AA Mission Acquisition Corp. II Charts Its Course to Food and Beverage Acquisitions

A newly public SPAC leverages sector expertise and China ties to pursue food and beverage targets while navigating unique regulatory risks.

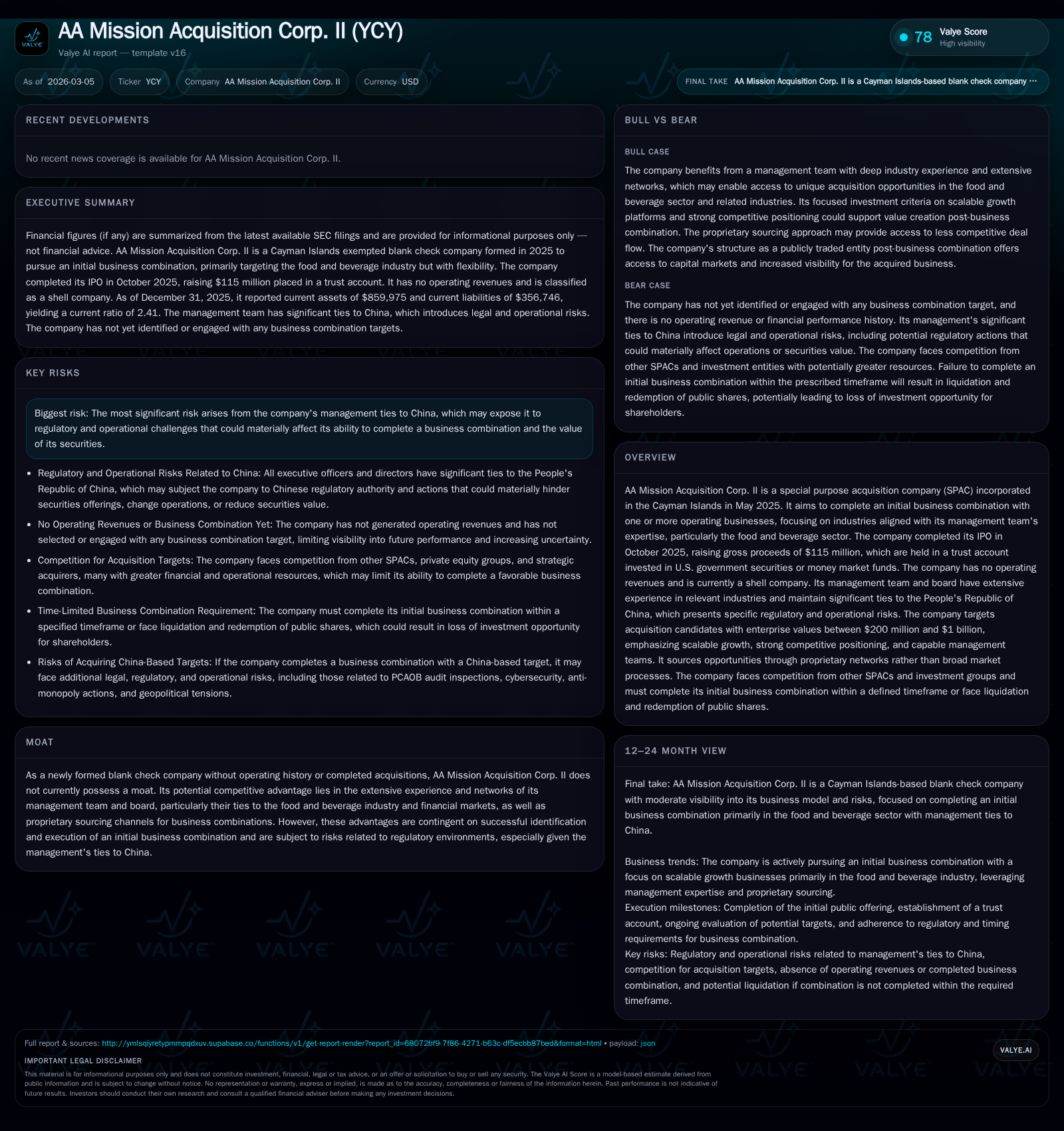

AA Mission Acquisition Corp. II (YCY) is a Cayman Islands-incorporated SPAC focused on acquiring businesses in the food and beverage sector, backed by a management team with deep industry experience and strong China connections. Having raised $115 million in its October 2025 IPO, funds are securely held in a trust account pending an initial business combination targeting companies valued between $200 million and $1 billion. The company currently operates as a shell with no revenues, facing regulatory and geopolitical risks primarily stemming from its management’s China ties. Investors should track milestone approvals, deal disclosures, and redemption terms as the SPAC moves toward consummating its initial acquisition.

Start-up Performance Snapshot: Operating from a Trust Account

AA Mission Acquisition Corp. II (Ticker: YCY) is a special purpose acquisition company incorporated in the Cayman Islands in May 2025, primarily serving as a blank check vehicle awaiting an initial business combination. The company held its IPO in October 2025, issuing 10 million units at $10 each, including an over-allotment executed fully by underwriters bringing gross proceeds to approximately $115 million [S10]. These funds are invested conservatively in U.S. government securities or qualified money market funds within a trust account — a hallmark of SPACs designed to protect investors’ capital until deployment in an acquisition.

From its latest available financial snapshot dated December 31, 2025, the company reported operating losses of approximately $497K reflective solely of administrative expenses given no operating activities, alongside a net income of roughly $585K likely derived from non-cash accounting entries or interest income on trust assets [F1]. Current assets stand near $860K while current liabilities total about $357K resulting in a current ratio of approximately 2.41 indicating solid short-term liquidity post-IPO [F1]. However, the company posted a negative approximate return on equity of -24.7%, consistent with startup status and non-operating cash flows [F1].

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Curation of Targets: Focused on Scalable Food & Beverage Opportunities

YCY’s business model centers on pursuing one or more business combinations targeting entities with enterprise values between $200 million and $1 billion [S5]. The company intends to leverage its management team's background to zero in on scalable platforms primarily within the food and beverage industry—an area where it believes it can add value based on operational knowledge and network connections.

Key investment criteria emphasize:

- Scalable growth potential: Preference for companies able to efficiently expand operations capturing new markets.

- Strong competitive positioning: Inclusion of factors like brand recognition, proprietary technology or superior cost structures.

- Management alignment: Targeting firms with professional leadership whose interests harmonize with shareholders.

- Public market readiness: Seeking companies positioned to benefit from capital markets access after becoming public [S7], [S14].

Their sourcing strategy leverages proprietary networks rather than broadly marketed processes, aiming for differentiated deal flow access—critical given competition from other SPACs, private equity firms, and strategic acquirers [S27]. This approach could foster exclusive opportunities but requires active network cultivation especially given YCY’s focus size range around mid-market targets.

Integration considerations post-business combination will hinge on operational synergies achievable within the public company structure—access to broader capital markets being one notable advantage highlighted [S14].

Management Team Expertise and China Connections: Opportunity Meets Risk

Distinctively, YCY’s management team and board comprise individuals with decades-long experience spanning food & beverage operations, capital markets transactions including SPACs, private equity investing, M&A advisory roles, and executive management in listed companies [S1], [S7], [S28]. This collective expertise underpins their ability to source proprietary deals and negotiate favorable terms.

However, all executives have significant ties to the People’s Republic of China (PRC), which is both an asset for target sourcing within Asia but also a substantial risk factor. Regulatory uncertainty around Chinese jurisdiction presents potential legal entanglements that might affect deal approvals or post-merger operations [S17], [S18]. The company explicitly avoids VIE structures within China due to audit inspection concerns but acknowledges risks related to cross-border regulatory reviews including possible U.S. governmental restrictions on transactions involving PRC-linked entities.

Geopolitical tensions could induce delays or discourage non-China-based targets from engaging given perceived additional compliance risks. Consequently, investor risk exposure encompasses potential disruptions tied not only to the transaction itself but also to future combined entity operations subject to evolving PRC regulatory landscape [S9], [S17].

Capital Structure, Cash Flow Status, and Shareholder Interests from IPO to Today

The capital base stems from both public shareholders purchasing Class A ordinary shares bundled into Units ($10 each) during IPO plus founder (“sponsor”) shares representing roughly 20% of total shares post-offering — about 2.875 million founder shares issued pre-IPO at nominal cost [S10]. The sponsor made small private placements concurrent with IPO totaling several million dollars contributing alongside gross proceeds pooled into the trust account.

Funds held are restricted primarily for use in consummating the initial business combination per SEC rules governing SPACs; usage outside such purposes is minimal excluding payment of organizational expenses funded from amounts outside trust assets [S6], [S19]. No dividends or share repurchase programs have been initiated given early-stage status; sponsor agreements waive liquidation rights on founder shares in case no acquisition occurs within prescribed completion window but retain such rights if founders acquire public shares later [S6], [S8].

Redemption features grant public shareholders rights at business combination vote events or tender offers to redeem shares pro rata for cash equal to trust account amounts per share (~$10.025), subject to conditions ensuring minimum combined net tangible assets; forced redemptions can lead to deal withdrawal if thresholds unmet—all forming built-in shareholder safeguards against poor acquisitions or dilution [S4], [S8], [S16].

Cash flow remains largely confined to inflows from interest earned on the trust investments offset by minimal outflows tied to administrative fees borne outside the trust [F1], consistent with standard SPAC mechanics before acquisition.

Governance Provisions Shaping Transaction Approval and Public Shareholder Redemption

YCY’s articles of association prescribe strict governance protocols governing transaction approvals including:

- Requirement for ordinary shareholder resolution (>50% affirmative vote) for mergers that would involve transfer of more than 20% outstanding shares or amendments affecting shareholder rights [S3].

- Quorum defined at one-third shares present or proxy representation at meetings ensuring sufficient shareholder engagement; founder shares committed by voting agreements supporting deal approval easing threshold attainment by reducing opposition risk [S15].

- Redemption mechanics vary based on whether conducted via tender offer regulated by Rule 13e-4 or proxy solicitation under Regulation 14A; both involve SEC filings ensuring transparency through detailed disclosure documents sent preceding votes or offers [S4], [S11].

- Shareholders electing redemption must timely tender certificates or electronically deposit shares prior to meetings/votes avoiding delays distributive timing issues [S4].

- Provisions ensure redemptions cease if minimum net tangible asset requirements post-acquisition cannot be met protecting surviving entity’s solvency integrity [S16].

These frameworks balance investor protections against transaction facilitation while embedding disclosure rigor preventing ill-informed decisions.

What Lies Ahead: Pipeline Exploration and Metrics to Monitor for Deal Success

To date YCY has not announced any definitive initial business combination nor engaged in substantive discussions publicly disclosed beyond ongoing opportunity reviews described in filings [S10]. Near-term milestones critical for shareholders include:

- Announcement of a chosen target providing clarity on industry subsector, financial profile, and strategic rationale.

- Disclosure of definitive agreement details outlining purchase price valuation metrics relative to trust funds.

- Scheduling of shareholder vote/certification dates determining redemption election results signaling investor confidence.

- Observed redemption rates which could impact residual capital available for deal closure or operational funding.

- Timeliness against statutory completion deadlines defining conditional liquidation scenarios driving urgency.

The absence of concrete pipeline updates augments uncertainty making these forthcoming markers primary indicators guiding investor monitoring efforts until a transaction conclusion emerges.

Valye Analysis: Forecasting Constraints and Milestones Beyond Year One

As a vehicle without current operating revenues or cash flow generation capacity except trust interest income constrained by regulatory design limits upside absent successful combination execution. Growth ambitions hinge entirely on identifying appropriately scaled targets within purview emphasizing food & beverage sector scalability matching management capability sets.

Regulatory dynamics inherent due largely to China affiliations impose potential valuation discounts or elongated timelines that could dampen returns despite sourced advantages. Redeeming shareholder protections insulate downside risk but simultaneously constrain available capital post-deal possibly impacting working capital buffers post-combination.

Important metrics beyond transactional close will include operational cash flow ramp-up capacity within acquired businesses validating target selection quality alongside subsequent return profiles amenable for eventual dividends or buyback strategies absent today’s inactivity.

Investors should weigh these structural factors alongside transparent progress reports considering that common SPAC lifecycle risks traverse deal execution probability through execution quality phases — compounded here by added geopolitical overlay unique to YCY's profile.

This analysis is based strictly on AA Mission Acquisition Corp. II's publicly filed SEC documents as of March 5, 2026 ([F1],[S1]-[S28]) without speculative projections beyond company disclosures. No investment advice is offered herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments