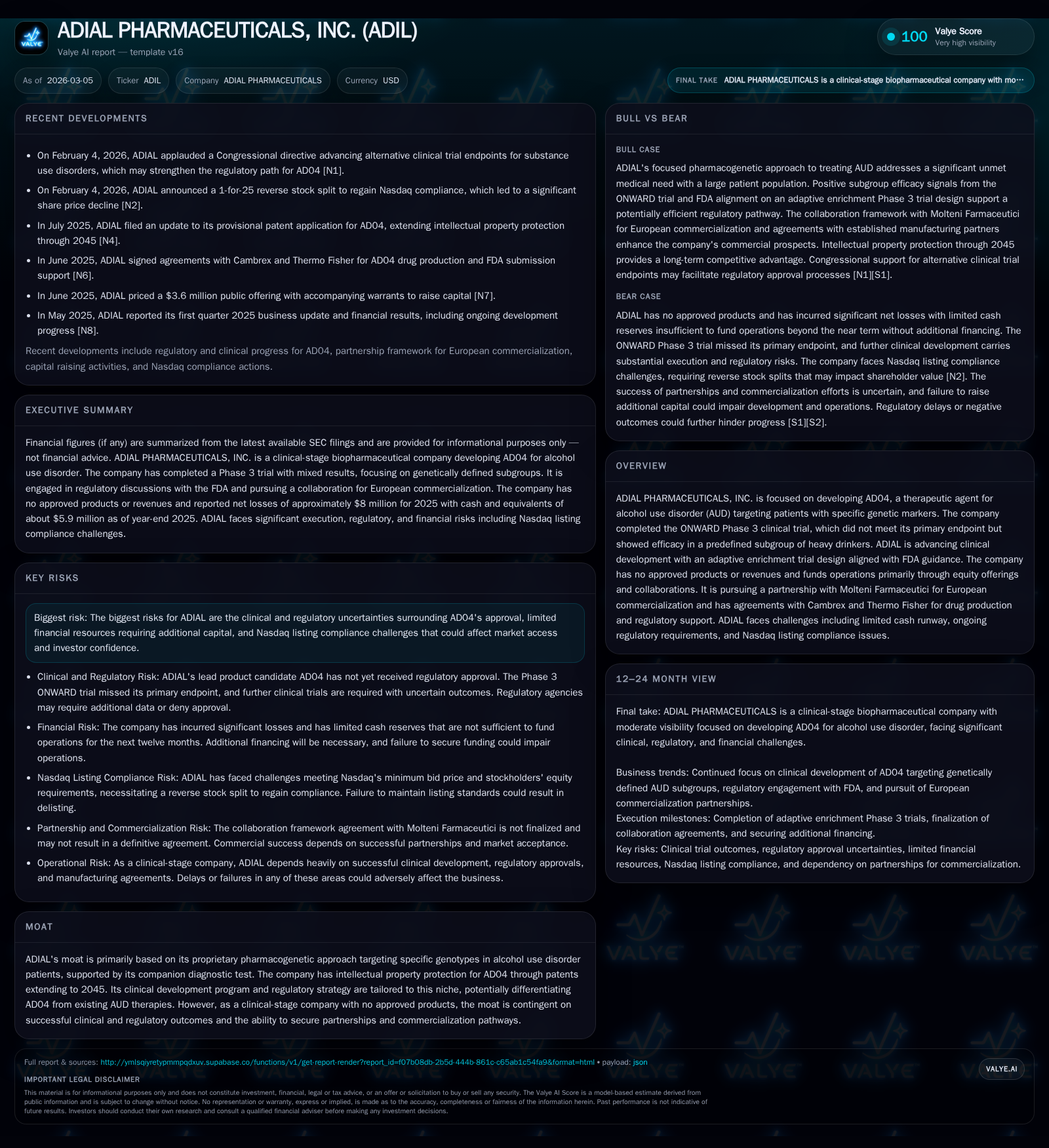

Adial Pharmaceuticals' Genetic-Targeted AUD Therapy Advances Amid Funding and Regulatory Pressures

Clinical-stage biotech Adial advances AD04 for alcohol use disorder focusing on genetic subpopulations with limited cash runway and Nasdaq challenges.

Adial Pharmaceuticals, Inc. remains a clinical-stage company focused on developing AD04, a pharmacogenetically targeted therapy for alcohol use disorder (AUD). Despite the ONWARD Phase 3 trial missing its primary endpoint, efficacy observed in a genetic subgroup has guided a refined FDA-aligned development strategy. The company operates without revenues, incurring consistent net losses and burning cash amid escalating R&D costs. Strategic partnership talks for European commercialization are underway, yet financial sustainability is strained by limited capital resources and the need for Nasdaq listing compliance remediation.

Company Overview

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -8 | -6 | -8 | +39.6% |

| 2024 | -13 | -7 | -8 | -157.6% |

| 2023 | -5 | -7 | -7 | +59.8% |

| 2022 | -13 | -11 | -13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | -151.2 | |

| 2024 | 1661 | -324.4 |

| 2023 | 1661 | -125.5 |

| 2022 | -388.6 |

Source: SEC companyfacts cache [F1].

Adial Pharmaceuticals operates as a clinical-stage biopharmaceutical developer concentrating on AD04, a novel therapeutic agent targeting alcohol use disorder (AUD) patients possessing specific genetic markers. Its patent-protected pharmacogenetic approach aims to treat subpopulations identified through its proprietary companion diagnostic test. Since inception, Adial has not commercialized any product and therefore has generated no revenue, relying heavily on public equity raises and partnerships to fund operations.

Historical Performance and Key Financials

The company's development journey reflects the inherent risk associated with early-stage biopharma investments focused on niche genetic-driven indications. Across four years up to FY2025, Adial consistently recorded net losses driven by research and development expenditures coupled with general administrative costs associated with clinical operations dedicated mainly to AD04.

| FY | OpInc | NetIncome | CFO | Capex | Equity |

|---|---|---|---|---|---|

| 2025 | -7,799,462 | -7,977,171 | -6,492,603 | 5,276,458 | |

| 2024 | -8,284,457 | -13,197,451 | -6,922,306 | 4,068,084 | |

| 2023 | -6,887,947 | -5,123,341 | -6,806,809 | 4,083,529 | |

| 2022 | -13,317,127 | -12,731,416 | -11,185,985 | 65,000 | 3,276,494 |

Operating income improved marginally by ~6% in FY2025 compared to FY2024 despite ongoing losses; net loss also narrowed significantly by nearly 40% reflecting possible operational adjustments or cost reductions [F1].

Operating cash flow (CFO) remains substantially negative over these years showing continuous cash burn to support clinical programs without offsetting revenues. Capital expenditure is minimal reflective of the biotech model's focus on R&D infrastructure mainly contracted out to external partners.

Clinical Development Progress and Regulatory Landscape

AD04's lead program was the ONWARD Phase 3 trial which unfortunately did not meet its primary endpoint across the overall study population. However the trial identified efficacy signals within a predefined genetic subgroup characterized by heavy drinkers possessing specific genotypes. This pivot prompted Adial to pursue an adaptive enrichment clinical strategy targeting this responder population aligning closely with emerging FDA regulatory guidance tailored towards pharmacogenetic therapeutics.

Regulatory dynamics appear optimistic following a Congressional directive encouraging the advancement of alternative endpoints for treatment trials in substance use disorders potentially easing pathways for drug approval focused on genetically stratified populations [N2].

That said, approval hurdles remain substantial given the novelty of pharmacogenetic approaches in AUD treatment combined with stringent requirements for companion diagnostics. Post-approval commercial viability also hinges heavily on third-party reimbursement decisions amid evolving US healthcare pricing reforms affected by legislation such as the Inflation Reduction Act influencing drug pricing pressures broadly [S8][S12].

Partnerships and Commercialization Strategies

To tackle geographic expansion challenges beyond the US market — where regulatory hurdles are often complex and reimbursement systems vary significantly — Adial has entered into a collaboration framework agreement with Molteni Farmaceutici intended to secure exclusive rights for European commercialization of AD04 upon approval. Such partnerships are critical given Adial’s lack of commercial infrastructure.

Additionally, contract manufacturing arrangements are established with Cambrex Corporation and regulatory/compliance support services through Thermo Fisher Scientific indicating efforts to de-risk supply chain components essential for future commercialization readiness [S3].

Capital Allocation and Financial Health

Adial’s balance sheet as of December 31, 2025 shows cash & equivalents around $5.9 million against current liabilities estimated near $1.4 million yielding a healthy current ratio above four — suggesting short-term liquidity coverage albeit from a small absolute base [F1]. Notably though current funds are forecasted only sufficient to carry operations into mid-2026 absent new financing given ongoing high burn rates primarily related to clinical research activities [S2].

The company’s roughly $90 million accumulated deficit alongside repeated annual losses portrays typical early-stage biotechnology risk profiles where positive earnings generation remains several years off contingent on successful product approval and commercialization trajectories.

Approximately negative return on equity around -151% reflects sustained losses relative to shareholder capital invested so far [F1], illustrative of high-risk venture development stage.

Capital allocation to date primarily focuses on research and administrative expenses without significant capital expenditures. Share repurchases historically have been negligible indicating absence of buyback policies during this expenditure-intensive phase.

Business Risks and Challenges

Adial faces multifaceted risks:

- Clinical trial uncertainties persist around conclusively demonstrating efficacy/safety required for FDA/EMA approvals.

- Regulatory frameworks around genetic-targeted therapies remain evolving adding compliance complexity.

- Financial constraints represent immediate pressure threatening operational continuity without successful financing or partnering.

- Nasdaq listing compliance issues led to a one-for-25 reverse stock split in early 2026 intended to regain adequacy but resulted in share price volatility impacting investor sentiment [N1].

- Intellectual property litigation risk exists given licensed patents expiring in early-mid next decade though new patents extend exclusivity potentially til mid-century; risks from potential infringement claims or challenging patent validity cannot be discounted .

- Healthcare reform legislation impacting drug pricing/reimbursement create uncertain market access environments affecting future revenue projections [S8][S12].

- Data privacy regulations especially GDPR impose strict controls relevant given companion diagnostic data processing [S5][S11].

Forward Outlook: What To Watch

Although explicit revenue or approval milestones remain unavailable due to inconclusive late-stage data pending ongoing trials designed under adaptive enrichment methodologies [N2], key value drivers include:

- Completion and successful readout of adaptive enrichment trials confirming efficacy in targeted genotypic populations per FDA guidance.

- Finalizing definitive partnership agreements in Europe enabling groundwork for multiregional commercialization tackling regulatory reimbursement hurdles outside US.

- Raising meaningful additional capital or strategic alliances securing operational runway beyond mid-2026 critical given current cash constraints.

- Monitoring changes in healthcare policies affecting drug pricing frameworks especially within Medicare/Medicaid dynamics impacting expected reimbursement levels.

- Surveillance of Nasdaq listed status maintaining compliance post-reverse split mitigating delisting risks detrimental to liquidity/access.

Concluding Perspective

Adial Pharmaceuticals exemplifies high-risk/high-reward clinical-stage biotech paradigm focused on precision medicine approaches within addiction therapeutics—a notoriously difficult indication domain historically underserved by effective medications. The proprietary targeting of AUD patients via companion genetic testing constitutes its differentiated moat supported by robust patent protection extending well into coming decades.

Nonetheless the firm faces profound execution risks: no product approval or revenue streams exist; future funding needs are urgent; regulatory pathways remain demanding; and commercial viability hinges upon complex reimbursement landscapes within US and EU markets. While strategic collaborations signal validation efforts externally — notably Molteni Farmaceutici partnership prospect for Europe — near-term survival depends heavily on financial resourcefulness amidst ongoing development expenses causing persistent operating losses.

Without concrete indications yet on expanded regulatory acceptances or commercial rollout timelines beyond speculation contained within governmental policy shifts advancing drug evaluation standards for substance use disorders (as highlighted recently), stakeholders must anticipate continued volatility common within biopharmaceutical innovation cycles before realizing transformative outcomes if success ensues.

DISCLAIMER: This analysis is informational only based strictly on disclosed public filings and news sources up to March 2026. It does not constitute investment advice or recommendation. Investors should conduct their own due diligence considering risks inherent in clinical-stage biotechnology ventures before any decision-making.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments