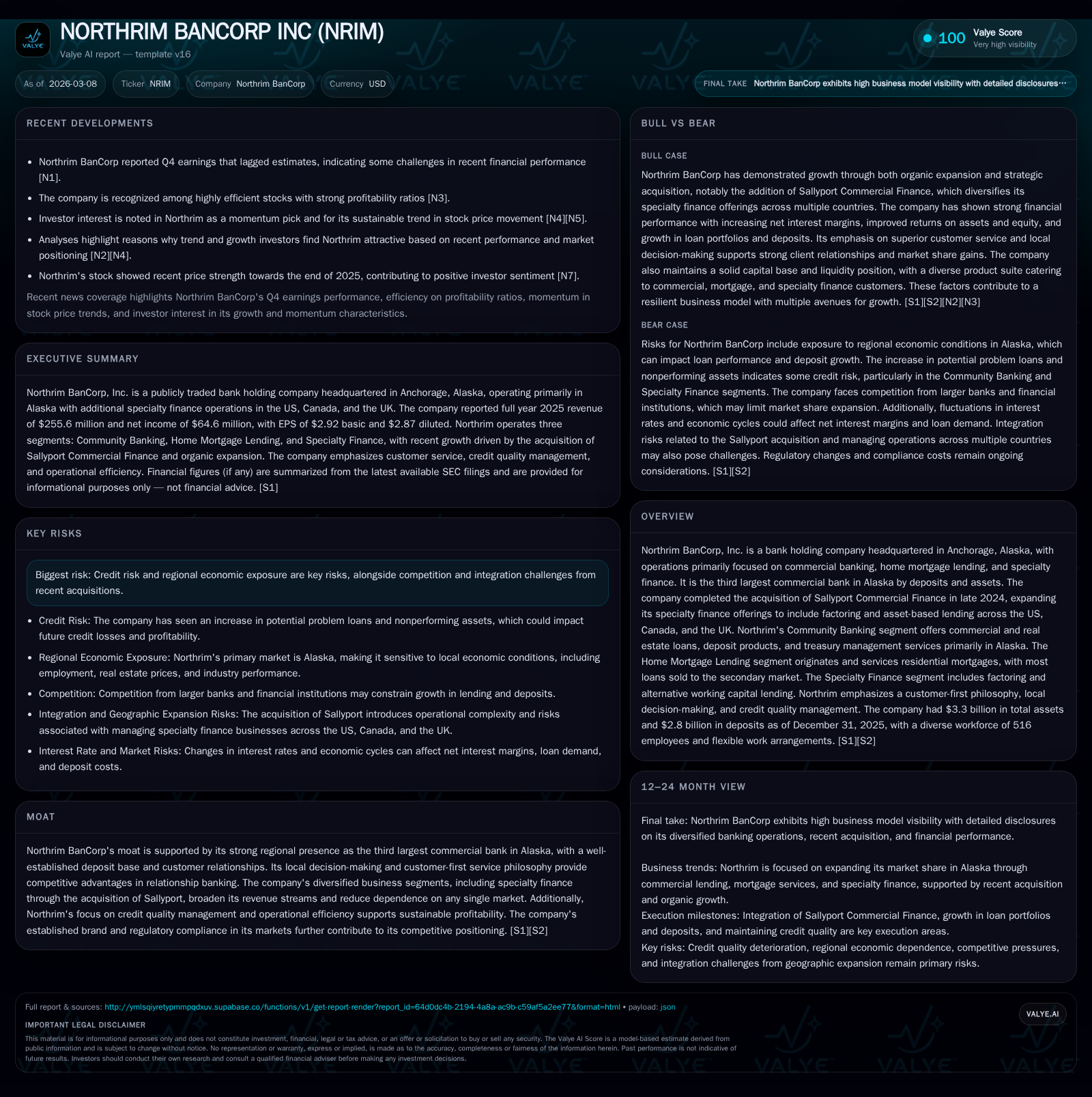

Northrim BanCorp's Expansion and Strong Alaska Roots Drive Record 2025 Performance

The company balances regional dominance with specialty finance growth following its Sallyport Commercial Finance acquisition.

Northrim BanCorp, Alaska’s third-largest commercial bank by deposits, posted notable growth in 2025 fueled by organic expansion and its recent acquisition of Sallyport Commercial Finance. The acquisition extends Northrim's footprint beyond Alaska into the U.S., Canada, and UK specialty finance markets. Despite regional economic exposures and integration risks, Northrim exhibits robust credit quality management and operational efficiencies that underpin its profitability. The bank maintains a solid capital position with strong cash flow generation, moderate dividend payouts, and paused share repurchases amid regulatory and market considerations.

Company Background and Historical Growth

Northrim BanCorp, Inc., headquartered in Anchorage, Alaska, is the state’s third-largest commercial bank based on deposits and assets, emphasizing community-oriented banking coupled with specialty finance services.[S1][S11] The company’s banking operations began in December 1990 and has operated as a holding company since December 2001. Its business comprises three segments: Community Banking focused on Alaskan markets; Home Mortgage Lending primarily generating residential mortgages sold to the secondary market; and Specialty Finance expanded nationally following the October 2024 acquisition of Sallyport Commercial Finance LLC.[S1][S11]

Financially, Northrim delivered strong growth with revenues rising from $195.96 million in 2024 to $255.58 million in 2025,[F1] representing a year-over-year increase of 30.4%. Net income improved from $36.97 million to $64.61 million over the same period,[F1] an increase of nearly 75%, underscoring enhanced profitability supported by revenue growth and operational leverage.

Financial Summary Table

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 256 | 65 | 139 | 5 | +30.4% | +74.8% |

| 2024 | 196 | 37 | -9 | 1 | +45.6% | |

| 2023 | 25 | 39 | 6 | -17.4% | ||

| 2022 | 31 | 78 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 15 | 0 | 134 |

| 2024 | 14 | 1 | -9 |

| 2023 | 14 | 9 | 33 |

| 2022 | 11 | 14 | 74 |

Source: SEC companyfacts cache [F1].

Note: Financial figures reflect substantial improvement driven by strategic initiatives including acquisitions.

Business Segments and Drivers of Growth

Community Banking

This segment retains a dominant regional presence within Alaska, offering commercial loans, real estate financing, deposit products, and treasury services.[S11][S27] As of December 31, 2025, total deposits were approximately $2.81 billion,[S11] supporting a loan portfolio exceeding $2.2 billion.[S8]

Growth is primarily driven by demand for commercial real estate loans—especially non-owner occupied properties—and commercial & industrial lending linked to sectors such as oil & gas.[S8][S17] Localized decision-making enhances responsiveness to customer needs relative to larger national banks.

Home Mortgage Lending

Through Residential Mortgage LLC, Northrim originates mainly conforming residential mortgages that are mostly sold to secondary market entities like the Alaska Housing Finance Corporation (AHFC).[S11] Retention of servicing rights provides ongoing fee income with stable origination volumes supporting revenue consistency.

Loan products include government-backed FHA/VA loans alongside conventional mortgages tailored for Alaska's housing market characteristics.[S11]

Specialty Finance

Following the October 2024 acquisition of Sallyport Commercial Finance LLC,[S1] this segment now offers factoring, asset-based lending, and alternative working capital solutions across the U.S., Canada, and the United Kingdom.[S1][S14]

This diversification into specialty finance—with generally shorter duration assets but potentially higher yields—provides revenue stability during economic volatility while complementing traditional community banking income streams.[S27]

Credit Quality and Risk Management

Credit risk remains a key focus due to Northrim’s geographic concentration in Alaska’s economy, vulnerable to fluctuations in oil & gas and other cyclical sectors.[S17][S23] The company monitors portfolio concentrations across industries including healthcare, tourism, accommodations, retail trade, aviation outside tourism, restaurants/breweries, and fishing—all material sectors within Alaska.[S17]

Nonperforming loans were controlled at around $11 million as of September 30, 2025,[S22] supported by rigorous internal credit administration aligned with FDIC guidelines including annual loan reviews and comprehensive underwriting policies.[S19][S29]

Allowance for credit losses increased modestly consistent with conservative provisioning reflecting current economic assessments.[S15]

Capital Structure and Liquidity Position

Northrim maintains capitalization comfortably above regulatory "well-capitalized" thresholds.[S24] Equity grew from approximately $267 million at December 31, 2024 to about $326 million at year-end 2025,[F1] supporting strategic lending capacity.

Liquidity is robust with stable deposit funding comprising roughly 86% transaction accounts as of September '25,[S21] supplemented by borrowing facilities including Federal Home Loan Bank lines totaling hundreds of millions of dollars available as collateralized advances.[S9][S15]

Operating cash flow was strong at $139 million for fiscal year 2025,[F1] a substantial recovery from prior negative flows tied partly to loan sales and improved earnings quality.

Capital expenditures remained moderate at $5.47 million,[F1] focusing on infrastructure enhancements rather than major expansions.

Capital Allocation: Dividends and Share Repurchases

The company paid dividends totaling $14.5 million in fiscal year 2025,[F1][S10] representing a balanced payout relative to earnings that supports both shareholder returns and retained capital for growth.

There were no share repurchases during the year,[F1] with the Board currently not authorizing buybacks for 2026 amid regulatory scrutiny including Basel III considerations affecting capital management strategies.[S10][N1]

Future Growth Prospects Analysis

Northrim’s outlook depends on several factors:

- Continued recovery in Alaska’s economy driven by oil & gas sector job growth and construction activity may boost loan demand in Community Banking.[S2]

- Integration of Specialty Finance operations provides new revenue channels across North America and the UK but entails execution risks associated with cross-border operations.[S1]

- Maintaining credit quality amidst inflationary pressures requires vigilant portfolio oversight given borrower repayment risks.[S25]

- Mortgage origination volumes will be influenced by housing market conditions intertwined with interest rate movements affecting refinancing activity.

- Regulatory changes related to capital adequacy or dividend policies could impact shareholder return strategies or lending capacity.[S10][S23]

Milestones & What To Watch (Analysis)

- Assess post-acquisition synergy realization within Specialty Finance impacting earnings diversification.

- Monitor deposit growth trends especially large account concentrations influencing liquidity risk.

- Track shifts in problem asset levels or loan rating migrations signaling credit condition changes.

- Observe regulatory developments potentially affecting dividend distributions or capital requirements.

- Follow macroeconomic trends impacting Alaska’s key industries such as energy prices influencing loan demand.

Conclusion: Positioning Between Local Strengths & Broader Ambitions

Northrim BanCorp combines deep regional expertise with strategic expansion into specialty finance markets beyond Alaska through its Sallyport acquisition.[S1][F1] The firm demonstrated significant year-over-year improvements in revenues and profitability underpinned by prudent credit risk management essential given its geographic concentration exposure. Capitalization remains solid providing flexibility for measured shareholder returns without compromising growth investments or regulatory compliance.[F1][S24] While challenges persist from credit risk tied to Alaska's cyclical economy alongside operational complexities from international specialty finance activities,[S17][S23] Northrim’s disciplined approach positions it well for steady progression toward broader market relevance beyond its traditional footprint.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments