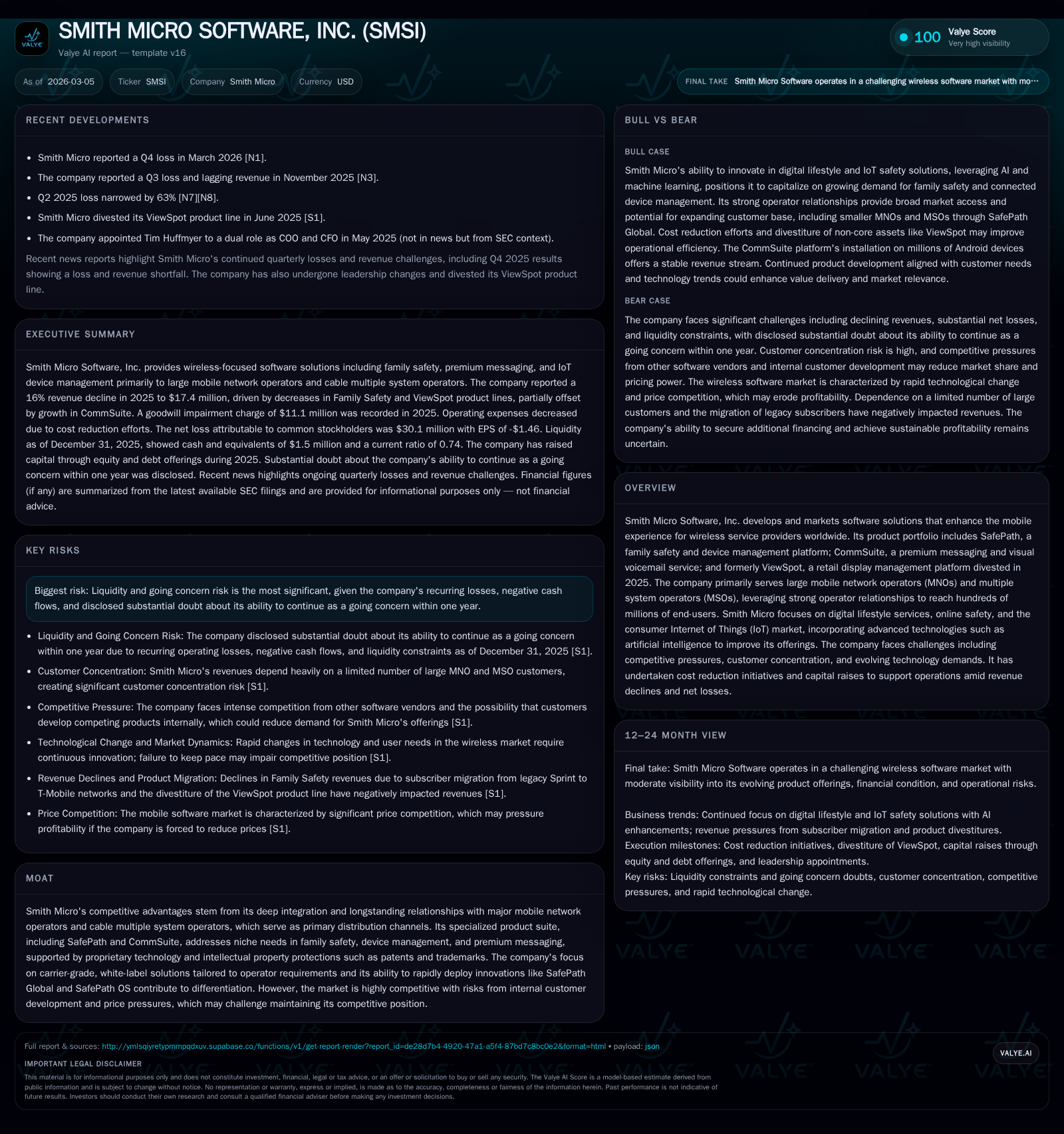

Smith Micro Software Faces Revenue Decline and Liquidity Constraints Amid Cost Reduction Initiatives

Smith Micro Software, Inc. continues to navigate a challenging financial environment with declining revenues and negative cash flows despite strategic efforts targeting cost efficiency and product innovation in digital lifestyle and IoT markets.

In 2025, Smith Micro Software, Inc. (SMSI) reported a revenue decline of 16% to $17.4 million driven by subscriber migration impacts and the divestiture of its ViewSpot product. The company sustained a net loss of approximately $29.3 million with operating cash outflows of $7.2 million, highlighting ongoing liquidity pressures. Management has implemented workforce reorganizations aimed at annualized cost savings exceeding $7 million to realign expenses with business objectives. Smith Micro’s operational focus remains on advancing its SafePath family safety platform and CommSuite messaging services through deep operator partnerships, although substantial doubt about the company's ability to continue as a going concern persists due to recurring losses and customer concentration risks [F1][S1][S6][S7][S26].

Company Overview

Smith Micro Software, Inc. provides software solutions that enhance mobile experiences for leading wireless service providers worldwide. Its portfolio includes digital lifestyle services like SafePath™, a family safety platform offering location tracking, parental controls, and AI-driven social media insights, as well as CommSuite®, a premium visual voicemail platform serving millions of Android users primarily in the U.S. wireless market [S4][S5][S25].

The company maintains strong relationships with major Mobile Network Operators (MNOs) and Multiple System Operators (MSOs), which serve as primary distribution channels granting access to vast end-user bases globally [S4][S16]. This customer concentration presents both an advantage in reach and a risk due to dependence on limited large customers.

Smith Micro operates within a rapidly evolving wireless industry marked by growing adoption of consumer Internet of Things (IoT) devices such as smartwatches, fitness trackers, pet trackers, GPS locators, and smart home devices that expand connected lifestyles but introduce complexity in device management and security requirements [S19].

Historical Financial Performance

The company has experienced persistent revenue declines over recent years during changing market dynamics and product portfolio adjustments such as the divestiture of ViewSpot in June 2025 [S1][S23]. Revenue for the full year 2025 was reported at $17.4 million, down approximately 16% from $20.6 million in 2024 due primarily to subscriber migration reducing Family Safety revenues by about $2.3 million and declining ViewSpot revenues by roughly $1 million following contract completion and sale [S1][S14]. CommSuite revenues increased marginally but were insufficient to offset these declines.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -29 | -7 | -29 | +39.8% |

| 2024 | -49 | -14 | -49 | -99.6% |

| 2023 | -24 | -7 | -18 | +16.7% |

| 2022 | -29 | -19 | -31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -159.5 |

| 2024 | -119.5 |

| 2023 | -32.4 |

| 2022 | -38.3 |

Source: SEC companyfacts cache [F1].

Gross profit margin improved from approximately 70% in 2024 to over 74% in 2025 due to cost control efforts despite reduced revenue volume [S14]. Operating expenses fell by nearly $22 million year-over-year reflecting smaller goodwill impairment charges ($11.1 million versus $24 million in prior year), workforce reductions, and decreased marketing spend [S1][S12].

Product Portfolio & Market Positioning

Smith Micro’s flagship SafePath platform integrates family safety features enhanced by AI/machine learning capabilities addressing parental concerns regarding online safety for children through social media monitoring insights [S25]. The launch of SafePathOS enables carriers to pre-install family safety features on devices targeted at children and seniors, facilitating faster deployment within operator ecosystems.

CommSuite offers next-generation visual voicemail services including voice-to-text transcription available on millions of Android handsets across prepaid and postpaid U.S. markets [S25]. The divestiture of ViewSpot reflects a strategic exit from retail display management following contract completion amid declining revenues.

Competition is intense from other software vendors as well as MNOs developing proprietary solutions internally which may displace third-party products like those offered by Smith Micro [S8]. Price competition is significant; any erosion could negatively affect margins given the company’s focused product set.

Additionally, over-the-top (OTT) messaging platforms increasingly challenge carrier-controlled messaging monetization models that underpin CommSuite’s value proposition [S19][S8]. Intellectual property protections are maintained via patents, trademarks, copyrights, confidentiality agreements but enforcement challenges persist [S8][S16].

Liquidity & Capital Structure

At December 31, 2025 Smith Micro held approximately $1.5 million in cash equivalents against current liabilities exceeding $6 million resulting in a current ratio near 0.74 indicative of working capital constraints [F1][S6]. Shareholders’ equity declined substantially to about $18.4 million from over $40 million the prior year due to accumulated losses [F1]. Operating cash flows improved but remained negative at roughly -$7.2 million for the full year [F1][S11].

Capital raising activities during fiscal year 2025 included registered direct stock offerings and issuance of short-term notes generating gross proceeds aggregating several millions supporting liquidity needs [S6][S11]. Despite these efforts, management acknowledges substantial doubt about Smith Micro's ability to continue as a going concern within one year stemming from recurring losses, negative cash flows, limited cash reserves relative to liabilities, and reliance on subscriber growth or additional financing [S6][S13][S27].

To address liquidity pressures management has initiated workforce reorganizations announced October 2025 expected to yield approximately $7.2 million in annualized cost savings alongside ongoing cost reduction measures [N1][S26]. Potential additional actions include further restructuring, securing credit facilities if available, asset disposals beyond ViewSpot sale or licensing intellectual property rights [S7][S13].

Growth Outlook & Strategic Priorities

Innovation efforts focus on expanding digital lifestyle services addressing family safety through AI-enhanced capabilities within SafePath products aiming for broader carrier adoption including smaller MNOs/MSOs via simplified deployment platforms such as SafePath Global™ designed for rapid integration [S4][S25].

Management targets increasing the customer base beyond existing large operators while deepening integration within current customers’ service ecosystems to drive upsell opportunities anchored on SafePath Kids™ embedded directly into core device offerings rather than add-ons [N1][S25]. Leveraging AI for behavioral insights is central to differentiation strategies amid commoditization risks.

However growth prospects face headwinds including:

- Potential displacement by internal carrier-developed software reducing third-party reliance;

- Pricing pressure compressing already thin margins;

- OTT messaging platforms eroding traditional carrier messaging revenues;

- Concentration risk arising from dependence on a limited number of large global MNO/MSO partners;

- Increasing cybersecurity demands requiring ongoing investments despite no material incidents reported recently [S22].

Key milestones include subscriber adoption rates following new product launches (e.g., SafePath OS devices), renewal or expansion agreements with key MNO customers, execution success on cost containment initiatives, capital raising outcomes, and market acceptance of AI-driven family safety features.

Returns Profile & Capital Allocation

Financial returns remain under pressure; approximate return on equity is deeply negative given net losses near $29 million relative to equity around $18 million illustrating ongoing erosion without recovery signs at scale currently achieved [F1]. No dividends were declared amid sustained losses.

Historical share repurchases are not evident in recent years aligning with financial constraints documented since late-stage fiscal years.[F1]

Free cash flow remains negative due primarily to operating losses outpacing modest capital expenditures focused on software development rather than fixed asset investments.[F1][S12]

Goodwill impairment charges totaling $11.1 million in FY25 following prior year’s $24 million reflect asset value reassessments aligned with performance outlooks underscoring continued pressure on investment returns metrics.[F1][S23]

Risk Factors Summary

Significant risks include liquidity constraints raising going concern doubts absent sufficient subscriber growth or financing; intense competition including potential substitution by carrier-developed alternatives; pricing pressures compressing margins; concentrated customer base increasing volatility; technology evolution requiring continuous investment; plus operational execution risk related to cost restructuring effectiveness.[S18][S29] Cybersecurity risk is monitored actively without material incidents reported but remains an area requiring vigilance.[S22]

Conclusion

Smith Micro Software stands at a pivotal crossroads balancing innovative family safety and messaging software embedded within operator ecosystems against structural financial challenges characterized by shrinking revenues post-divestiture impact alongside sizeable recurring losses impacting liquidity. The company’s strategy emphasizes leveraging proprietary AI-enhanced platforms deployed through established operator channels while aggressively trimming costs targeting profitability pathways. Nevertheless material risks tied to evolving market dynamics like OTT disruption combined with financial fragility require careful monitoring where operational execution success alongside timely capital access will determine longer-term viability.

Disclosure: This analysis is based exclusively on publicly available information sourced from SEC filings dated through March 2026 and verified news reports cited herein; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments