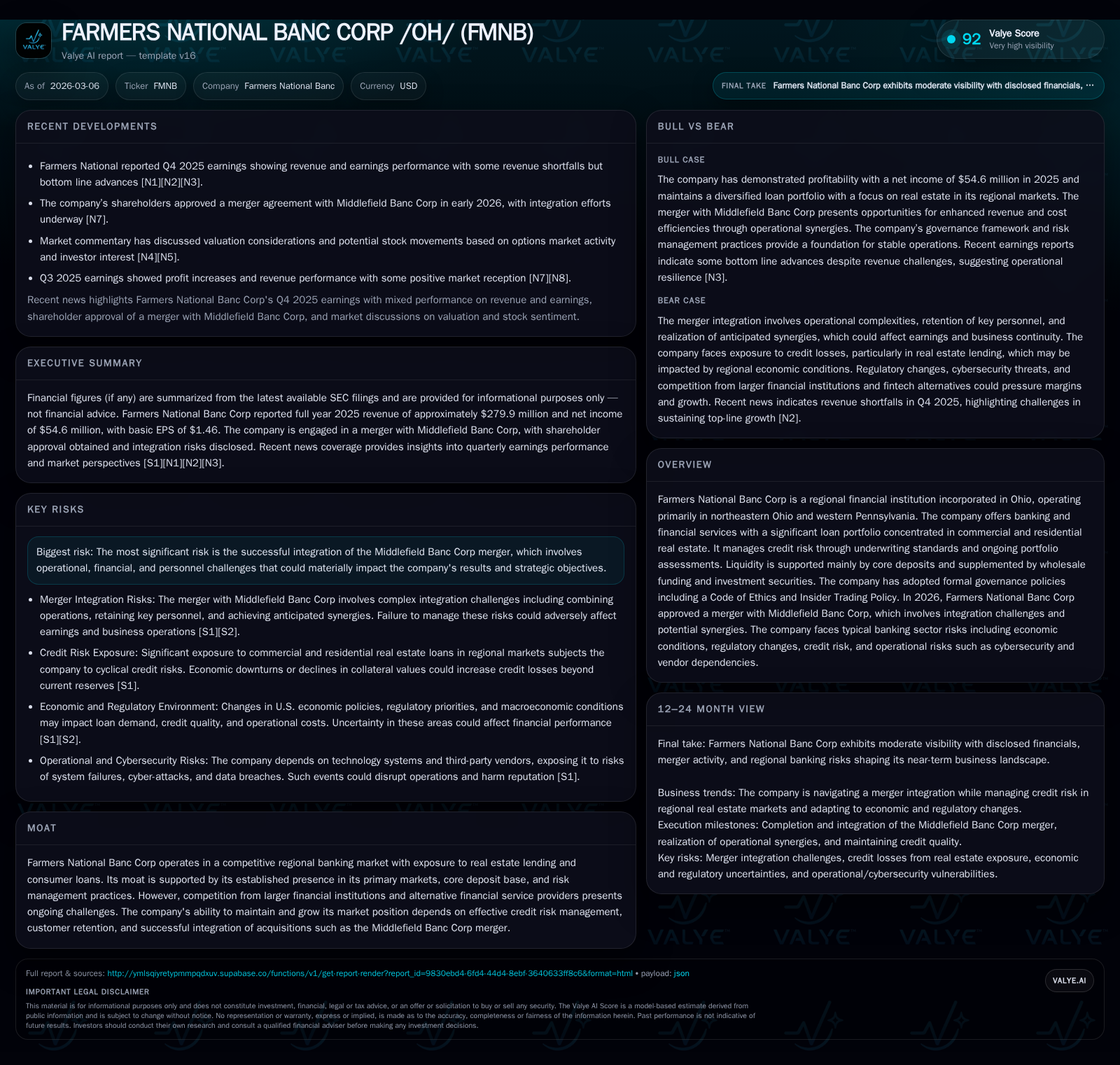

Farmers National Banc Corp's Modest Growth and Merger Integration Challenges Define 2025 Performance

The company posted steady revenue and income gains in 2025 while initiating a complex merger with Middlefield Banc Corp.

Farmers National Banc Corp, a regional Ohio-based financial institution specializing in commercial and residential real estate loans, demonstrated moderate growth in revenue and net income in 2025. Its top-line rose nearly 4% year-over-year, supported by a sizable commercial real estate loan portfolio and prudent risk management. The completion of its merger with Middlefield Banc Corp in early 2026 introduces integration complexities that represent the most significant near-term risk. Strong capital levels and positive free cash flow underpin financial stability, though competitive pressures and regional economic sensitivity remain structural constraints.

Historical Performance Analysis

Farmers National Banc Corp (FMNB), headquartered in Ohio with operations extending into western Pennsylvania, posted steady financial results for fiscal year 2025. Total revenues increased to approximately $280 million from $269.4 million in the prior year, equivalent to a 3.9% increase [F1]. This growth was primarily attributed to its focused lending efforts in commercial and residential real estate sectors—a dominant component of its loan portfolio as disclosed [S11]. Net income improved even more sharply at 18.8%, reaching $54.6 million compared to $45.9 million in 2024 [F1]. This suggests enhanced efficiency or effective cost controls offsetting the deceleration seen in operating cash flows.

Operating cash flows dropped roughly 10% year-over-year to $60 million, reflective of working capital changes or higher loan placements requiring funding absorption [F1]. Capital expenditures fell materially by around one-third from $11.7 million to $7.9 million, potentially signaling a temporary pullback in infrastructure or technology investment [F1]. The company strengthened its equity base significantly to about $486 million from $406 million the prior year—partly due to retained earnings—yielding an implied ROE near 11.2% based on reported net income [F1]. Notably, share buybacks were paused after modest activity in FY2023 [F1], pointing to cautious capital deployment amid expansion initiatives.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 280 | 55 | 60 | 8 | +3.9% | +18.8% |

| 2024 | 269 | 46 | 67 | 12 | -8.0% | |

| 2023 | 50 | 62 | 4 | +273.9% | ||

| 2022 | 13 | 84 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 52 | 11.2 |

| 2024 | 0 | 55 | 11.3 |

| 2023 | 12 | 58 | 12.3 |

| 2022 | 0 | 78 | 4.6 |

Source: SEC companyfacts cache [F1].

Figures in millions USD; Years based on fiscal year-end December.

Business Model and Market Position

FMNB’s business is rooted deeply in regional banking services with a loan portfolio heavily weighted towards commercial real estate (CRE) and residential mortgage loans within northeastern Ohio and western Pennsylvania [S11]. This geographic concentration is a double-edged sword—it fosters a moat via local customer relationships and market knowledge but also exposes the bank to region-specific economic fluctuations.

Credit risk management is essential given the cyclicality of real estate markets; FMNB employs rigorous underwriting standards emphasizing "in-market" loans while avoiding high leverage and concentration risks [S1][S11]. Additionally, the bank holds significant exposure through indirect auto loans acquired from local dealerships, which carry typical risks associated with collateral depreciation and borrower creditworthiness variability [S11].

Liquidity management rests on a solid core deposit base forming about 93% of total deposits at year-end—an advantage for stable funding compared to wholesale borrowings or brokered deposits [S4][S7]. Unpledged investment securities approximated $498 million as of December 31, 2025, providing supplementary liquidity buffers [S4].

Competition is intense from larger banks benefiting from scale advantages as well as nonbank lenders pushing technological innovation; FMNB recognizes the challenge of adapting technologically while maintaining its customer-centric approach [S14][S16]. Governance policies including Codes of Ethics and Insider Trading guidelines further fortify internal controls [S23].

Merger Completion and Integration Risks

A defining development for FMNB was completing the merger with Middlefield Banc Corp on March 2, 2026 [S3][N1]. The strategic rationale centers on expanding market footprint and capturing potential revenue synergies alongside cost savings.

However, integration remains fraught with risks: aligning IT systems, harmonizing corporate cultures, retaining key talent, confronting contractual obligations pre-existing at Middlefield, and managing potentially unforeseen liabilities all demand significant managerial focus [S19][S21]. Distraction or delays could dampen expected benefits or impair customer relationships.

Growth Prospects and Constraints

Growth drivers include:

- Leveraging combined branch networks post-merger for enhanced deposit generation.

- Deepening penetration in commercial real estate lending leveraging regional market expertise.

- Cross-selling financial products among an expanded customer base.

- Selectively entering new markets or product segments aligned with risk appetite.

Conversely, growth may be capped by:

- Credit risk volatility tied to cyclical real estate markets susceptible to macroeconomic pressures such as inflation or recession [S1][S9].

- Elevated noninterest expense stemming from merger-related integration costs.

- Regulatory capital requirements tightening under evolving federal rules possibly mandating additional capital raises [S5].

- Intensified competition from larger institutions or fintechs eroding pricing power.

Financial Returns and Capital Allocation

FMNB’s conservative capital posture is evident; it maintains strong equity levels enabling resilience against credit losses or economic headwinds [F1][S23]. Its ROE around low double digits reflects balanced profitability appropriate for a mid-sized regional bank engaged primarily in traditional lending.[F1]

Capital allocation has been cautious: no buybacks were executed in FY2024 or FY2025 after modest repurchases three years prior [F1], indicative of prioritizing capital retention possibly related to acquisition expenses or upcoming investment needs.

Operating cash flow trends suggest ample free cash generation even after capex deductions — estimated free cash flow stood above $52 million for FY2025 — giving flexibility for debt servicing, dividends, or strategic investments.[F1]

Dividend payments remain dependent on regulatory approval tied closely to subsidiary earnings distributions; any restriction here could impact share-level payouts [S5][S21].

Key Risks Summary

Primary risks confronted include:

- Merger execution risk: failure to realize targeted synergies or disruption during integration could materially harm results.

- Concentrated credit risk: heavy reliance on CRE exposes FMNB to cyclicality beyond management’s control.

- Regional economic dependence: downturns in northeastern Ohio and western Pennsylvania impact borrower repayment capacity.[S1]

- Regulatory uncertainties: shifting supervisory priorities may increase compliance costs or constrain growth strategies.[S15]

- Technological adaptation challenges: failure to implement new digital banking platforms effectively risks customer attrition.[S16]

- Cybersecurity exposure given dependence on both internal systems and third-party vendors.[S21]

Outlook Considerations (Analysis)

While explicit forward guidance was not provided publicly as of filing dates,[N1][N2] investor focus should center on tracking integration milestones following the March merger completion. These include system consolidation timelines, retention rates of key employees across organizations, realization of anticipated cost savings versus incremental expenses, and stability of core deposit retention amidst operational changes.

Monitoring loan portfolio performance metrics will be critical too—particularly assessing trends within CRE segments amid changing interest rates that influence refinancing activity and borrower solvency.[S1][S9][S17]

Capital adequacy levels remain a watch item due to ongoing federal proposals altering minimum requirements; transparent disclosures around these developments will be instructive.[S5]

Externally driven economic variables—such as Federal Reserve monetary policy shifts impacting interest rate spreads—and competitive innovations affecting deposit gathering will continue shaping operational results moving forward.[S14][S16]

DISCLAIMER: This report is prepared solely for informational purposes based on publicly available data up to March 2026. It does not constitute investment advice nor an offer or solicitation for purchase or sale of securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments