Phio Pharmaceuticals Advances Clinical Trial Milestones While Managing Nasdaq Compliance Risks

Phio Pharmaceuticals pushes forward its lead skin cancer asset PH-762 amid persistent operating losses and looming Nasdaq listing challenges.

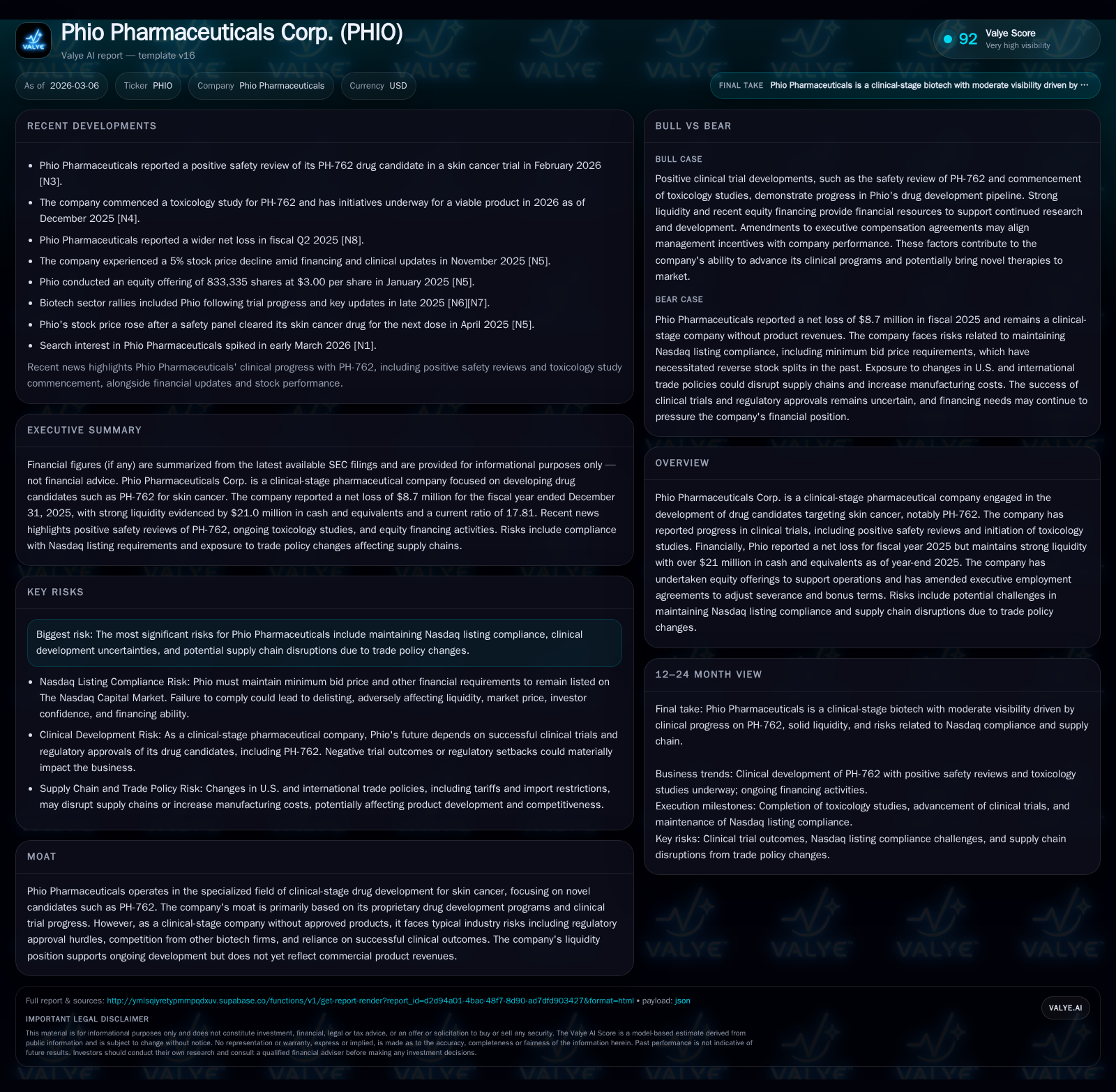

Phio Pharmaceuticals remains a clinical-stage biotech focused on developing PH-762 for skin cancer, recently reporting encouraging safety data and progression into toxicology studies. Despite these clinical advancements, the company’s financials highlight ongoing losses, steady cash burn, and reliance on equity offerings to fund operations. Meanwhile, Phio faces risk from Nasdaq minimum bid price compliance and supply chain uncertainties tied to trade policy shifts. Monitoring clinical milestones alongside capital adequacy and regulatory compliance will be crucial as the company seeks to build value in a competitive oncology space.

Historical Growth: Operating Losses Amid Clinical Development Investment

Phio Pharmaceuticals Corp. continues to operate in the pre-revenue clinical stage biotechnology model. Its financial history underscores persistent investment in R&D without commercial product revenues—the hallmark of early-stage drug developers focused on pipeline advancement before market entry.

Since FY2017, Phio has generated negligible revenue, with reported top-line numbers effectively zero—$0 reported for FY2020 and prior years showing only minimal amounts under $150K that likely represent trial-related reimbursements or grants rather than product sales [F1]. This zero-revenue environment translates into steadily accumulating operating losses. In FY2025 alone, the company incurred an operating income deficit of $9.22 million, worsening year-over-year by about 25% compared to FY2024's loss of $7.39 million [F1]. Net income trends mirror this pattern with a net loss of approximately $8.70 million in FY2025 marking a 21.7% increase in loss magnitude relative to the prior year.

Operating cash flow data reveals a comparable trend — outflows continue with nearly $7.98 million spent on core operations during FY2025 (compared with around $7.11 million in FY2024), highlighting ongoing clinical program outlays [F1]. Capital expenditures remain minimal but increased modestly to $12K in 2025 from only $1K in 2024, reflecting perhaps minor investments in fixed assets or infrastructure.

These financials yield an approximate return on equity of negative 43% for FY2025, indicative of capital consumption consistent with non-revenue R&D-centric firms [F1]. Total equity rose notably from roughly $4.72 million at end-2024 to over $20 million at end-2025, signaling that financing activities—primarily equity raises—have supplied fresh capital to sustain product development efforts.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -9 | -8 | -9 | 12000 | -21.7% |

| 2024 | -7 | -7 | -7 | 1000 | +34.0% |

| 2023 | -11 | -11 | -11 | 5000 | +5.7% |

| 2022 | -11 | -12 | -11 | 121000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -8 | -43.2 |

| 2024 | -7 | -151.4 |

| 2023 | -11 | -140.1 |

| 2022 | -12 | -105.9 |

Source: SEC companyfacts cache [F1].

Table: Phio Pharmaceuticals Historical Financial Summary (FY2018-FY2025)

This financial footprint typifies clinical-stage biotech firms balancing the high-risk profile of novel therapeutic development against capital-intensive R&D spend preceding any potential product commercialization.

Clinical Progress and Pipeline Focus: The Path of PH-762

Phio's strategic emphasis rests squarely on PH-762—a small interfering RNA (siRNA)-based candidate designed for intratumoral treatment of skin cancers such as cutaneous squamous cell carcinoma (cSCC). Recently reported clinical updates have painted a cautiously optimistic picture regarding this lead asset.

In late 2025 and early 2026 communications from the company describe key trial milestones: completion of Phase 1b enrollment (NCT06014086), positive formal safety reviews by the Safety Medical Committee confirming favorable tolerability across doses of PH-762 intratumoral administration [N3][S20], and acceptance of nonclinical toxicology study protocols by the FDA allowing commencement of these pivotal studies in Q1 2026 [S18]. Toxicology studies are standard prerequisites before later-stage trials ensure patient safety at therapeutic doses.

Clinical efficacy signals have also emerged—press releases indicate up to a 70% overall histopathological response rate among cSCC patients treated within the trial cohorts; notably, approximately ten out of fourteen responders achieved complete lesion clearance [N2][S21]. These outcomes lend promise but remain preliminary given the Phase 1b stage focused primarily on safety and dosing rather than definitive efficacy confirmation.

Biotech insiders recognize PH-762 operates within an intensely competitive landscape where immunotherapies and targeted molecular agents vie for FDA approvals addressing skin cancers with varying tumor microenvironment challenges. RNA interference therapies like PH-762 are innovative yet face hurdles including delivery optimization and durability of response.

As such, Phio’s emphasis on robust clinical data readouts backed by regulatory-compliant nonclinical programs reflects an attempt to de-risk PH-762 ahead of critical Phase 2/3 trials necessary to support eventual commercial applications.

Regulatory and Market Risks Including Nasdaq Listing Challenges

Aside from typical biotech regulatory complexities inherent in new drug approval pathways (e.g., FDA scrutiny over study design and data integrity), Phio confronts notable market risks linked to its public listing maintenance on Nasdaq.

The company explicitly flags risk factors associated with meeting Nasdaq’s minimum bid price rule (Rule 5550(a)(2)) requiring a sustained share price above $1 for continued listing [S2][S6]. Past remedial actions included executing reverse stock splits—the most recent occurred July 5, 2024—to regain compliance when trading prices dipped below thresholds.

Noncompliance could trigger delisting proceedings that would likely depress liquidity and share valuation adversely impacting investors’ confidence and restricting access to capital markets vital for ongoing financing needs [S6]. The firm indicates active monitoring and readiness to deploy corrective measures if pricing deficiencies re-emerge.

Additionally, Phio notes exposure to shifts in U.S.-international trade policies as pertinent risks due to foreign supplier dependencies critical for manufacturing clinical compound batches or raw materials [S2][S7]. Potential increased import tariffs or disrupted supply chains tied to geopolitical tensions may heighten production costs or cause delays jeopardizing clinical timelines—a frequent challenge observed across biopharma manufacturers navigating globalized sourcing ecosystems.

This combination of regulatory oversight pressure alongside external macroeconomic vulnerabilities frames a complex operational backdrop for Phio’s advancement trajectory.

Financial Health and Liquidity: Sustaining Operations Through Equity Raises

At December 31, 2025, Phio Pharmaceuticals held $21.03 million in cash and equivalents according to its latest annual report filing [F1], which provides a substantial liquidity cushion relative to current liabilities (~$1.21 million as latest mid-year figure) resulting in an estimated current ratio near 18—indicative of comfortable near-term solvency [F1][S10][S15].

However daunting operating cash flow deficits—$7.98 million outflow recorded for FY2025—highlight continued reliance on financing activities rather than operating-generated funds to support core expenditures related primarily to research programs and clinical trial logistics [F1]. Equity raises conducted during recent quarters underpin this liquidity position including registered direct offerings disclosed through filings dated late 2025 into early 2026 [S10][N1].

Absent commercial revenues circa yet-to-be-approved products like PH-762 necessitates ongoing capital access facilitated largely through equity issuance diluting current ownership but preserving operational continuity while enabling milestone achievement potential.

Capital Allocation Strategy: No Dividends but Managed Cash Burn

Consistent with typical biotech industry norms where reinvestment into drug pipelines dominates budgetary priorities over shareholder returns such as dividends or buybacks, Phio Pharmaceuticals confirms absence of dividend payments or share repurchase programs up through early March 2026 disclosures [S9][S11][S12][S13]. Capital allocation decisively favors preclinical development costs and clinical trial execution expenses.

Further notable is management’s focus on aligning executive compensation with company goals while controlling costs—executive employment contracts were amended recently enhancing severance protections while adjusting bonus target percentages upward moderately without expanding fixed salary commitments significantly [S19]. Such contractual refinements may balance incentivizing leadership retention amid volatile biotech commercial prospects.

Cash preservation remains a key ethos bolstered by disciplined spending judiciously scaled against anticipated funding inflows derived chiefly from equity market transactions.

Future Growth Catalysts and Potential Roadblocks

Forward growth hinges heavily upon forthcoming trial milestones involving PH-762 progression through toxicology assessments toward later-phase efficacy validation trials anticipated post-FDA protocol acceptance dates currently initiated Q1-26 [N2][S18]. Positive interim data reinforcing safety/tolerability alongside emerging efficacy signals will serve as critical value inflection points.

Conversely potential pitfalls include failures to meet efficacy endpoints or unforeseen adverse events disrupting development timelines—risks endemic to all investigational oncology agents—as well as external constraints such as inability to maintain Nasdaq listing thresholds that may impair fundraising capacity which is essential given absence of revenue streams presently.

Competitive landscape intensity elevates pressure; other modalities vying for similar indications may capture attention or resources away from RNAi-focused therapeutics like PH-762 necessitating efficient operational execution by Phio’s management team.

Supply chain robustness amid evolving trade policy environments remains another wildcard factor that could complicate manufacturing cost structures or timing reliability further impacting developmental velocity.

Key Metrics to Monitor and Analyst Expectations

Market participants should closely track several measurable indicators as gauges of progress:

- Timing and outcomes from toxicology study completions following FDA-endorsed protocols expected throughout calendar year 2026;

- Enrollment advances and interim data releases from the Phase 1b/next phase clinical trials assessing PH-762 efficacy specifically within cutaneous squamous cell carcinoma cohorts;

- Share price movements vis-à-vis Nasdaq minimum bid price rules monitoring potential risk triggers requiring corporate action (e.g., reverse stock splits);

- Quarterly liquidity metrics focusing on cash burn rates relative to available capital reserves informing runway sustainability;

- Any announced plans for further equity offerings necessary to cover increased funding needs pending regulatory events ; These factors collectively underpin fundamental assessment frameworks given official guidance remains limited outside routine SEC-disclosed commentary.

Disclaimer: This report is based solely on information available as of March 6, 2026 collected from company filings ([F1],[S#]), regulatory documents ([N#]) without speculative assumptions beyond stated facts. It is intended solely for informational purposes without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments