-up aims not only to increase production volume but also optimize primary component sourcing—balancing raw material input costs against labor efficiencies within U.S.-based manufacturing nodes compliant with FEOC rules underpinning tax credit eligibility [S1]. Electrode active material fabrication represents a substantial cost vector addressed via process improvements expected during line maturation.

Cycle-life durability attributes further enhance comparative economics by extending system replacement intervals thereby amortizing fixed costs over longer operational timelines—a salient value proposition amidst growing renewable intermittency demands.

What Investors Should Monitor: Milestones and Market Risks Ahead

Explicit guidance remains modest given uncertainties in regulatory interpretations surrounding tax credit applicability post-OBBB enactment alongside potential delays inherent in commercialization ramps typical within advanced energy technologies [S1]. Monitoring rollout milestones such as commercial site deployments of Energy Base units will be critical alongside tracking supply chain stability affecting raw material continuity particularly given global geopolitical fluctuations impacting cobalt-free alternatives.

Competitive pressures continue unabated from rapidly advancing lithium-ion manufacturers expanding duration capabilities plus emergent flow chemistry startups targeting analogous market niches [S1]. Potential shifts in tariff regimes or additional legislative amendments could either bolster or constrain tax incentive frameworks thereby materially altering margin expectations.

Putting Returns Under the Microscope: Cash Flows, ROE, and Allocation Strategies

Financial return metrics underscore ongoing challenges faced by ESS Tech during this growth phase. Approximate return on equity was deeply negative at roughly -736% calculated from FY2025 net loss of $63.44 million against scant equity of $8.62 million [F1]. Free cash flow similarly remained negative at approximately -$53.67 million illustrating persistent outflows aligned with scale investments minus capex contractions reflective of conservative spend elevations [F1].

The absence of dividend distributions or share repurchase programs confirmed reaffirmation of reinvestment priorities over shareholder returns presently [S9][S18][F1]. Capital allocation emphasizes sustaining liquidity buffers while advancing technology commercialization milestones acknowledging the high-risk trajectory typical among cleantech pioneers entering nascent markets.

This analysis synthesizes public filings up to March 6th, 2026 without predictive judgments or investment advice; prospective readers should consider broader market conditions when interpreting operational progress indicators provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments