Inuvo's AI-Driven Pivot: From IntentKey Innovation to Financial Hurdles

Inuvo leverages patented generative AI in advertising while confronting profitability and liquidity challenges.

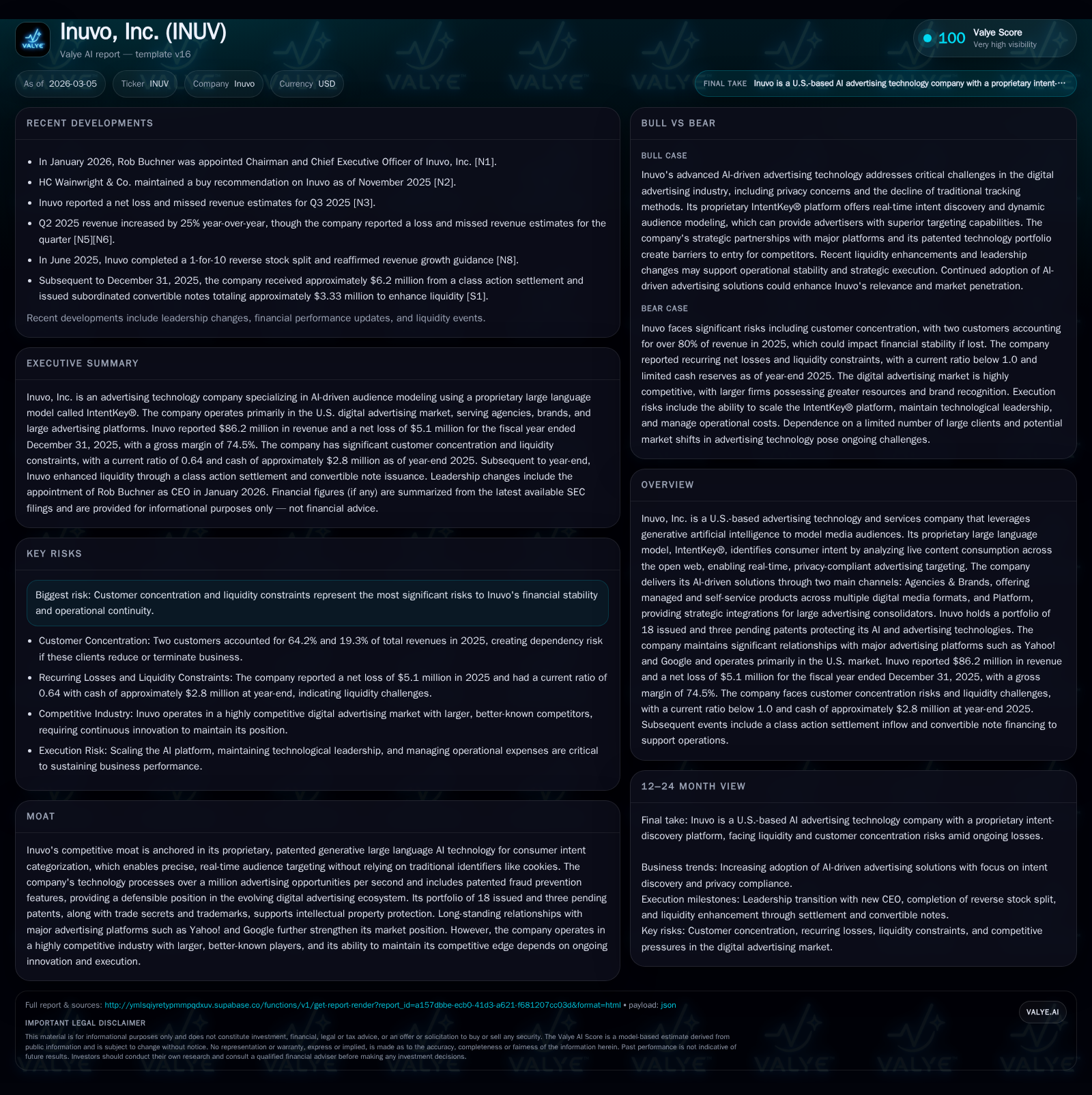

Inuvo, Inc. capitalizes on its proprietary large language model, IntentKey®, delivering advanced real-time consumer intent discovery for programmatic advertising. Despite revenue growth to $86.2 million in 2025, the company continues to face operating losses and strained cash flows, driven by concentrated customer risk and liquidity pressures. Its competitive moat centers on patented AI technologies and strategic partnerships with major ad platforms, but sustaining growth hinges on improving profitability and managing capital.

Proprietary AI Innovation Underpinning Inuvo’s Growth Trajectory

Inuvo distinguishes itself within the advertising technology domain through its proprietary large language model (LLM) branded IntentKey®. This generative artificial intelligence model analyzes live content consumption across the open web in real time to categorize consumer motivations rather than relying on traditional identifiers such as third-party cookies or IP addresses [S1]. The technology maps human intent onto a vast concept graph of over 25 million ideas, enabling early detection of emerging audience trends roughly 24 hours before they gain market competition [S1].

IntentKey® operates seamlessly within programmatic bid streams by responding dynamically to over a million advertising opportunities per second. Its architecture integrates patented fraud prevention capabilities to safeguard advertiser investments alongside precision audience targeting [S5]. This technological differentiation positions Inuvo’s agentic system–compatible AI as a neural network for autonomous media planning agents, facilitating a shift away from static historical data toward adaptive real-time intent categorization [S1].

Accompanying IntentKey are complementary tools such as IntentPath®, providing marketers with real-time visualization of audience journeys from discovery to conversion, and Ranger®, which applies AI-driven quality assurance within the Campsight platform for message consistency and compliance across digital campaigns [S1].

Reviewing Revenue Trends and Earnings Performance: Progress with Profitability Still Elusive

Inuvo recorded net revenues of $86.2 million in fiscal year 2025, reflecting a 2.9% increase compared to $83.8 million in 2024 [F1]. This moderate top-line growth reflects increased client onboarding—15 new Agencies/Brands were signed in 2025—but was coupled with margin pressure from a revenue mix shift leading to a gross margin decline from 85.6% in 2024 to 74.5% in 2025 [S15].

Operating income deteriorated by 21.4% year-over-year, resulting in an operating loss of approximately $6.7 million in FY2025 down from $5.5 million the prior year [F1]. Net loss improved marginally by around 11.6%, totaling roughly $5.1 million versus $5.7 million last year, signaling some cost control amid still challenging profitability dynamics [F1]. However, operating cash flow weakened substantially with negative cash generation of nearly $1.8 million compared to positive $229 thousand in FY2024—a decline exceeding 870%—largely due to decreased receivables collection efficiency amid slower media sales payment terms relative to payables [F1][S25]. Capital expenditures mainly reflect internally developed software costs at about $1.6 million annually [F1][S27].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | -2 | -7 | 1601903 | +11.6% |

| 2024 | -6 | 0 | -6 | 1857375 | +44.5% |

| 2023 | -10 | -3 | -10 | 1682683 | +20.7% |

| 2022 | -13 | -6 | -13 | 1689869 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -50.8 |

| 2024 | -2 | -42.8 |

| 2023 | -4 | -61.2 |

| 2022 | -7 | -60.3 |

Source: SEC companyfacts cache [F1].

Intent Discovery Technology as a Competitive Moat in Programmatic Advertising

Inuvo’s moat rests on its suite of patented generative AI inventions that redefine audience targeting paradigms within programmatic advertising ecosystems [S5]. By cataloging intent data mapped onto concept graphs surpassing 25 million discrete ideas, the company achieves precision targeting capabilities that competitors relying predominantly on legacy cookie-based data struggle to replicate.

Further reinforcing its technical defensibility are patents concerning sophisticated advertising fraud detection algorithms integrated into its platforms—both core patents and patent-pending assets contribute to barriers for newer entrants or larger incumbents who face challenges surpassing real-time supply/demand yield optimizations embedded in bid stream management [S5]. The use of agentic systems for adaptive media allocation underlines sector-specific differentiation where Inuvo acts as an intelligence layer enabling autonomous media buying agents.

This technology facilitates superior monetization by aligning messaging dynamically with consumer intent signals captured live online—contrasting offline or lagging data feeds—and provides marketers transparency into evolving consumer mindsets via IntentPath visualization tools while ensuring compliance hygiene through Ranger monitoring [S26][S9]. Such modular AI-driven orchestration across both demand-side (Agencies & Brands) and supply-side (Platform integrations) enhances scalable adoption across varied digital channels including CTV, video, audio, native, and display formats [S9][S13].

Risk Factors: Customer Concentration and Liquidity Constraints

A material strategic risk lies in significant customer concentration—two customers generated more than 80% of total revenues in fiscal year 2025 (64.2% and 19.3%, respectively) [S6][S9]. Such dependency exposes Inuvo’s revenue base to volatility if one client reduces spending or discontinues engagement.

Liquidity pressures are evident given a net working capital deficit of approximately $5.1 million against cash reserves near $2.8 million as of December 31, 2025 [F1][S7]. Negative operating cash flow alongside accumulated deficits exceeding $178 million underscores persistent funding needs supported historically through equity issuance and debt draws rather than internal cash generation [F1][S7]. Media sales contracts feature slower payment terms relative to payables which compresses operating cycles further intensifying short-term financing requirements [S25].

Additionally, Inuvo’s credit facility with SLR Digital Finance LLC—a commitment up to $10 million secured primarily by accounts receivable—is subject to eligibility criteria limiting borrowing capacity tied to receivables aging and geography [S4][S20]. At year-end, the outstanding balance stood at approximately $3.3 million bearing interest at prime plus one percent but no less than seven percent per annum—a relatively high financing cost impacting net margins amid losses [S7][S20].

Capital Structure Evolution and Funding Strategy

Capital structure developments include the initiation of an At-The-Market offering agreement effective May 2024 enabling flexible equity raise capacity up to $15 million; proceeds realized in FY2025 totaled about $1.18 million from sales of common stock under this program [S4][F1]. Post-fiscal-year events comprised issuance of subordinated convertible notes aggregating approximately $3.33 million with an original issue discount of ten percent convertible at $3.10/share under specified NYSE American limits enhancing immediate liquidity post December 31, 2025 [S11][N1].

Repayment obligations under the SLR credit line rely principally upon collections from eligible accounts receivable; termination fees apply depending on timing relative to agreement anniversaries constraining flexibility but providing multi-year access through January 2027 subject to covenant compliance [S4][S20]. Facility fees include a minimum utilization fee besides interest payments implying fixed costs even if drawdowns remain low.

These financing arrangements reflect management’s strategy to bridge financing until positive operational cash flow can be achieved through scale-up of proprietary offerings notably IntentKey-powered services within both Agencies & Brands and Platform channels accelerating go-to-market execution following leadership appointments including CEO Rob Buchner effective early 2026 [N1][S13].

Operational Highlights: Segments, Geographic Focus and Partner Ecosystem

Inuvo operates as a single reportable segment focused almost exclusively on the United States market generating most revenues domestically through digital device inventories spanning social media, search engines, streaming CTV channels, native advertising leases, video, audio formats among others [S6][S9][S22]. Dual business lines include:

- Agencies & Brands: Managed service offers plus self-service SaaS leveraging IntentKey intelligence for targeted campaign activation emphasizing brand safety.

- Platform: Strategic integration services for major consolidators like Yahoo! and Google that aggregate advertising demand optimizing quality control and scalability through AI matching merchant messaging with content contextually over open web inventories.

Long-standing contracts with marquee platform partners underpin distribution scale while proprietary tools continue evolving offering tactical leverage over generic demand-side platforms reliant chiefly on ID-based targeting now curtailed by privacy rules around cookies hence accelerating switch towards intent categorization models embedded at AdTech layers [S9][S13].

Capital Allocation Efficiency: Assessing ROE, Cash Flows, and Shareholder Returns

Return metrics remain deeply negative owing primarily to continued operating losses amidst investment phases; calculated approximate return-on-equity stands near -50.8% based on net income against shareholders’ equity around $10 million at year-end fiscal 2025 highlighting significant deficit absorption relative to capital base [F1]. Free cash flow is also negative estimated near -$3.39 million after capex outlays reflecting ongoing commitment towards software development primarily related to IntentKey maintenance/enhancements alongside system scaling efforts that inherently depress near-term earnings capacity.

No dividends or share repurchases occurred reflecting prudent retention given financial headwinds; management appears focused chiefly on directing capital toward sustaining competitive positioning rather than shareholder distributions at this stage pending profitable inflection [F1][S29]. This cautious reinvestment approach prioritizes maintaining unique AI assets and expanding client integrations crucial for ensuring future monetization upside aligns with evolving market demands.

This analysis synthesizes publicly available regulatory filings combined with recent management commentary without offering investment recommendations or price targets. All financial values adhere strictly to reported figures without extrapolation beyond disclosure dates. Readers should consider potential additional risks not covered here including litigation outcomes or market shifts affecting technology adoption rates.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments