BridgeBio Oncology Therapeutics Confronts Clinical Execution and Capital Intensity Amid Early-Stage Pipeline Development

BridgeBio Oncology Therapeutics focuses on novel KRAS and PI3Kα inhibitors but faces substantial operational and financial hurdles as it advances clinical programs.

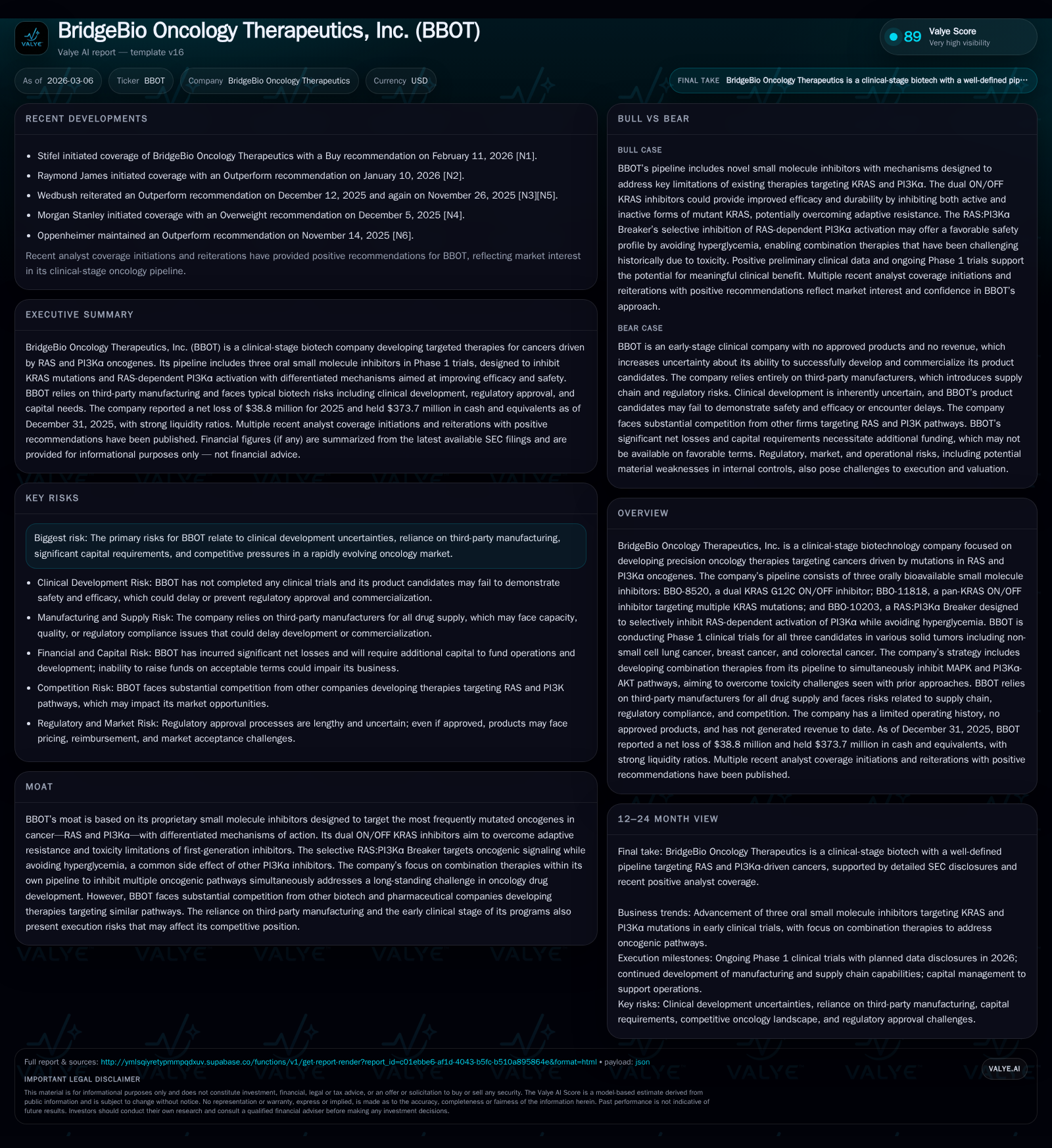

BridgeBio Oncology Therapeutics, Inc. (BBOT) is a clinical-stage biotech dedicated to developing small molecule precision oncology therapies targeting RAS and PI3Kα mutations, with three candidates in Phase 1 trials. The company's historic financials reveal dramatic widening losses and negative cash flow driven by intensified clinical development activities without any revenue generation. BBOT's future growth hinges on successful clinical milestones for its dual ON/OFF KRAS inhibitors and selective RAS:PI3Kα Breaker, while risks include reliance on third-party manufacturing, heavy capital needs, competitive pressures, and regulatory uncertainties. Investors should monitor upcoming trial data readouts and cash runway indications given the pronounced cash burn and absence of revenue.

Company Overview

BridgeBio Oncology Therapeutics (BBOT) is a clinical-stage biopharmaceutical entity concentrating on precision therapies against cancers harboring aberrations in RAS and PI3Kα genes. Its innovative portfolio comprises three orally available small molecules: BBO-8520 (dual KRAS G12C ON/OFF inhibitor), BBO-11818 (pan-KRAS ON/OFF inhibitor covering multiple mutations), and BBO-10203 (a RAS:PI3Kα Breaker engineered to inhibit oncogenic PI3Kα activation selectively while sparing normal glucose metabolism). These assets are engaged in Phase 1 studies targeting tumors such as non-small cell lung cancer (NSCLC), breast cancer, and colorectal cancer .

Historical Financial Performance

BBOT has neither commercialized any products nor recorded revenues historically due to its early developmental stage [S1][F1]. Its operating model thus centers on research commitments primarily financed through equity issuances and financing activities.

The last two fiscal years emphasize significant swings attributable to accelerated pipeline progression:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -134 | -114 | -146 | -1863.9% |

| 2024 | 8 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -32.6 |

| 2024 | -203.6 |

Source: SEC companyfacts cache [F1].

These figures highlight an extraordinary increase in operating losses (24,852% worsening Year-over-Year), net losses (1864%), and operating cash outflows (~14,811%). Such jumps delineate intensifying expenditures linked to clinical trial escalations and infrastructure scaling during lead asset advancement phases [F1]. The equity position turned strongly positive by the end of 2025 versus negative prior year.

Future Growth Prospects

BBOT’s trajectory depends critically upon demonstrating favorable safety and efficacy profiles for its Phase 1 candidates. Its strategy goes beyond monotherapies by pursuing synergistic combination regimens that concurrently inhibit MAPK alongside the PI3Kα-AKT axis aiming to manage adaptive resistance challenges seen in earlier inhibitors .

Growth drivers rest on:

- Successful transition beyond Phase 1 establishing proof-of-concept signals.

- Efficient scale-up of GMP-compliant drug manufacturing despite reliance on third parties.

- Securing intellectual property scope broad enough to defend exclusivity.

- Favorable regulatory interactions facilitating expedited review pathways given the unmet need in RAS-driven malignancies.

Conversely, growth caps emerge from:

- Delays or failures in clinical development due to toxicity or insufficient efficacy.

- Escalating competition targeting overlapping molecular mechanisms affecting market positioning.

- High capital consumption necessitating frequent funding rounds possibly diluting shareholder value.

- Regulatory uncertainties across geographies with variable pricing controls impacting commercial economics.

Forecasts / Milestones / Expectations

Explicit company guidance is not articulated publicly; however, attention should focus on interim clinical readouts from ongoing Phase 1 trials which serve as critical inflection points. Also essential will be announcements related to:

- Dose escalation completions validating tolerability profiles.

- Biomarker-driven patient subgroup analyses predicting target engagement.

- Progression into Phase 2 efficacy trials following initial safety demonstrations.

Monitoring BBOT's cash reserves relative to burn rate will indicate operational runway sufficiency ahead of potential financing endeavors .

Returns & Capital Allocation

Due to its developmental stage status devoid of commercial revenues or profits BBOT shows consistently negative returns metrics; specifically FY2025 ROE approximates -32.6% highlighting unprofitable leverage of equity capital thus far [F1].

Capital deployment has prioritized research expenditure manifested through elevated operating losses coupled with negative operating cash flows around -$114 million annually [F1]. There have been no dividend distributions or share repurchases as resources have been funnelled towards advancing investigational compounds through costly early-stage trials [S1][F1].

Industry Context & Competitive Moat Analysis

In oncology pharmaceutical research circles, KRAS mutations have traditionally been considered 'undruggable'. The advent of direct covalent inhibitors like those targeting the G12C variant marked a paradigm shift. However, limitations including resistance emergence mandate next-generation agents with broader selectivity or combinatorial mechanisms such as those BBOT pursues .

PI3Kα inhibition is similarly complicated by unwanted metabolic side effects like hyperglycemia due to off-target impacts. Thus the selective inhibition profile engineered into BBOT’s BBO-10203 attempts a differentiated approach reducing toxicity burden—a crucial differentiator amidst crowded competitors also advancing PI3K pathway modulators internally or via partnerships .

BBOT's approach emphasizes internal combination regimens aiming for simultaneous blockade within RAS-dependent signaling cascades—an innovation seeking enhanced efficacy balanced against tolerability constraints that plagued predecessors.

Beyond technical moat factors exist operational challenges including sole-source supplier dependencies exposing program timelines to disruption risks—an issue not uncommon among emergent biotechs relying on CMOs adapting novel molecules.[S22]

Additionally noteworthy are evolving global healthcare compliance obligations encompassing data privacy regimes like GDPR/CCPA (to which BBOT is subject given its clinical trials involving personal health data), anti-bribery statutes governing physician interactions especially salient in EU member states with strict disclosure requirements for payments, as well as fluctuating pharmaceutical pricing negotiations influenced by government payors worldwide potentially compressing future product margins.[S5][S8]

Risk Factors Summary

Key risks flagged extensively throughout SEC filings include:

- Clinical trial failure or regulatory approval delays thwarting timely product availability.[S1]

- Manufacturing complications at third-party facilities causing supply bottlenecks.[S22]

- Capital raising dependence with possible unfavorable dilution terms.[S1]

- Potential intellectual property disputes obstructing freedom-to-operate.[S6][S12][S16]

- Compliance lapses generating fines or reputational harm under health fraud/abuse laws.[S9][S17]

- Market competition from better-funded incumbents or more advanced pipelines targeting overlapping mutational niches.

Conclusion

BridgeBio Oncology Therapeutics embodies the archetypal clinical-stage biotech grappling with intense scientific complexity inherent in targeting stubborn oncogenic drivers while scaling financially precise development efforts under operational constraints. Its distinctive chemistry directed at adaptive drug resistance and toxicity mitigation could carve an important niche if ongoing Phase 1 evaluations validate hypotheses regarding tolerability and combinatorial benefits. However, the absence of revenue amidst steep losses underscores acute need to monitor clinical progress milestones alongside capital runway metrics closely. Market positioning within a crowded oncology landscape demands not only scientific merit but adept navigation of regulatory pathways and global reimbursement climates tethered tightly to safety-efficacy value propositions.

Given these factors, stakeholders tracking BridgeBio Oncology Therapeutics should prioritize forthcoming trial data releases for developments portending de-risking scenarios while maintaining awareness of liquidity trends due to persistent heavy R&D outflows absent external commercial cash inflows.

This analysis relies solely on publicly filed SEC documents up to March 6, 2026 ([F1],[S#]) plus cited news ([N#]). It neither constitutes investment advice nor forecasts future stock performance but aims solely at summarizing company fundamentals alongside industry context grounded in disclosed facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments