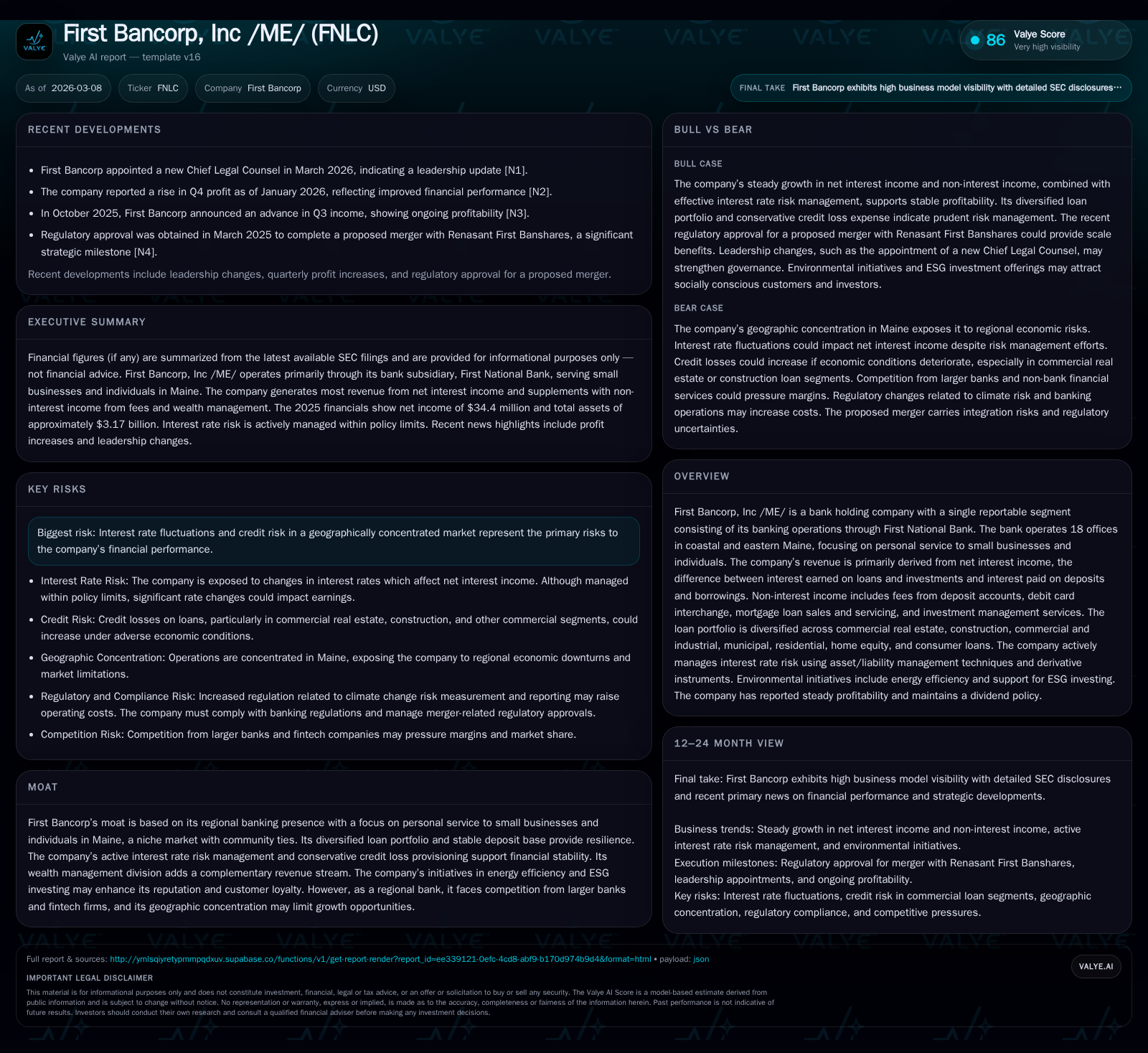

How First Bancorp Leverages Interest Rate Management and Local Ties for Sustainable Expansion

First Bancorp's disciplined asset/liability management and community-centric approach underpin its steady financial growth within Maine's regional banking sector.

First Bancorp, Inc /ME/ has demonstrated solid net income growth driven by robust net interest income expansion amidst variable interest rate conditions. The bank's diversified loan portfolio, anchored in Maine’s small business and individual client base, supports stable earnings while active interest rate risk management via ALCO mitigates repricing volatility. Its capital ratios remain comfortably above regulatory thresholds, supporting a consistent dividend policy with minimal share repurchases. Going forward, geographic concentration and competitive pressures may constrain growth potential, but strategic ESG initiatives and evolving fee income streams provide avenues for diversification and operational resilience.

Historical Earnings Growth and Revenue Drivers Through 2025

First Bancorp has steadily progressed its profitability with a notable acceleration in FY2025. Net income rose about 39.7% year-over-year to $10.17 million [F1], reflecting a combination of increased net interest income spurred by growth in loan balances and lending spreads as well as efficient asset-liability management [S1]. The bank primarily earns through the spread between interest on loans/investments and funding costs on deposits/borrowings—the net interest margin dynamic is critical here. Despite some volatility in market rates, the company has maintained moderate exposure with ALCO oversight ensuring balance sheet repricing alignment [S1].

While net interest income dominates revenue composition, non-interest sources such as deposit fees and debit interchange also add stability. Operating cash flow notably improved by 45.2% in FY2025 to $37.8 million alongside capex rising to a still-moderate $3.22 million consistent with branch modernization efforts [F1]. This financial trajectory underscores a methodical expansion path rooted in regional service.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 10 | 38 | 3 | +39.7% |

| 2024 | 7 | 26 | 1 | +9.0% |

| 2023 | 7 | 37 | 3 | -27.4% |

| 2022 | 9 | 41 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 16 | 282000 | 35 |

| 2024 | 16 | 212000 | 25 |

| 2023 | 15 | 250000 | 34 |

| 2022 | 15 | 277000 | 40 |

Source: SEC companyfacts cache [F1].

Note: ROE calculated as net income divided by year-end equity.

Loan Portfolio Composition and Interest Rate Risk Management

The bank's loan book—totaling over $2.39 billion—is diversified across key segments: commercial real estate (both owner-occupied and non-owner), construction loans supporting regional development projects including energy efficiency initiatives,[S7][S12] municipal loans backed by local government entities,[S7] residential mortgages including home equity lines of credit,[S10] and consumer installment loans.[S8][S11]

Credit quality management employs rigorous allowance for credit losses built on discounted cash flow models incorporating prepayment speeds and historical benchmark data.[S7] Qualitative overlays account for policy shifts or economic condition changes relevant to Maine’s localized economy.

On the exposure side of interest rate risk—which could materially affect net interest margins given rate volatility—ALCO governs via static gap analysis comparing repricing profiles of assets vs liabilities.[S25] The one-year cumulative repricing gap contracted slightly from (15.98)% to (13.24)% of total assets year-over-year but remains well within the board-set +/-20% limit.[S25]

The bank also utilizes derivative hedging instruments (interest rate swaps/floors/caps) totaling $235 million notional with counterparties rated A- or better to mitigate abrupt earnings fluctuations due to rising rates.[S12][S25] This use of hedges aligns with best practice in regional banks managing tight spreads amid economic cycles.

Mortgage prepayment modeling helps refine cash flow estimates considering coupon ranges and loan ages—important for accurately anticipating timing of principal repayments affecting asset repricing schedules.[S25]

Evolving Non-Interest Income Streams Supporting Diversification

Although First Bancorp derives most revenues from net interest spread expansion,[S1] non-interest income constitutes a meaningful secondary pillar encompassing dealer interchange from debit cards issued to consumer accounts plus fees from deposit accounts such as maintenance/service charges.[S1]

Mortgage banking activities generate fee income from both sales and ongoing servicing rights—a typical regional bank revenue diversification lever benefiting from active real estate markets even if localized.[S1] Complementing this is First National Wealth Management services that provide investment advisory and private banking offerings tailored for the local affluent segment with ESG-aligned portfolios increasingly requested by clients.[S1]

This diversification into fee-based products represents a strategic second revenue stream reducing sole dependence on cyclical lending margin dynamics characteristic of mid-sized national banks.

Balance Sheet Strength and Capital Adequacy Metrics

Capitalization at First Bancorp remains robust: common equity Tier 1 capital ratio stood at 12.84% against a regulatory minimum of 4.5%, Tier 1 capital ratio was identical at 12.84% above the required minimums.[F1][S5] Total risk-weighted assets approximated $2.21 billion while the tier one leverage ratio was a strong 8.84% versus a floor of 4% documented at year-end FY25.[F1][S5]

Such buffers provide significant cushion above prompt corrective action triggers, reflecting conservative capital management despite incremental shareholder returns. Off-balance-sheet credit exposures—largely commitments and guarantees—amounted to approximately $130 million with allowances reflecting prudent provisioning levels.[S7]

The company maintains sizable liquidity positions including available credit facilities ($101 million correspondent bank lines plus $313 million Federal Reserve Board facility), none drawn as of FY25 end,[S11][S23] supporting flexibility amid local market cyclicality or broader liquidity shocks.

Dividend Policy, Share Repurchases, and Shareholder Returns

First Bancorp has exhibited disciplined capital return policies underpinning shareholder value with reported dividends exceeding $16 million in FY25,[F1] consistent with gradual annual growth aligning closely with earnings performance. Conversely buybacks remain modest ($282 thousand in FY25), signaling preference for sustaining dividend reliability over expansive repurchasing amid current profitability levels.[F1] Return on equity measured near 3.6% implies operational headroom exists should leverage or expense efficiencies improve over time fostering enhanced returns on invested equity capital.[F1]

Capital deployment thus favors steady payout progression complemented by cautious share repurchase reflecting industry norms amongst community-focused mid-sized banks contending with limited scale economics externally.

Forward-looking Considerations: Growth Opportunities and Market Constraints

Recent corporate governance shifts include appointment of new Chief Legal Counsel early-2026,[N1] potentially influencing future strategic execution frameworks especially governance around compliance or regulatory adaptation. Market-wise First Bancorp's geographic concentration exclusively along coastal/eastern Maine inherently restricts scale-driven growth potential; localized economic conditions heavily influence borrower credit quality particularly tied to real estate sectors endemic there.[S4] Competition intensifies from larger regional/national banks entering Maine’s market alongside fintech firms advancing deposit plus lending tech platforms targeting similar small business clientele could pressure margins or customer retention creating headwinds absent product innovation or partnership moves. Management’s continued ESG integration alongside expanding energy efficiency lending programs offers niche growth vectors possibly unlocking new client segments aligned with prevailing sustainability trends locally.[S1] A cautious economic outlook prevalent across broader U.S./regional perspectives necessitates vigilance towards potential credit deterioration especially in construction or commercial real estate portfolios sensitive to rate hikes or economic slowdowns.[S4]

Operational Initiatives: ESG Efforts and Tech Adoption in Banking Services

The bank champions several operational sustainability efforts including installation of LED lighting across multiple offices, elimination of courier runs reducing fuel usage, and implementation of geothermal systems during recent branch buildouts—all contributing measurable carbon footprint reductions without impairing operational effectiveness.[S1] Digital transformation initiatives promote customer adoption of electronic statements, increase remote video conferencing cutting employee travel needs, as well as embracing fintech solutions enabling streamlined wealth management offerings compatible with responsible-investing mandates gaining traction among clientele.[S1] Investments in green bonds support portfolio ESG alignment adding reputational plus financial benefits absent material operational cost impacts.[S1] These measures position First Bancorp advantageously amidst growing community expectations around corporate responsibility while fostering cost avoidance through efficiency gains.

Monitoring Key Indicators: What to Watch Next

Looking ahead analysts should prioritize observing net interest margin trajectories particularly under different Fed rate scenarios aligned with ALCO position disclosures given prevailing one-year negative repricing gaps.(analysis) Closely monitoring credit quality metrics especially nonperforming loans or charge-off rates concentrated in commercial real estate segments provides early warning signals related to local economic stress.(analysis) Progression on ESG integration initiatives via expanded green lending volumes along with client uptake behavioral patterns may indicate sustainable revenue diversification.(analysis) Tracking capital consumption vis-à-vis dividend escalations plus buyback modest activity will reveal if capital discipline tightens or becomes more aggressive depending on earnings power shifts.(analysis) Maintaining awareness around leadership changes impacting governance or strategic agility remains advisable given evolving competitive landscapes locally.(analysis)

This memorandum summarizes publicly available information without offering investment advice or recommendations regarding First Bancorp securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments