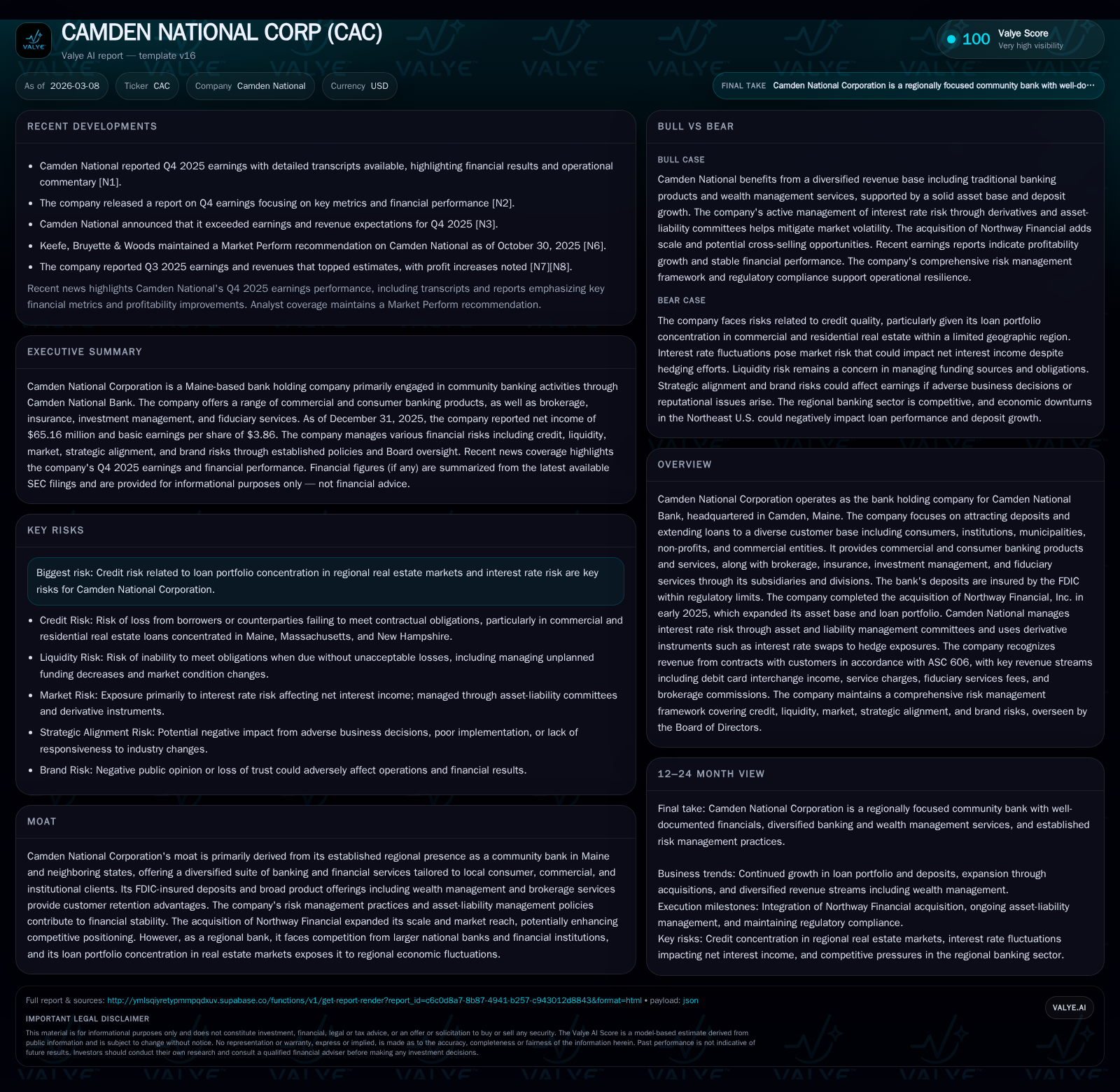

Financial Momentum and Risk Management Shape Camden National’s 2025 Trajectory

Acquisition-fueled growth combined with disciplined risk mitigation underpins Camden National’s strong 2025 performance and future outlook.

Camden National Corporation delivered a substantial net income increase of nearly 23% in fiscal 2025, driven largely by its strategic acquisition of Northway Financial. This deal expanded its loan portfolio and asset base, enhancing scale but also concentrating loan risk in regional real estate markets. The company’s active asset-liability management committee (ALCO) uses derivative instruments to hedge interest rate exposure, supporting net interest margin stability amid fluctuating rates. While credit risk from regional loan concentrations remains a key challenge, Camden National’s prudent capital deployment and solid operational cash flow position it well for sustained growth in its core markets.

Transformative Acquisition Boosts Asset and Loan Base

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 65 | 64 | 6 | +22.9% |

| 2024 | 53 | 61 | 6 | +22.2% |

| 2023 | 43 | 68 | 3 | -29.4% |

| 2022 | 61 | 105 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 21 | 0 | 58 |

| 2024 | 18 | 2 | 55 |

| 2023 | 18 | 2 | 65 |

| 2022 | 18 | 10 | 103 |

Source: SEC companyfacts cache [F1].

Camden National Corporation significantly scaled its balance sheet through the acquisition of Northway Financial Inc. on January 2, 2025 [S1][N1]. The acquired loans had an estimated fair value of approximately $772.6 million at acquisition date, expanding Camden's loan portfolio notably in the Northeast region [S20][S23]. This transaction broadened the geographic footprint into neighboring states beyond Maine while augmenting exposure to commercial and residential real estate sectors predominant in Northway’s portfolio.

While accretive to scale and market reach, this expansion also increased concentration risks related to regional real estate markets — a traditionally cyclical sector subject to local economic shifts [S11]. The acquired assets included both non-Purchase Credit Deteriorated (non-PCD) loans valued at roughly $682 million and PCD loans estimated at about $90.6 million; valuation utilized discounted cash flow techniques sensitive to prepayment speeds and discount rates [S20][S23].

Historical Performance: Robust Earnings Growth with Key Drivers

Despite macroeconomic uncertainties impacting banking broadly, Camden National posted net income of $65.16 million for FY2025 — an impressive 22.9% increase over $53 million earned in FY2024 [F1]. This financial momentum reflected the blend of organic growth augmented by acquisition contributions alongside revenue diversification.

The firm serves a heterogeneous client base encompassing consumers, institutions, municipalities, non-profits, and commercial entities across multiple product lines including traditional lending, brokerage services, wealth management, and fiduciary offerings [S1][N2]. Such diversification undergirds revenue resilience against single-sector downturns.

Operationally, net interest income benefited from expanded loan balances post-acquisition whereas non-interest revenues incorporated fee income from wealth management custodial assets totaling around $1.3 billion as of year-end 2025 [S6]. Overall efficiency ratios showed modest improvements driven by integrated operations after Northway’s assimilation.

Asset-Liability Management: Hedging Interest Rate Risks

Camden National maintains a well-defined asset-liability management framework governed by Board ALCO and Management ALCO committees responsible for oversight on interest rate sensitivity and liquidity exposure [S1][S4]. Utilizing sophisticated dynamic simulation models extending over two-year horizons, these committees evaluate net interest income risks given potential rate shifts.

Instrumental to this strategy is deployment of interest rate swaps designated as cash flow hedges that stabilize interest expense on subordinated debt among other liabilities. Fair values of derivatives stood at meaningful levels with collateral arrangements mitigating counterparty risk [S13][S16]. The Company reported interest expense on subordinated debentures including swap reclassifications at $3.6 million for FY2025 versus $2.1 million prior year reflecting higher rates but effective hedge accounting practices [S13].

Loan Portfolio Concentrations and Credit Risk Considerations

Credit quality remains a paramount focus given loan concentration in Maine-centric commercial real estate plus adjacent Massachusetts and New Hampshire markets [S11]. Camden applies rigorous underwriting standards supported by ongoing borrower creditworthiness assessments coupled with collateral evaluations utilizing appraisals consistent with policy guidelines [S14][S17]

Allowance for credit losses (ACL) frameworks incorporate segmented portfolio analysis including commercial real estate non-owner-occupied loans covering multi-family units to industrial warehouses. Off-balance sheet commitments are similarly scrutinized for expected credit losses using funding probability models anchored in historical data [S4][S22]. Committees such as the Credit Risk Policy Committee oversee systematic monitoring while management periodically adjusts provisioning reflecting economic outlook shifts.

While risk concentrations amplify sensitivity to regional downturns or real estate price corrections, proactive portfolio diversification efforts aid risk dispersion within constrained geographies.

Future Growth Outlook Amidst Regional Market Dynamics

Although explicit long-term guidance is not provided publicly beyond recent earnings calls [N1], management commentary highlights priorities for realizing synergies post-Northway integration including cross-selling wealth management services and expanding commercial loan offerings in adjacent markets [N3][S1]. Competitively confronting national banks relies on leveraging community banking strengths — personalized client relationships and tailored financial solutions — which remain core differentiators.

Analysts should watch deposit growth patterns serving as primary funding sources alongside evolving interest rate environments influencing margin sustainability. Integration cost control will be critical to ensure net accretion rather than dilution.

Capital Deployment Strategy: Dividends, Buybacks, and Equity Changes

Camden National’s capital policies emphasized shareholder returns through dividend enhancements with dividends paid rising to about $21.3 million in FY2025 compared with roughly $18.4 million in FY2024; no share repurchases were undertaken during FY2025 following minimal buyback activity previously [F1][S5].

Equity base expanded materially to approximately $696.6 million at year-end due largely to retained earnings accumulation post-acquisition effects versus $531.2 million prior year end reflecting cautious balance sheet strengthening amid stimulus withdrawal phases [F1].

The resulting approximate return on equity (ROE) stood near a solid 9.4%, corroborating efficient economic use of equity capital despite sector-wide profit margin pressures.

Operational Cash Flow Trends and Investment Activity

Operating cash flows demonstrated steady generation capacity with CFO totaling about $63.9 million in FY2025 representing a slight increase over prior year’s $60.9 million figure (+4.9% YoY) despite greater capital consumption due to business combination integration costs [F1]. Capital expenditure activity stabilized around $5.7 million representing marginal incremental reinvestment reflective mainly of branch technology enhancements rather than expansion capex spikes.

Free cash flow — defined operationally as CFO minus capex — approximated $58.2 million providing robust internal liquidity enabling flexible capital deployment strategies without reliance on outside financing sources currently.

Key Metrics to Monitor in Upcoming Quarters

Key indicators poised for close observation include:

- Quarterly credit quality trends along with allowance coverage levels signaling emerging stress or improvement.

- Deposit balances relative to local competitive pressures around pricing and retention given rising interest rates.

- Effectiveness of hedging instruments assessed via changes in derivative fair value adjustments impacting earnings volatility.

- Progress on integration milestones particularly cost synergy realization relative to acquisition-related goodwill impairment risks.

- Regulatory capital ratio trajectories against Basel III frameworks ensuring compliance amidst capital consumption dynamics stemming from asset growth.

Prudence around these metrics will be essential for assessing whether Camden National sustains its current trajectory or faces headwinds emanating from market or operational factors.

Disclosures herein rely strictly on publicly filed financial statements and verified transcripts up through March 8, 2026 ([F1],[N1],[N3],[S1]-[S29]). This memo does not constitute investment advice but aims to offer a grounded analytical perspective relevant for finance professionals tracking regional banking sector developments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments