Cryoport’s Return: Rebounding Revenue and Strategic Refocus in Temperature-Controlled Logistics

Cryoport navigates a significant revenue contraction alongside a sharp net income turnaround, driven by strategic divestitures and cost optimization within the high-stakes biopharma cold chain sector.

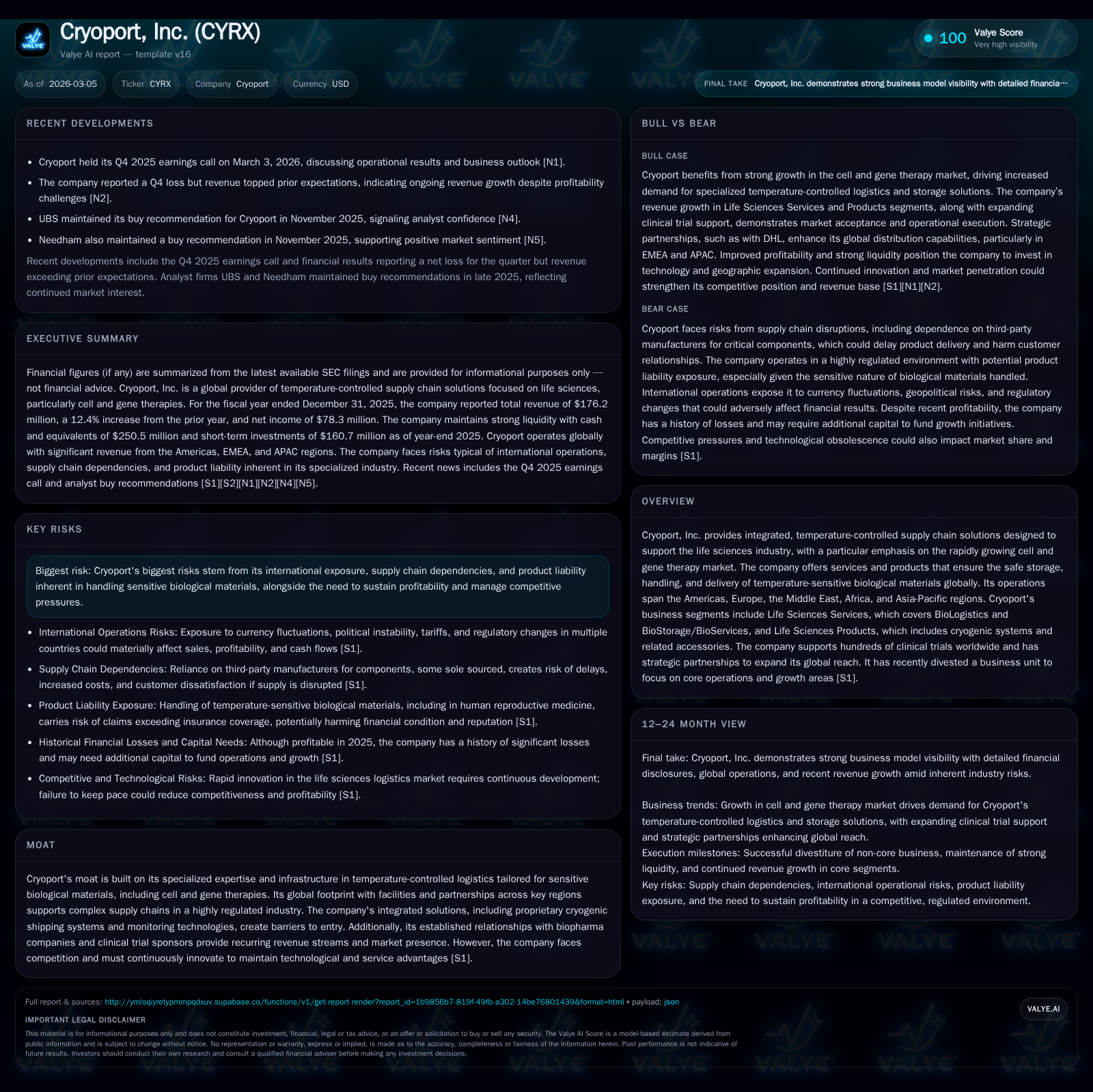

Cryoport, Inc. experienced a steep revenue decline of nearly 23% in FY2025 after years of rapid growth but achieved a notable swing to positive net income, supported by substantial operating loss reduction. The company executed a focused divestiture strategy to sharpen its core Life Sciences Services and Products offerings, particularly targeting cell and gene therapy logistics, while managing large international regulatory and operational challenges. Capital allocation has favored share repurchases and debt reduction amid ongoing investments in cryogenic infrastructure crucial for cold chain integrity. Key metrics to monitor include customer concentration shifts, clinical trial demand, pricing dynamics, and capital structure adjustments.

A Brief Retrospective: From Rapid Growth to Revenue Contraction

Cryoport's trajectory over recent years showcases a compelling story of brisk expansion tempered by an abrupt revenue pullback. After scaling revenues from approximately $60.4 million in FY2022 to peaks exceeding $230 million by FY2023, FY2025 witnessed a steep reversal with total revenues declining 22.9% year-over-year to $176.2 million [F1]. This retreat can be understood within the context of the company recalibrating its supply chain capacity utilization amid evolving customer demand patterns in the biopharma sector.

The Life Sciences Services segment—which bundles BioLogistics and BioStorage/BioServices—continued steady growth with revenue reaching $96.5 million aided by increased cryopreservation services adoption and expanded clinical trial support [S6, S24]. Meanwhile, Life Sciences Products showed resilience with strategic manufacturing enhancements enhancing margins despite the top-line softness.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 176 | 78 | -9 | -37 | -22.9% | +168.2% |

| 2024 | 228 | -115 | -16 | -131 | -2.1% | -15.2% |

| 2023 | 233 | -100 | -1 | -115 | +286.5% | -166.8% |

| 2022 | 60 | -37 | -2 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 10 | -25 | 15.6 |

| 2024 | 38 | -34 | -28.6 |

| 2023 | 38 | -40 | -20.4 |

| 2022 | 38 | -24 | -6.7 |

Source: SEC companyfacts cache [F1].

Table: Cryoport Annual Financial Performance Highlights (FY2022-FY2025) [F1]

Unpacking the Drivers Behind FY2025’s Income Turnaround

The pronounced improvement from an operating loss of $130.9 million in FY2024 to a much narrower $36.8 million deficit in FY2025 is attributable to tight cost management initiatives combined with favorable shifts in product mix [N1, S18]. Gross margin expanded to 47.1%, up from 44.4% prior year, propelled by higher-margin service offerings within BioServices and efficiencies gained from manufacturing innovations in cryogenic products.

Operating expenses saw meaningful reductions via workforce optimization, contractor utilization cuts, and project reprioritization aligned with profitability goals outlined during earnings discussions [N1]. Notably, non-recurring gains related to business divestitures inflated net income figures resulting in a positive net income of $78.3 million despite persistent underlying operational losses [S1]. This includes a substantial gain on the divested CRYOPDP business which was classified as discontinued operations.

Strategic Realignment: Divestitures and Market Focus

A hallmark of Cryoport’s recent strategic pivot is the divestiture of non-core assets to concentrate efforts on high-value Life Sciences Services and Products segments dedicated to supporting cell and gene therapies (CGT) globally [S1, S6]. The targeted shedding of peripheral businesses enabled management to channel resources into proprietary cryogenic shipping systems integration and advanced supply chain monitoring technology, indispensable moats guarding market share against rising competition.

Capital expenditures have accordingly been realigned toward technology upgrades facilitating cold chain integrity enforcement across complex multi-national patient sample logistics [S22]. While such concentration enhances margins and operational coherence, it elevates reliance on specific verticals subjected to regulatory flux.

International Exposure and Regulatory Complexities in Life Sciences Logistics

Operating extensively across Americas, EMEA, and APAC regions, Cryoport confronts multifaceted risks including currency fluctuations, trade restrictions, import/export licensing regimes, and evolving data privacy laws such as GDPR that impose heavy compliance costs [S1, S5]. Political instability or pandemic outbreaks further threaten supply continuity.

The company's cold chain solutions necessitate rigorous adherence to clinical trial oversight regulations coupled with anti-corruption statutes like the U.S Foreign Corrupt Practices Act given international dealings [S5]. Mitigating enforcement risk involves continual investment in compliance protocols alongside active engagement with customs and data protection authorities—an operational imperative for handling shipment telemetry data tied to high-value biologics [S18].

Capital Deployment: Share Repurchases, Debt Reductions, and Investment Priorities

Cryoport's capital allocation strategy over recent years underscores disciplined balance sheet management complemented by shareholder-friendly buybacks [S7]. In FY2025 alone, the company repurchased approximately $10 million of common shares at an average price near $7.45 per share while managing convertible senior notes maturity efficiently through targeted repurchases totaling over $200 million authorized under two consecutive repurchase programs [S12].

Despite improved operational cash flows—reflected by approximately 47% CFO improvement—negative free cash flow persists principally due to sustained investment into cold storage infrastructure modernization totaling roughly $16.4 million annually [F1]. This capex supports scalable deployment of MVE Biological Solutions’ cryogenic freezers integral to differentiating service offers.

With equity increasing from around $402 million in 2024 to over $502 million at year-end 2025, Crpytoport achieved an approximate ROE of 15.6%, signaling effective use of capital amidst ongoing profitability transition [F1].

Monitoring Metrics: What to Watch in Cryoport’s Growth Prospects

Absent explicit forward guidance from management disclosures [N2], key near-term indicators warrant close observation:

- Customer concentration shifts: One client accounted for over 10% revenue concentration solely in Life Sciences Services segment last fiscal year—a new development compared with prior years’ dispersion [S8].

- Clinical trial activity volume: Increases fuel demand for advanced bio-logistics solutions vital for CGT sample transport reliability.

- Pricing power versus inflationary pressures: Margin resilience depends on successful pass-through of rising labor/material/transport costs amid subdued economic conditions [S6].

- Capital structure evolution: Maturity timelines for remaining 2026 Convertible Senior Notes approaching tight liquidity management windows [S14]. These factors collectively will shape Cryoport’s ability to sustain profitable growth while safeguarding its technological lead.

Sector-Specific Challenges: Handling Sensitive Biological Materials at Scale

Cryoport operates within one of the most exacting logistical landscapes where "cold chain integrity" is non-negotiable—failure risks irreparable damage both clinically and commercially [S1]. Maintaining precise temperature control over extended transit durations accompanied by real-time shipment monitoring telemetry distinguishes leaders from commoditized freight handlers.

Their solutions comply with stringent CGT compliance standards necessitating continuous calibration against FDA/foreign regulatory device classifications including potential Class II medical device designations requiring exhaustive validation processes [S13,S18]. Product liability exposure remains material given life-critical nature of samples handled; even limited warranty claims can evolve into reputational risks necessitating extensive quality assurance beyond traditional cold storage protocols [S9,S11].

Conclusion: Forecasting Cryoport’s Position in a Competitive Global Framework

Cryoport emerges from recent turbulence stronger strategically yet still navigating a delicate balance between risk exposures inherent in international complex supply chains and operational scaling demands required by burgeoning CGT markets [N1,F1,S1,S7]. Its integrated temperature-controlled logistics platform fortified by proprietary technology offers robust differentiation but requires continuous innovation complemented by vigilant regulatory adherence.

Capital allocation choices reveal an emphasis on debt reduction combined with selective share repurchases supportive of shareholder value preservation amidst capital-intensive investments critical for long-term competitiveness.

Ongoing refinement of service offerings focused squarely on high-growth cell and gene therapy verticals anchors the company's path forward but heightens dependency on regulatory developments outside its control.

Maintaining resilience against geopolitical uncertainties, foreign exchange volatility, product liability risks whilst capturing clinical trial expansion opportunities will determine whether Cryoport consolidates its foothold as a leader or faces margin pressures induced by aggressive competitors entering this niche life sciences logistics domain.

This analysis is based solely on public filings dated through March 5, 2026, earnings calls transcripts through early March 2026, news reports cited herein, and company factual data without speculation or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments