A.K.A. Brands Boosts Revenue Despite Continued Losses and Tight Debt Covenants

Modest net sales growth contrasts with persistent net losses and strengthened credit agreement terms in A.K.A. Brands’ 2025 performance.

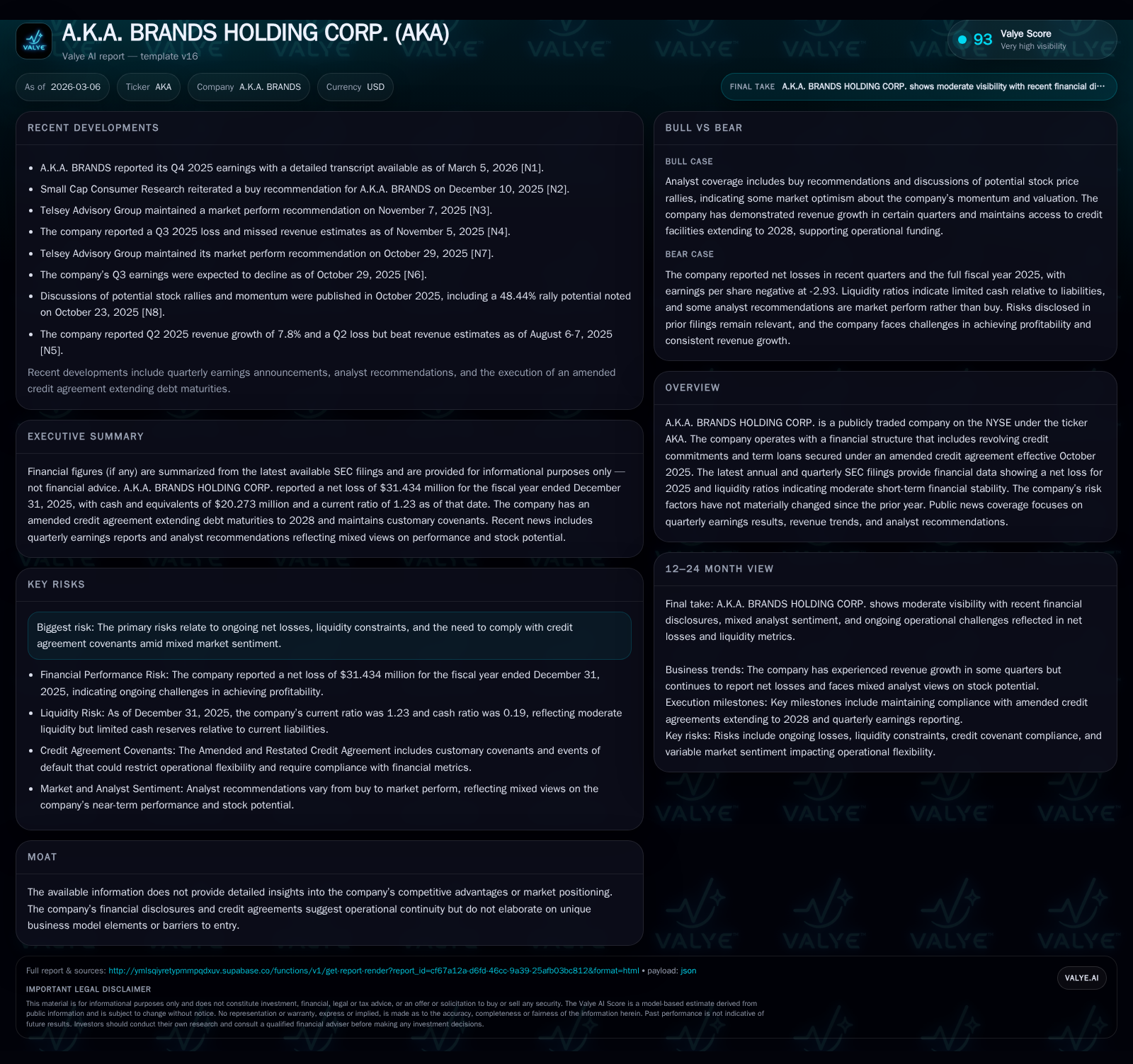

a.k.a. Brands Holding Corp. achieved a 4% increase in net sales for 2025, driven by expanding U.S. sales and a data-driven merchandising strategy targeting next-generation consumers. Despite this growth, operating income declined sharply year-over-year, contributing to a net loss of $31.4 million, though gross margins improved slightly. The company’s amended credit agreement extends debt maturities to 2028 but includes mandatory amortization and restrictive covenants reflecting liquidity and leverage considerations. Capital deployment reflected a cautious approach, with operating cash flow growth offset by rising capital expenditures and modest share repurchases.

2025 Financial Snapshot: Growth Amid Profitability Challenges

a.k.a. Brands Holding Corp. reported fiscal year 2025 net sales of $600.2 million, marking a 4% increase over the $574.7 million recorded in 2024 [S1][N1]. This growth was driven primarily by U.S. operations where revenue rose 7% year-over-year to $394.3 million. Gross margin expanded modestly by approximately 30 basis points despite macroeconomic headwinds.

However, operating income declined from a loss of about $10.3 million in FY2024 to a loss of $18.0 million in FY2025—a nearly 75% decrease year-over-year—reflecting ongoing pressures on profitability even as top-line metrics improved [F1]. Net loss widened to $31.4 million compared to a loss of $25.9 million in the prior year (a -20.9% change) [F1]. This divergence highlights continued investment in brand expansion and associated operating costs.

Liquidity metrics show a current ratio of approximately 1.23 (current assets of $129 million versus current liabilities around $105 million), indicating sufficient near-term coverage but necessitating careful covenant compliance given upcoming amortization obligations [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -31 | 16 | -18 | 17 | -20.9% |

| 2024 | -26 | 1 | -10 | 12 | +73.7% |

| 2023 | -99 | 33 | -83 | 6 | +44.0% |

| 2022 | -177 | 0 | -172 | 20 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 2 | -1 |

| 2024 | 2 | -11 |

| 2023 | 2 | 27 |

| 2022 | -20 |

Source: SEC companyfacts cache [F1].

Data-Driven Retail Model Supports Brand Growth

a.k.a.’s merchandising strategy centers on a "test, repeat & clear" model that refreshes product assortments weekly by analyzing SKU sales velocity and clearing underperforming items swiftly [S1]. This approach is enhanced by omnichannel marketing leveraging social media analytics and influencer partnerships targeting Gen Z and millennial consumers.

Real-time consumer insights enable rapid introduction of exclusive fashion items aligned with evolving trends—a critical factor in the fast-fashion segment where speed-to-market drives competitive advantage.

Brand Portfolio: Engaging Next-Generation Consumers

a.k.a.’s portfolio includes four key brands: Princess Polly and Petal & Pup focusing on women’s fashion; Culture Kings and mnml targeting streetwear enthusiasts [S1][N1]. These brands engage consumers through hybrid retail models combining strong e-commerce presence with expanding physical store footprints.

Princess Polly notably opened its first U.S.-based store in September 2023 and expanded to fourteen stores across key metropolitan areas by the end of 2025 [S1], bolstering direct customer engagement alongside e-commerce leadership.

Credit Facility Amendment: Extended Maturities with Covenant Discipline

In October 2025, the company amended its syndicated credit facility establishing revolving credit commitments totaling approximately $35 million plus term loans aggregating $85 million maturing October 14, 2028 [S4][S7][S8].

The amendment introduced pricing stepdowns linked to annual compliance certificates based on consolidated EBITDA targets near $35 million and mandated quarterly principal repayments starting Q4 2025 at approximately 1.875% of initial loan balances through end-2027 before increasing thereafter [S7]. The indebtedness is secured by first-priority liens on substantially all assets.

Covenants restrict dividend payments, additional indebtedness or liens beyond agreed limits, investments outside approved parameters, and significant asset sales—reflecting lender emphasis on financial discipline amid ongoing losses.

Risks: Economic Sensitivity and Supply Chain Dependencies

Risk disclosures reiterate macroeconomic vulnerabilities including inflationary impacts on discretionary spending patterns [S1][S5]. Dependence on China-based suppliers exposes operations to geopolitical risks amid evolving trade policies between China and the U.S.[S1]

Inventory management complexity is heightened by rapid fashion cycles requiring precise forecasting to avoid excess stock or markdowns [S1]. Additionally, evolving global data privacy regulations may increase compliance costs impacting digital marketing strategies [S6].

Legal matters include settlements related to intellectual property disputes during FY2025 involving payments totaling approximately $16.5 million [S1], representing episodic financial burdens now resolved.

Capital Allocation: Improving Cash Flow Amid Increased Investments

a.k.a.’s operating cash flow surged over twentyfold from roughly $669 thousand in FY2024 to more than $16.4 million in FY2025 due to operational improvements despite persistent net losses [F1]. Capital expenditures increased about 47% to nearly $17.1 million reflecting investments in store openings and e-commerce infrastructure.

Free cash flow was negative at roughly -$633 thousand given higher capital spending relative to internal cash generation.

Share repurchases totaled approximately $2 million during FY2025 as management maintained cautious capital returns aligned with liquidity preservation under restrictive debt covenants [F1][S9].

The approximate return on equity remained negative near -32%, consistent with ongoing losses constraining shareholder returns despite revenue gains [F1].

Outlook: Key Milestones and Monitoring Points

Investors should monitor upcoming quarterly earnings for signs of margin stabilization and sustained revenue growth particularly within the U.S market where the bulk of sales originate [N1][S3].

Compliance with EBITDA-linked covenant requirements will be critical for financing flexibility given mandatory amortization schedules emphasizing working capital efficiency [S4][S7].

Expansion milestones such as further brick-and-mortar store openings beyond the current fourteen locations will indicate progress in scaling omnichannel strategies successfully [S1].

Ongoing vigilance regarding potential litigation or regulatory developments remains warranted given recent settlement experiences impacting liquidity reserves [S1].

This analysis synthesizes information from recent SEC filings and public disclosures without providing investment recommendations or price forecasts. It aims to inform readers about A.K.A Brands Holding Corp’s financial condition and strategic positioning amid current market dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments