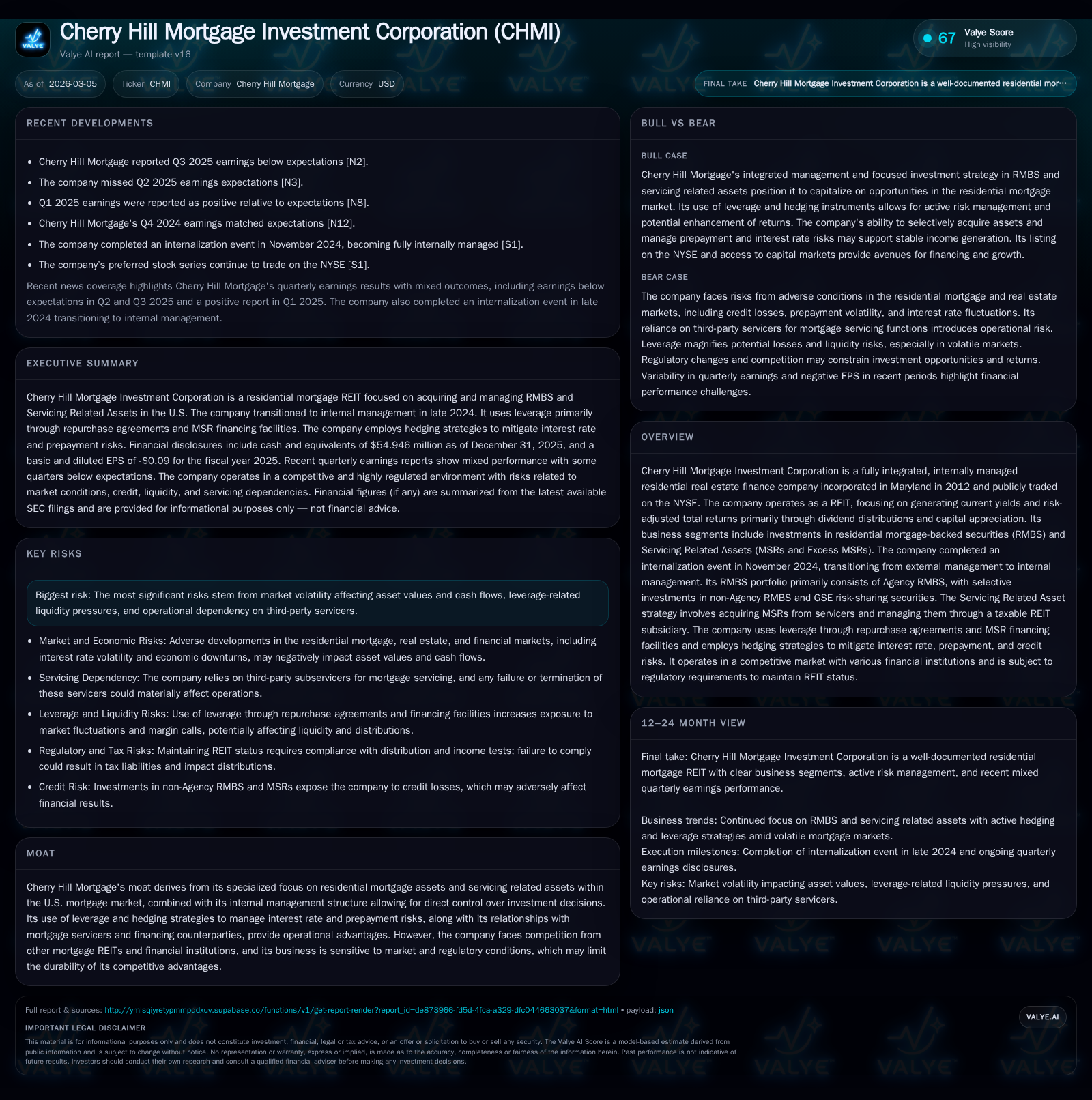

Cherry Hill Mortgage Investment Corp's Internalization and Leverage Strategy Shape 2025 Performance

Transition to internal management and leverage usage drive portfolio strategy amid challenging mortgage market conditions.

Cherry Hill Mortgage Investment Corporation, operating as a REIT specializing in residential mortgage-backed securities (RMBS) and servicing related assets (MSRs), completed an important internalization event in late 2024. This shift granted the company direct control of its investment decisions while it navigates a market environment defined by interest rate volatility and liquidity constraints. After volatile results including negative revenues in 2022 and 2023, the company returned to positive revenue generation in 2024 and 2025, albeit with significant year-over-year declines. Leverage remains a critical component of its RMBS financing strategy, contributing both to risk and return dynamics. Dividend distributions have been maintained at substantial levels, supported by improved operating cash flows in 2025.

Company Overview

Cherry Hill Mortgage Investment Corporation is a Maryland-incorporated publicly traded REIT focusing on residential mortgage finance within the U.S., managing portfolios primarily composed of Agency RMBS and Servicing Related Assets (notably MSRs and Excess MSRs). Since its IPO commencement in October 2013, Cherry Hill has sought to deliver current income through dividends supplemented by capital appreciation [S1][S18].

A pivotal change occurred with the completion of an internalization event in November 2024, which replaced external management by Cherry Hill Mortgage Management, LLC with an internally managed structure. This move brought direct hire of senior management personnel previously contracted externally—aiming for enhanced integration of strategy execution and operational oversight without paying termination fees for ending the external management agreement [S1][S18].

Historical Performance

Cherry Hill has experienced fluctuation throughout recent years due mainly to adverse conditions in the residential mortgage market and capital markets volatility. The company reported losses in revenue during FY2022 (-$31.1 million) and FY2023 (-$21.2 million), reflecting the challenges faced across the mortgage-backed securities sector heightened by volatile interest rates and credit concerns [F1]. However, revenue recovered to a positive $34.6 million in FY2024 before contracting again to $23.3 million in FY2025, representing a -32.5% year-over-year decline [F1].

Operating cash flow followed a similar volatile pattern, turning sharply negative at -$4.7 million in FY2024 after strong cash inflows the prior two years ($59.9 million FY2022, $40.7 million FY2023) before bouncing back positively to $19.1 million in FY2025 [F1].

Equity base showed some contraction consistent with earnings trends: equity stood at approximately $236 million at FY2025 year-end compared to about $262 million at FY2022 year-end [F1]. Dividend distributions have been consistently maintained near ~$28–31 million annually over the last four years despite income volatility [F1].

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | Rev YoY |

|---|---|---|---|

| 2025 | 23 | 19 | -32.5% |

| 2024 | 35 | -5 | +263.1% |

| 2023 | -21 | 41 | +31.9% |

| 2022 | -31 | 60 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) |

|---|---|

| 2025 | 29 |

| 2024 | 28 |

| 2023 | 31 |

| 2022 | 31 |

Source: SEC companyfacts cache [F1].

The table summarizes key financial metrics highlighting fluctuating revenue and cash flows alongside steady dividend payments.

Asset Composition & Strategy

Cherry Hill’s asset deployment currently focuses on two main segments: investments in Agency RMBS — residential mortgage pass-through certificates with exposure focused mainly on government-sponsored enterprises (GSEs) — and Servicing Related Assets including MSRs held through its taxable REIT subsidiary Aurora Financial Group Inc., which manages servicing operations via third-party subservicers [S18][S23].

The RMBS portfolio predominantly comprises whole-pool Agency RMBS but may opportunistically include non-Agency RMBS (including private label post-2010 issues) and GSE risk-sharing securities that offer credit protection related to defaults on loan pools insured by Fannie Mae/Freddie Mac [S20][S23].

Servicing Related Assets strategy involves acquisition of MSRs from originators or other servicers on both bulk or flow bases; these MSRs provide contractual rights to collect servicing fees on underlying mortgage loans without direct servicing obligations—outsourced instead through third-party servicers [S23][S27]. Intercompany Excess MSRs are created from MSRs acquired by Aurora and transferred internally benefiting from REIT tax treatment when guidelines are met.

Capital Structure & Leverage

Leverage underpins Cherry Hill’s investment capacity especially for Agency RMBS financing, predominantly sourced via short-term master repurchase agreements (repurchase transactions backed by underlying RMBS collateral). These repo financings typically involve sale-and-repurchase contracts with maturities ranging from approximately one month up to one year [S4][S6][S10].

While enabling substantial financing flexibility without fixed targeted debt-to-equity ratios, this leverage exposes Cherry Hill to margin calls triggered by asset value declines or fluctuations in collateral valuations—requiring additional cash or collateral postings that can pressure liquidity [S5][S7][S10][S22]. The company also utilizes revolving credit facilities secured by MSR portfolios for its servicing-related asset investments totaling up to $200 million across Fannie Mae and Freddie Mac focused facilities [S4].

Interest rate hedging is extensively employed using instruments such as interest rate swaps, Treasury futures, swaptions, TBAs (to manage prepayment/duration/basis risks), Eris SOFR swap futures among others aiming to mitigate interest rate volatility impacts on both asset yields and financing costs while preserving REIT status requirements [S8][S14].

Risks & Operational Considerations

Key risks stem from sensitivity to macroeconomic factors influencing home prices, borrower delinquency rates, prepayment speeds, housing demand shifts—all correlated heavily with mortgage market performance impacting asset valuation and yield stability [S1][S15][S16]. The company depends on third-party mortgage servicers for loan servicing activities underlying its MSRs; any servicer failures or contract terminations could materially impair operations or collections [S15][S27]. Liquidity risks arise given reliance on short-term repo markets that can experience tightening or increased haircuts requiring additional collateral or forced asset sales potentially at depressed prices [S11][S12][S22]. Regulatory changes impacting mortgage servicing practices or REIT qualification rules may also influence future capital allocation options or operational constraints [S19][S21].

Additionally, heavy dependency on analytical models for asset valuation introduces model risk—including incorrect assumptions could lead to mispricing or misguided acquisition decisions impacting portfolio returns [S9]. Cybersecurity considerations related to data shared with servicers add potential vulnerabilities though no material incidents are currently reported [S11].[N1]

Outlook & What To Watch

With no explicit guidance available as of the latest filings, future performance will hinge on several critical factors: ability to selectively acquire high-quality servicing rights amid competitive bidding; maintenance of healthy repo financing terms under evolving credit market conditions; effective hedging of rising or volatile interest rates that continue shaping prepayment speed behavior; sustaining REIT distribution levels balanced against corporate tax impacts within its TRS subsidiaries; managing margin calls smoothly without forced liquidation; all against macroeconomic headwinds including possible inflationary pressures or geopolitical tensions affecting housing demand.

From an operational perspective engineers will pay close attention to the ongoing integration benefits from the internalization event—whether cost savings or agility gains translate into better risk-adjusted returns—and how strategic shifts toward servicing assets versus RMBS evolve given relative return profiles.

Industry-wise this niche of residential real estate finance remains competitive with other mortgage REITs focusing efforts toward combining rigorously managed leverage structures alongside diversified asset classes that offer defensible risk-return tradeoffs amidst ongoing Fed monetary tightening cycles.

Capital Allocation & Returns

Cherry Hill maintains disciplined capital allocation priorities supporting substantial dividend distributions mandated by REIT rules—distributing nearly all taxable income annually—which totaled approximately $28.7 million in fiscal year ended December 31, 2025 despite net revenue contraction from prior years [F1][S20].

Operating cash flow profitability improvement in FY25 facilitates these payouts without immediate pressure on capital reserves highlighted by over $54 million cash & equivalents balance at year-end providing liquidity buffers against margin calls or market dislocations [F1][S4]. The company has refrained from share repurchases since fiscal year ended December 31, 2022 reflecting prudent capital deployment preferences amid uncertain environment [F1].

Return on equity approximates modestly below industry averages around ~7.9% based on latest net income relative to equity book value suggesting room for enhancement as portfolio mix optimizes under internalized management leadership structure [F1].

This analysis synthesizes publicly filed SEC disclosures as of March 5, 2026 ([F1],[S1]-[S29]) combined with industry contextual understanding relevant at time of writing without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments