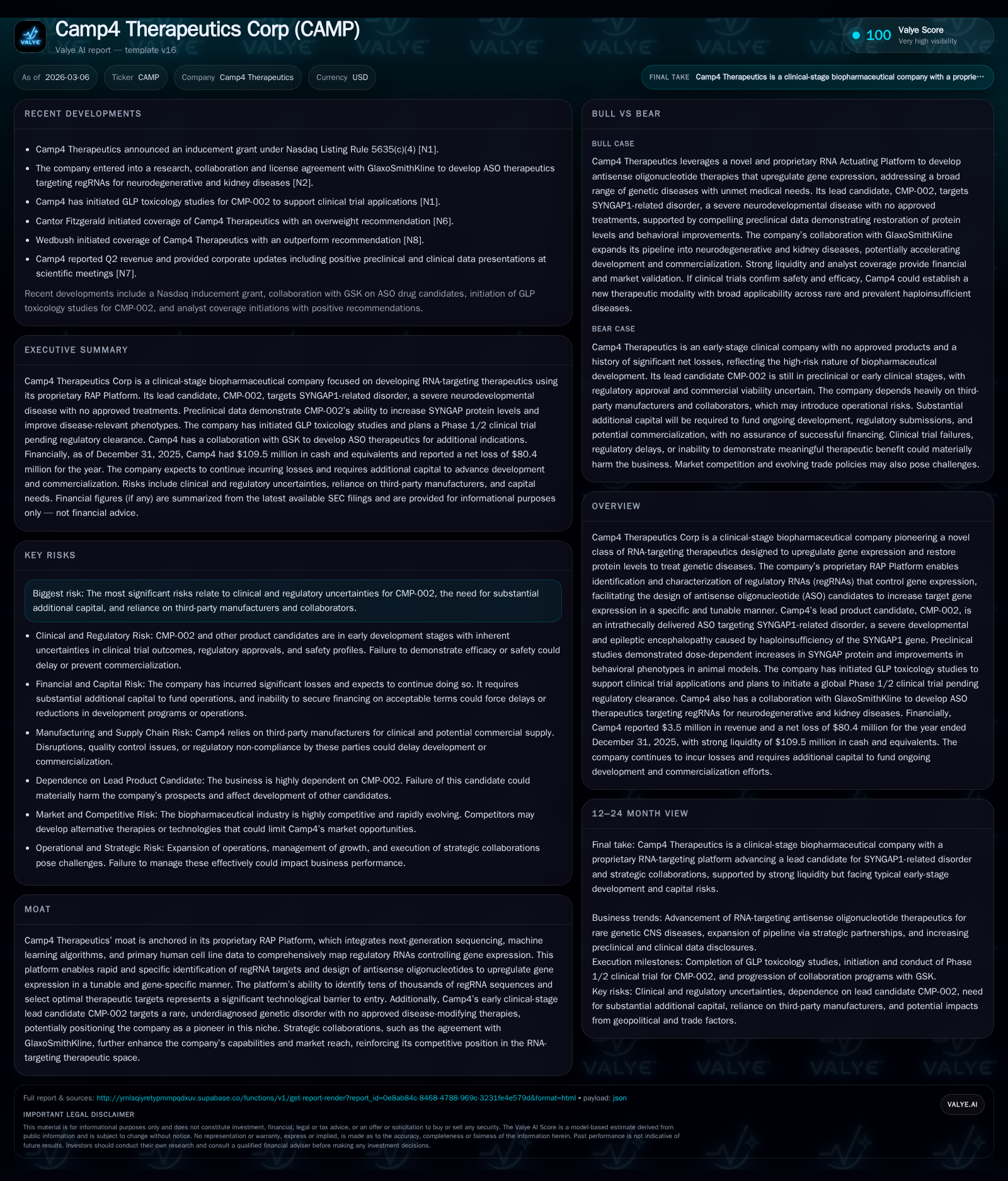

Camp4 Therapeutics Drives Innovation in RNA-Targeting Gene Upregulation Technology

Camp4 Therapeutics pursues gene expression modulation for SYNGAP1 disorder using its proprietary RAP Platform, confronting early-stage clinical and financial challenges.

Camp4 Therapeutics is advancing a unique RNA Actuating Platform (RAP) designed to upregulate gene expression via antisense oligonucleotides (ASOs) targeting regulatory RNAs. Its lead candidate CMP-002 targets the rare CNS genetic disease SYNGAP1-related disorder, with preclinical validation and GLP toxicology studies underway ahead of planned Phase 1/2 trials in H2 2026. The company reported revenue growth driven by grants and collaborations but with widening net losses due to increased R&D investments. Supported by a solid cash position exceeding $109 million, Camp4 faces risks from regulatory uncertainty, capital needs, and operational dependencies as it advances clinical development.

Innovative Technology Platform Powers Gene Expression Modulation

Camp4 Therapeutics has developed a proprietary RNA Actuating Platform (RAP) that represents a novel approach in gene therapy through targeting regulatory RNAs (regRNAs) with antisense oligonucleotides (ASOs). This platform combines high-resolution next-generation sequencing data, advanced machine learning algorithms, and insights from primary human cell lines to map tens of thousands of enhancers and promoters regulating gene expression.

Unlike traditional gene replacement or knockdown strategies often used in genetic disease therapeutics, Camp4’s approach focuses on upregulating endogenous gene expression by attenuating inhibitory regRNA elements at the transcriptional level. The platform identifies specific regRNAs tied to disease-associated genes and designs tunable ASOs that selectively bind these regulatory sequences. This enables precise amplification of the target gene’s messenger RNA (mRNA), theoretically restoring deficient protein levels with potentially fewer off-target effects.

Sector-native complexity lies in designing ASOs capable of achieving effective intrathecal CNS distribution while balancing stability and safety profiles. By anchoring their discovery engine around primary human CNS cells—a challenging tissue compartment for RNA therapeutics—the RAP Platform seeks to overcome common hurdles of delivery efficiency and translational relevance.

Development Progress: Advancing CMP-002 Toward Clinical Readiness

The front-runner asset emerging from Camp4’s platform is CMP-002, an intrathecally delivered ASO targeting SYNGAP1-related disorder—a rare neurodevelopmental condition caused by haploinsufficiency reducing functional SYNGAP protein by roughly half. SYNGAP1 disorder manifests as epileptic encephalopathy characterized by seizures, cognitive impairment, and developmental delays with no approved disease-modifying therapies currently available.

Preclinical evaluation demonstrated that intracerebroventricular administration of CMP-002 in haploinsufficient mouse models restored SYNGAP protein to near-normal levels after a single dose; furthermore, motor coordination and spatial learning deficits improved following a short dosing regimen. Non-human primate cynomolgus monkeys tolerated biweekly intrathecal doses well, showing dose-linear increases of SYNGAP proteins across brain regions implicated in the pathology.

To translate these findings into clinical development readiness, Camp4 has initiated Good Laboratory Practice (GLP) toxicology studies. Assuming favorable results and regulatory clearance, the company plans to initiate global Phase 1/2 clinical trials targeting individuals living with SYNGAP1 during the second half of 2026 [S1], [S3]. Given the rarity and underdiagnosis of this condition—estimated at approximately 21,000 patients across key western markets—these studies will likely face challenges associated with patient recruitment and endpoint selection.

Financial Profile: Rising R&D Expenses Amid Early-Stage Biopharma Challenges

Camp4’s financial profile reflects typical dynamics for a clinical-stage biotech focused on early development without commercial products. Revenue increased substantially from $0.65 million in FY2024 to $3.5 million in FY2025—a gain of +436.5%—driven largely by government grants and research collaborations rather than product sales [F1].

Operating income losses remained large but stable at approximately -$53 million in FY2025 versus -$53 million prior year (+1%), while net loss expanded materially from -$51.8 million to -$80.4 million (-55.2%) [F1]. The growth in net loss largely stems from ramped investments in preclinical work and preparations toward clinical trial launch alongside general administrative scaling.

Operating cash flow burn improved substantially: outflows declined by roughly one third (-35%) year-over-year from -$45.6 million to -$29.6 million due primarily to tighter spending controls despite increasing activities [F1]. Capital expenditures were minor (~$279k FY2025) consistent with a focus on trial readiness rather than fixed asset investment.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3 | -80 | -30 | -53 | +436.5% | -55.2% |

| 2024 | 1 | -52 | -46 | -53 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -30 | -168.5 |

| 2024 | -46 | -82.0 |

Source: SEC companyfacts cache [F1].

Table: Camp4 Therapeutics Historical Financials [F1]

The company ended FY2025 with approximately $109.5 million in cash & equivalents against modest current liabilities totaling ~$15.5 million—translating into a robust current ratio above 7x [F1]. Recurring net losses yield an approximate trailing return on equity near -168%, underscoring ongoing equity dilution pressure [F1]. Free cash flow remains deeply negative at nearly $29.8 million annually when combining operating cash flow with capital expenditures [F1].

Intellectual Property and Strategic Collaborations Reinforce Competitive Edge

Camp4 anchors its technological moat firmly through extensive intellectual property protection covering its RAP Platform discoveries as well as therapeutic ASO candidates directed at regRNAs [S1]. This IP portfolio acts as both a deterrent against competitor encroachment and a value proposition validating investment interest.

Strategic alliances notably include collaboration agreements with major pharmaceutical players such as GlaxoSmithKline (GSK), which contribute capital and provide access to development expertise and commercialization channels [S1]. Such partnerships indicate external confidence in both platform robustness and corporate strategy amid competition from other RNA technology innovators.

Navigating Regulatory and Operational Risks in Clinical Development

Despite technological promise, Camp4 faces considerable risk centered on clinical-stage uncertainties inherent to first-in-class RNA upregulators like CMP-002 [S1], [S4]–[S6]. These include:

- Ambiguity over safety profiles given intrathecal administration demands strict tolerability requirements.

- Potential delays or failures in GLP toxicology studies that could stall or jeopardize IND submission.

- Reliance on third-party manufacturers for GMP supply introduces vulnerabilities related to capacity constraints or quality control lapses.

- Complex healthcare laws governing marketing practices require vigilant compliance efforts given scrutiny on pharmaceutical conduct [S4]–[S16].

Operational execution risks span patient enrollment challenges typical for ultra-rare CNS disorders plus evolving FDA regulatory landscapes typified by shifting interpretations post major court decisions [S22]. Financial strain from continuous negative cash flows adds further uncertainty regarding timely milestone achievements without additional capital raises.

Capital Allocation: Cash Position Supports Near-Term Operations Amid Ongoing Losses

The company maintains defensible liquidity with cash reserves surpassing $109 million at fiscal year-end enabling near-term execution of planned GLP studies and initial clinical trials [F1]. The low current liability load combined with sizable current assets permits flexible resource deployment while managing burn rate prudently.

However, expansive net losses—growing over fifty percent year-on-year—and persistently negative free cash flow necessitate vigilant capital management strategies moving forward [F1]. Absent meaningful product revenues from commercialization—as expected given preclinical stage—the firm must anticipate multiple financing rounds or partnership deals to sustain operations beyond initial Phase 1/2 readouts.

Capital allocation choices will critically influence whether Camp4 can continue agile platform enhancement alongside competitive lead candidate progression without excessive shareholder dilution.

Outlook: Milestones to Monitor for Investors

Foremost near-term catalysts include successful completion of GLP toxicology evaluations critical for IND submission readiness targeted toward global Phase 1/2 trial commencement planned for H2 2026 [S3]. Progress on enrollment logistics for this first-in-human trial will be closely watched given rarity of SYNGAP1 disorder patients.

Beyond CMP-002 advancement, trajectory updates on RAP Platform enhancement efforts—such as identification of additional druggable regRNA targets—and dealmaking activities hold strategic importance as they validate platform scalability prospects.

From an analytical perspective:

- Demonstration of CNS delivery safety/tolerability may substantially de-risk subsequent pipeline endeavors leveraging the same modality.

- Market acceptance factors hinge on achievement of robust efficacy signals plus alignment with payors given specialty therapy cost sensitivities within ultra-rare disease frameworks.

- Capital availability remains critical; failure to secure follow-on funding on reasonable terms could more negatively impact timelines than technical feasibility alone.

In sum, Camp4 Therapeutics embodies emerging science intersecting unmet medical need tempered by standard early-stage development risks common across innovative RNA therapeutic companies.

Disclaimer: This report is prepared solely for informational purposes based on publicly available filings dated through March 6, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments