Bluejay Diagnostics’ Journey Toward FDA Clearance: Financial Challenges and Clinical Milestones

Bluejay Diagnostics advances its Symphony IL-6 diagnostic platform with pivotal clinical trial progress, facing significant capital demands and regulatory timelines.

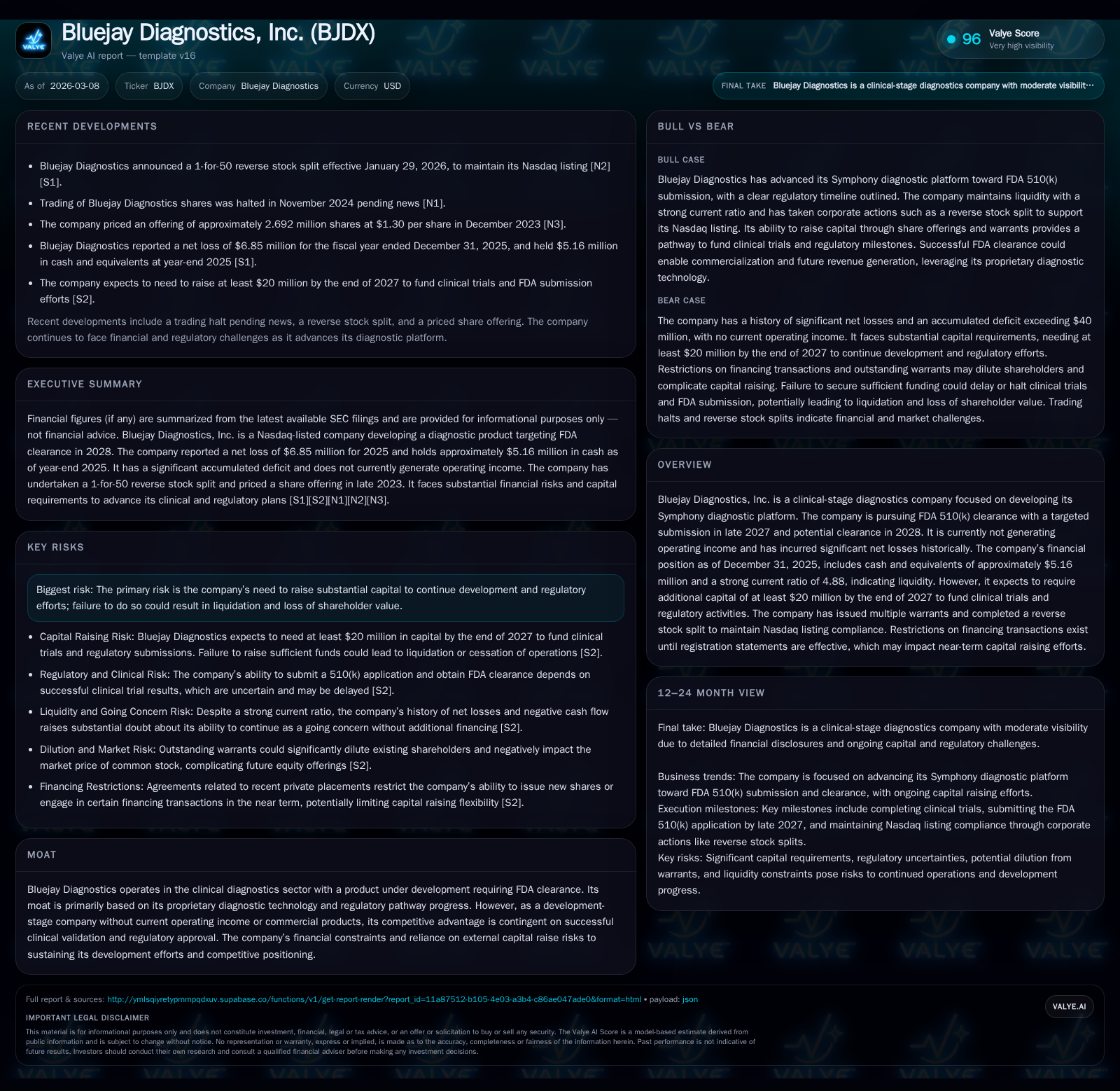

Bluejay Diagnostics is a clinical-stage company developing the Symphony platform designed to provide rapid IL-6 immunoassay testing for sepsis management in critical care. While its Symphony device demonstrates promising clinical utility potential, the company remains pre-commercial with no operating income and an accumulated deficit exceeding $40 million as of 2025. Bluejay aims for FDA 510(k) clearance by late 2027 but must navigate steep financial challenges, including a cash runway of just over $5 million and an urgent need to raise at least $20 million by year-end 2027 to sustain clinical trials and manufacturing upgrades necessary for regulatory submission. The firm has employed aggressive reverse stock splits and numerous warrants to comply with Nasdaq requirements and finance operations, complicating its capital structure and dilution risk profile.

From Pre-Clinical Development to Market Readiness: Tracing Symphony's Progress

Bluejay Diagnostics’ flagship Symphony platform is engineered as a near-patient diagnostic system aimed primarily at critical care environments such as ICUs and emergency rooms. The platform consists of a dedicated analyzer paired with single-use cartridges capable of conducting rapid immunoassays for interleukin-6 (IL-6), a biomarker widely recognized for its role in inflammatory response severity assessment—particularly sepsis prognosis. The Symphony IL-6 test is intended to produce laboratory-quality results in approximately 20 minutes using whole blood samples.

Since its pre-clinical phase completion, Bluejay transferred key manufacturing technology from Toray Industries to Sanyoseiko’s FDA-certified contract facility during 2026 [S1]. This transition reflects industry-standard approaches toward scaling manufacturing that complies with stringent FDA quality controls essential ahead of a 510(k) submission. Symphony’s manufacturing process is undergoing modification to overcome technical barriers that could impair diagnostic performance reliability—a crucial step before regulatory submission [S1]. The emphasis on immunoassay precision and reproducibility aligns with sector expectations where robustness and analytical validation underpin payer acceptance and clinical adoption.

Currently, Symphony remains unapproved by the FDA without commercial sales generated. Its future hinges on successful clinical validation and regulatory authorization.

Revenue Stagnation and Deepening Operating Losses: Historical Financial Portrait

Financially, Bluejay Diagnostics exhibits typical developmental stage burdens marked by flat revenues yet rising net deficits signaling ongoing investment in R&D without offsetting income streams. Revenue was approximately $249K in FY2022 with no year-over-year growth evident by end-2025 [F1]. This figure represents minimal service income or grant funding but no recurring commercial revenue.

Operating losses hovered near $7 million annually with net income losses paralleling this trend closely ($6.85M loss in FY2025) [F1]. Operating cash flow consistently negative ($6.05M outflow in FY2025) accentuates the burn rate challenge amid marginal capital expenditure reductions reflecting tightened discretionary spending [F1]. Meanwhile, equity reported dropped from over $11.5M in FY2022 to about $6M in FY2025 signaling accumulated deficits consuming shareholder value [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -7 | -6 | -7 | +11.3% | ||

| 2024 | -8 | -8 | -7 | +22.5% | ||

| 2023 | 249040 | -10 | -8 | -10 | 0.0% | -7.1% |

| 2022 | 249040 | -9 | -8 | -9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -114.6 |

| 2024 | -8 | -134.7 |

| 2023 | -9 | -343.8 |

| 2022 | -9 | -80.6 |

Source: SEC companyfacts cache [F1].

The approximate return on equity stands at about -115% given net income relative to equity as of FY2025 [F1], underscoring the absence of profitability typical for companies relying entirely on investor funding for development phase work.

Clinical Trial Advances: SYMON-II Pivotal Study Updates and Implications

Bluejay’s lead clinical effort is the SYMON-II pivotal trial targeting enrollment of approximately 750 ICU patients to consolidate findings from an earlier pilot (SYMON-I). As disclosed in early 2026 filings [S1], about 583 patients have already been enrolled—a substantial portion indicating momentum toward study completion.

This trial seeks to clinically validate IL-6 measurements as predictive markers for all-cause mortality within a critical care population over a standard follow-up period (28 days). Demonstrating statistically significant prognostic performance in such settings is critical for FDA's acceptance under the device premarket notification pathway (510(k)), particularly when predicate devices exist but may lack Symphony’s rapid turnaround features.

The trial design aligns with common diagnostics sector precedence emphasizing real-world clinical utility endpoints alongside technical assay performance metrics. Finalizing this study successfully will be an important value inflection point potentially enabling regulatory filings and subsequent commercialization.

FDA 510(k) Submission Timeline and Regulatory Hurdles Ahead

Bluejay anticipates submitting its Symphony platform for FDA clearance via the traditional 510(k) route in late 2027 with possible clearance earliest in Q3/2028 pending satisfactory clinical outcomes [S1,S2]. Regulatory filings will require comprehensive demonstration not only of clinical validity but also manufacturing process control advancements now underway given prior technical challenges highlighted earlier [S1].

FDA review times for diagnostics under the streamlined premarket notification framework typically range from several months up to one year depending upon review complexity; these timeline estimates align with industry norms.

However, delays or underperformance in clinical data generation or unresolved manufacturing issues could extend timeline risks materially beyond stated guidance [S1,S2], impacting commercial preparedness.

Capital Structure Dynamics: Reverse Splits, Warrants, and Financing Restrictions

To uphold Nasdaq Capital Market listing criteria amid prolonged share price pressures frequently faced by clinical-stage biotechs without revenues generating positive EPS trajectories [S1], Bluejay has implemented four reverse stock splits totaling an aggregate ratio of approximately one-for-32,000 since mid-2023 [S1,S6,S7]. Such substantial consolidation significantly reduced share count but also compresses liquidity float adversely affecting trading volumes.

Further complicating its capital structure are multiple outstanding warrants granted across recent private placement offerings with strike prices ranging broadly from fractional cents up to double digits per share [S4,S9]. Collectively these warrants represent several multiples of common shares outstanding which magnifies dilutive risk if exercised fully.

Additionally restrictive covenants stemming from registration rights agreements mandate delays on certain financing transactions until relevant resale registration statements are declared effective by the SEC—imposing near-term limitations on raising new capital mechanically linked to warrant registrations [S4,S9].

Overall these warrant overhangs combined with reverse split impacts create a challenging environment balancing the need for shareholder base stability against inevitable dilution required to fund lengthy regulatory paths common in diagnostics innovation sectors.

Cash Burn, Capital Needs, and Liquidity Risks Through 2027

As of December 31st, 2025 Bluejay held roughly $5.16 million in cash equivalents with total current assets around $5.46 million versus only about $1.12 million current liabilities yielding a healthy current ratio near 4.88 which indicates solid short-term liquidity coverage [F1].

Despite this apparent liquidity cushion the company forecasts requiring at least an additional $20 million by end-2027 fiscal year funding continued clinical trials (SYMON-II completion), resolution of cartridge manufacturing process enhancements at Sanyoseiko facility and preparation for FDA submission filing activities [S1,S2,S4].

Given persistent negative operating cash flows running about $6 million annually combined with likely increased spending ramp associated with final trial stages plus manufacturing scale-up preparations this projected funding gap appears realistic. Restrictions resulting from purchase agreements place practical constraints hindering immediate capital raises until SEC registration statements are effective further heightening financial risk exposure through midterm horizons [S4,S9].

Such liquidity stress scenarios are common among diagnostics device developers many years away from revenue generation highlighting the importance of securing sufficient bridge financing or strategic partnerships timely.

Capital Allocation Strategy: No Dividends or Buybacks Amid Funding Pressures

Reflecting typical strategy among developmental-stage healthcare technology firms,the company has neither declared nor paid any dividends historically nor engaged in share repurchase programs at any point through latest reporting periods [F1,S6,S7].

Capital allocation focus remains tightly directed toward sustaining research & development initiatives including SYMON-II trial advancement plus manufacturing improvements necessary ahead of anticipated commercial launch in post-clearance years.

For investors accustomed to biotech or diagnostics firms still years away from profitability this lack of immediate capital return aligns logically with operational priorities emphasizing value creation through product development milestones rather than yield generation.

Investor Considerations: What To Watch in Bluejay’s Upcoming Milestones

Key forthcoming events serving as critical checkpoints include:

- Completion of SYMON-II enrollment near target patient numbers (~750) which will enable commencement of data analysis phases;

- Disclosure dates relating to pivotal trial outcome metrics validating IL-6 prognostic utility;

- Progress updates regarding final manufacturing process qualification steps at contract manufacturer Sanyoseiko;

- Formal FDA pre-submission communications potentially clarifying evidentiary expectations;

- Successful effectiveness declaration of resale registration statements facilitating additional fundraising efforts;

- Execution or announcement of new financing tranches totaling or exceeding the estimated $20 million need before end-2027; These milestones combine operational signals informing strategic value assessments while highlighting inherent risks related to financing sufficiency amid protracted regulatory timelines. Investors should closely monitor official communications around these pivot points as they will materially influence Bluejay’s trajectory toward commercialization potential balanced against capital structure dilution dynamics.

This report synthesizes publicly disclosed financial statements and SEC filings as well as corporate statements regarding Bluejay Diagnostics’ technology development journey. It aims solely to provide an analytical overview grounded strictly in verified disclosures without prescribing specific investment actions. The company’s path remains contingent on successful regulatory clearance efforts supported by adequate capitalization amid competitive clinical diagnostics landscape dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments