Lexicon Pharmaceuticals Navigates Growth and Funding Challenges Amid Clinical Progress

Lexicon has achieved notable revenue growth driven by collaborations but continues to face operational losses and capital demands tied to development-stage assets and rebuilding commercial capabilities.

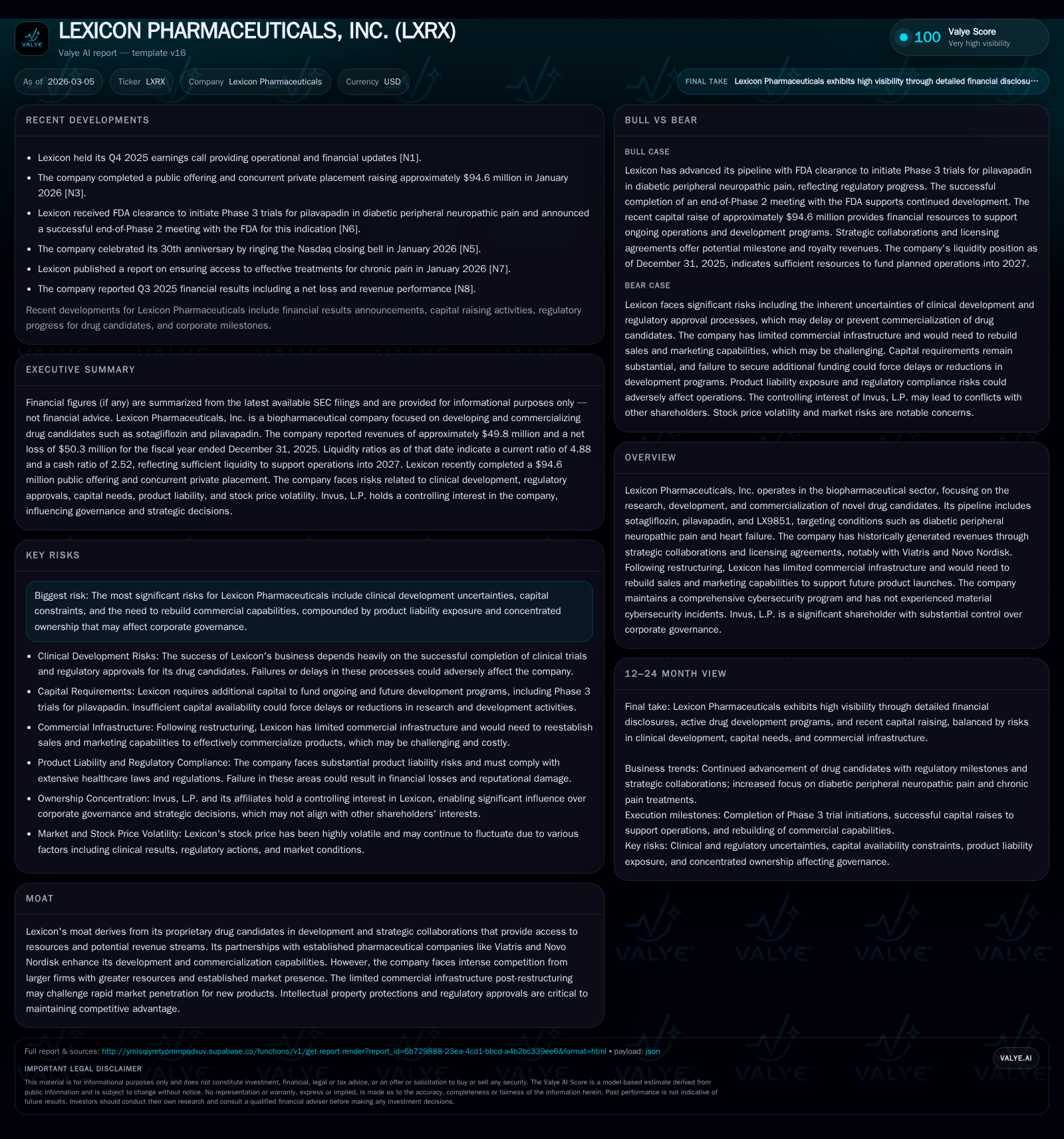

Lexicon Pharmaceuticals posted a strong revenue increase of over 60% in FY2025, reaching nearly $50 million, fueled primarily by collaboration income. Despite this growth, the company remains unprofitable with operating losses narrowing to $48.9 million due to ongoing R&D investment, notably in late-stage clinical trials including pilavapadin's Phase 3 program. Cash reserves declined to $34.3 million at year-end 2025, prompting a $94.6 million equity raise in early 2026 to support pipeline advancement and operations. Heavy indebtedness of approximately $54 million and restrictive covenants limit financial flexibility. Intellectual property risks, regulatory complexities, and a concentrated ownership structure with Invus L.P. holding nearly half the common shares present governance and operational challenges. The near-term outlook hinges on clinical milestones and effective capital management amid evolving healthcare market dynamics.

Historical Financial Performance

Lexicon Pharmaceuticals has demonstrated significant top-line growth over recent years, expanding from minimal revenues of $139,000 in FY2019 to about $12 million in FY2023. This accelerated substantially with revenues reaching approximately $31.1 million in FY2024 followed by a sharp increase of over 60% to nearly $49.8 million in FY2025 [F1].

This growth primarily stems from milestone payments, royalties, and licensing fees under collaboration agreements rather than direct product sales given Lexicon's focus on clinical-stage drug development [N1][S1].

Operating losses remain substantial but have contracted markedly from a peak operating loss of $197.1 million in FY2024 to $48.9 million in FY2025 as programs mature and spending stabilizes. Net losses follow a similar trend narrowing from $200.4 million to $50.3 million despite continued negative margins.

Cash flow from operations remains negative at -$67.8 million for FY2025 but shows improvement against prior periods (e.g., -$178.8 million in FY2024). Capital expenditures are minimal reflecting an asset-light model reliant on outsourcing manufacturing and development activities.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 50 | -50 | -68 | -49 | +60.2% | +74.9% |

| 2024 | 31 | -200 | -179 | -197 | +2481.5% | -13.1% |

| 2023 | 1 | -177 | -162 | -172 | ||

| 2019 | 0 | -102 | -89 | -101 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -68 | -46.8 | |

| 2024 | 1730000 | -180 | -137.3 |

| 2023 | 824000 | -162 | -190.2 |

| 2019 | 864000 | -90 | -87.0 |

Source: SEC companyfacts cache [F1].

Table: Key financial metrics illustrating revenue growth alongside persistent losses; buyback activity has been modest [F1]

Business Operations & Industry Context

Lexicon operates within the high-risk biopharmaceutical sector characterized by extended R&D cycles requiring substantial capital investment before commercialization potential can be realized. The company’s recent restructuring significantly reduced its commercial footprint following earlier reliance on collaborations for marketing late-stage assets such as INPEFA for heart failure indications [S1][N1].

Current pipeline assets include sotagliflozin targeting hypertrophic cardiomyopathy; pilavapadin for diabetic peripheral neuropathic pain—recently granted FDA clearance for Phase 3 trials—and LX9851 alongside other early-stage programs focusing on metabolic and neurological conditions [S1][N8][N9]. The upcoming Phase 3 clinical stages represent critical milestones but will require significant funding.

Regulatory compliance imposes complex challenges involving FDA approvals, manufacturing standards (cGMP), marketing restrictions including Anti-Kickback Statutes and False Claims Act provisions as well as evolving pricing regulations exemplified by the Inflation Reduction Act impacting Medicare drug pricing starting mid-2020s [S4][S5][S17]. These factors contribute to cost pressures and may constrain market access.

Capital Structure & Funding Dynamics

As of December 31, 2025 Lexicon held cash and cash equivalents totaling approximately $34.3 million—a decline reflecting operational cash burn outpacing inflows [F1]. To support costly late-stage development programs especially Phase 3 pilavapadin trials along with corporate activities amid commercial rebuilding efforts the company completed a public equity offering plus concurrent private placement raising roughly $94.6 million in January 2026 [N3][N4].

The balance sheet includes approximately $54 million in term loan debt subject to affirmative and restrictive covenants that may constrain Lexicon’s ability to secure additional financing or react flexibly to business developments; covenant breaches could trigger defaults with material consequences [S14][S15]. Sustained negative operating cash flow absent further capital raises or strategic partnerships will remain a key liquidity risk.

Intellectual Property & Regulatory Risk Profile

Lexicon’s competitive positioning depends on proprietary drug candidates protected through patents which require continuous legal defense amid industry-wide high litigation risk; patent applications pending issuance add uncertainty regarding exclusivity timelines [S6][S9][S18].

Regulatory approval pathways are inherently uncertain; trial outcomes may not meet efficacy or safety endpoints potentially delaying or halting product advancement while compliance with expansive healthcare laws presents ongoing operational challenges that could impact commercialization prospects [S4][S16][S25].

Product liability exposure exceeds current insurance coverage levels posing potential reputational or financial risks if adverse events occur post-marketing or during clinical trials [S7][S10][S12].

Governance & Ownership Concentration

Invus L.P., holding approximately 48% of common stock alongside convertible preferred shares convertible into common stock increasing ownership above majority thresholds (~50%), exerts significant influence over governance including board composition and major corporate decisions such as mergers or asset sales [S10][S16]. This ownership concentration may affect shareholder alignment dynamics.

Forward-Looking Considerations & Milestones

Key near-term catalysts include pivotal Phase 3 trial data readouts for pilavapadin following FDA clearance announced early 2026 which could materially affect developmental strategy or partnership opportunities [N8][N9]. Successful progression may necessitate either internal sales force rebuilding or new licensing agreements due to limited current commercial infrastructure [S25].

The recent capital raise provides runway into the coming year based on current plans but uncertainties persist around trial execution timing and cost escalation amid evolving regulatory landscapes that could impact reimbursement frameworks once products reach market.

Summary Assessment

Lexicon Pharmaceuticals exhibits encouraging topline growth driven by partnerships yet continues facing sizable operating losses fueled by intensive R&D investment without current full-scale commercialization capacity post restructuring. The company’s ability to successfully navigate upcoming clinical milestones coupled with prudent capital management will be critical amid governance dominated by a controlling shareholder.

Risks remain material across clinical development uncertainty, regulatory complexity, intellectual property protection challenges and liquidity constraints given persistent negative cash flows requiring ongoing financing or collaboration arrangements.

Monitoring should focus on pipeline trial progress and results timing; announcements regarding commercial partnerships or sales capability restoration; capital markets receptivity evidenced by future financings; regulatory developments affecting market access; and governance dynamics involving Invus’ influence.

This analysis is based solely on reported data extracted from Lexicon Pharmaceuticals' SEC filings including its latest Form 10-K filed March 5, 2026 ([F1],) and recent news releases () without speculative commentary or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments