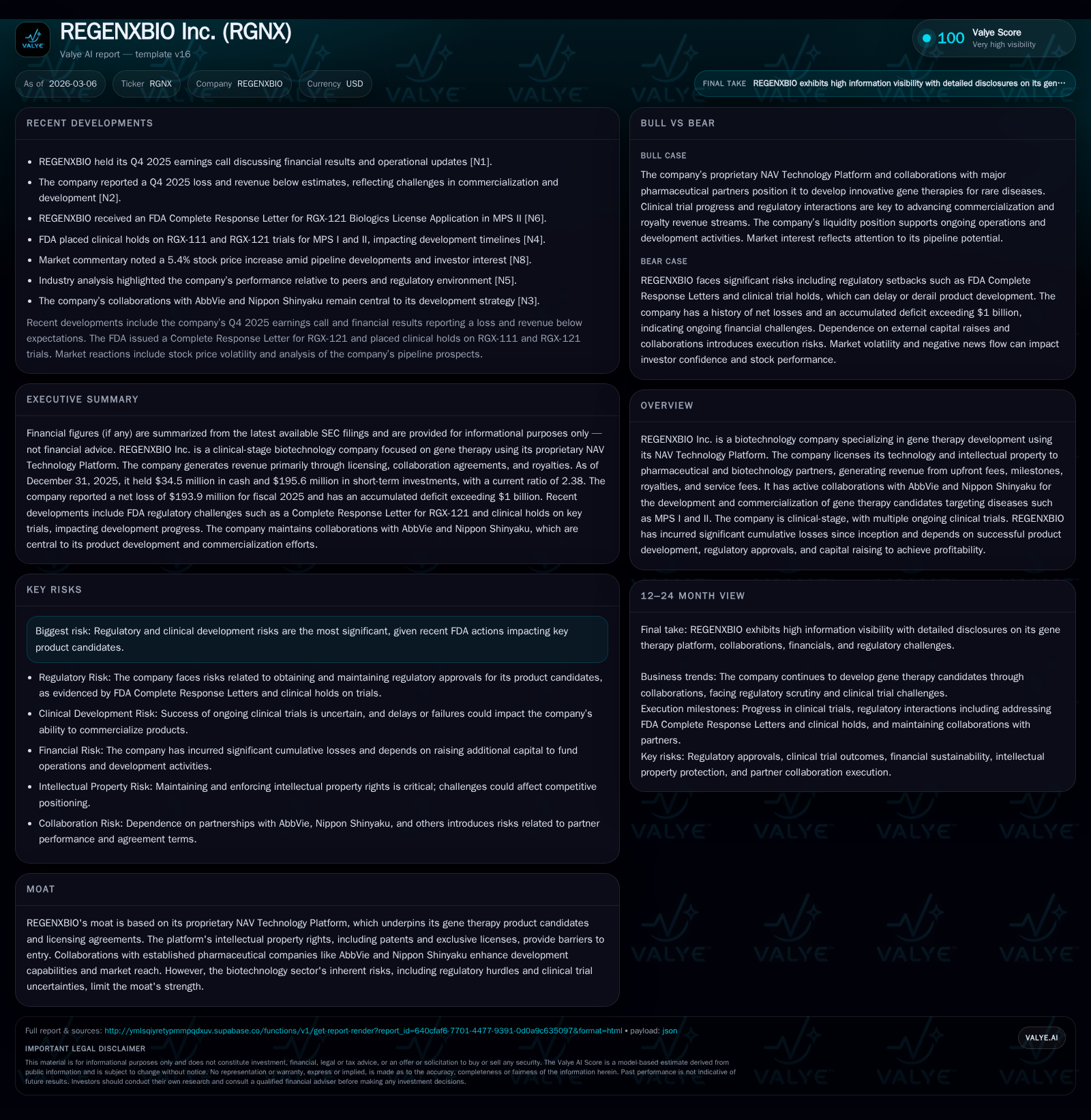

REGENXBIO Battles Regulatory Hurdles Amid Ongoing Gene Therapy Development

A clinical-stage biotech with a proprietary gene delivery platform faces mounting losses and financing needs amid shifting regulatory dynamics.

REGENXBIO Inc. has developed a unique NAV Technology Platform facilitating gene therapy development, licensing it to pharma partners including AbbVie and Nippon Shinyaku. Despite a 20% revenue growth in 2025, the company remains unprofitable with rising operating losses and negative cash flows due to clinical trial holds and FDA scrutiny of lead assets targeting MPS I and II. Cash reserves near $34 million at year-end suggest limited runway, emphasizing the importance of partnership milestones, regulatory approvals, and capital raises for sustaining operations. Licensing royalties and milestone revenues from collaborations represent key near-term growth drivers but remain subject to clinical progress and FDA decisions.

Company Overview

REGENXBIO Inc. operates as a clinical-stage biotechnology firm focusing on gene therapy development through its proprietary NAV Technology Platform—an exclusive portfolio of adeno-associated virus (AAV) vectors designed to deliver gene therapies as one-time treatments for various serious diseases [S1][S12]. The company’s business model partly revolves around licensing its technology platform to pharmaceutical collaborators such as AbbVie and Nippon Shinyaku. Revenue streams derive from upfront license fees, milestone payments tied to development or sales triggers, royalties on commercialized products, and service fees linked to development activities [S27].

While internal product candidates remain in clinical stages with ongoing trials addressing diseases like mucopolysaccharidosis types I (MPS I) and II (MPS II), REGENXBIO has faced significant regulatory challenges impacting commercialization timelines [N7][N11]. Financially, the entity has sustained large cumulative net losses since inception and depends heavily on raising further capital alongside successful product development for eventual profitability [S4][F1].

Historical Performance Highlights

REGENXBIO’s financial trajectory over recent years illustrates growth in top-line revenue accompanied by persistently steep operating expenses related to research and development:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -194 | -124 | -161 | 2 | +14.6% |

| 2024 | -227 | -173 | -233 | 2 | +13.8% |

| 2023 | -263 | -218 | -268 | 10 | +6.0% |

| 2022 | -280 | -207 | -263 | 31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -126 | -188.7 |

| 2024 | -176 | -87.5 |

| 2023 | -228 | -84.5 |

| 2022 | -238 | -54.3 |

Source: SEC companyfacts cache [F1].

(Financial figures except revenue were explicitly reported; revenue stated only for early years without consistent recent data to tabulate [F1])

The company recorded a roughly 20% year-over-year improvement in revenue for FY2025 over FY2024 per management commentary [N1], though absolute revenue remains low relative to high operating expenses. Operating losses shrank by near 31%, indicating some cost management or milestone-related revenue recognition effects. Net loss improved comparably but continues reflecting the high-cost nature of late-stage biotech innovation.

Cash flow from operations remained substantially negative at almost $124 million for the year ending December 2025 while capital expenditures held steady at modest levels (~$2.4 million), implying continued investment focused primarily on R&D infrastructure rather than large-scale fixed assets [F1][S1].

Cash balances fell perilously low to approximately $34.5 million by year-end—a marked decline from June’s liquidity buffering near $363 million noted earlier [S4][F1]. This steep drawdown is attributable primarily to sustained operating deficits combined with limited near-term commercialization revenues.

Industry Context

The gene therapy sector embodies exceptional promise due to potentially curative single-dose treatments for rare genetic diseases but remains fraught with risks including complex manufacturing processes using viral vectors like AAVs. Navigating the stringent FDA approval environment requires extensive clinical data demonstrating durable efficacy and safety in small patient populations . Competition intensifies not only among direct gene therapy developers but also from emerging modalities such as RNA therapies that challenge conventional approaches.

Licensing models are common industry practice whereby platform owners partner with pharma groups to share costs/risks while enabling global commercialization scale-ups . As such, REGENXBIO’s strategy blends internal innovation pipelines augmented by partnerships that distribute development responsibilities while leveraging its NAV platform’s intellectual property moat.

Future Growth Drivers and Constraints

Key catalysts include potential advancement or approval of therapeutic candidates RGX-111 targeting MPS I and RGX-121 for MPS II—although recent regulatory setbacks have complicated paths forward: The FDA issued a Complete Response Letter for RGX-121’s Biologics License Application citing outstanding data requirements; concurrent clinical holds were placed by regulators affecting both RGX-111 and RGX-121 trials pending resolution of manufacturing/process issues [N7][N11]. These events materially dampen near-term revenue visibility and elevate execution risks.

Collaborations under active agreements with AbbVie and Nippon Shinyaku provide structured avenues for future royalty streams alongside milestone receipts based on product development progress or sales performance [S27][N1]. Expanding these partnerships or entering new licensing deals could drive longer-term growth if REGENXBIO’s platform demonstrates durable clinical success.

However significant uncertainty remains around timing of regulatory clearances due to incomplete data packages or inspection outcomes typical in gene therapy manufacturing scale-up phases [N7][S7]. Failure or prolonged delays could severely impair financial viability given heavy reliance on partnership-dependent revenue.

Guidance and Milestones to Watch

REGENXBIO has not issued detailed formal earnings guidance or explicit milestone timelines beyond standard collaboration terms reported [N1][S3]. Market observers should focus on:

- FDA correspondence outcomes relating to RGX-111/RGX-121 clinical hold lifts or supplemental data submissions.

- Clinical trial enrollment rates and interim efficacy/safety readouts across pipeline programs.

- New partnership announcements that might reinforce monetization of NAV Technology Platform rights.

- Capital raising activities prompted by constrained cash runway expenditure patterns observed late-2025.

Maintaining operational continuity through funding will be crucial considering burning negative free cash flow exceeding $126 million annually coupled with limited internal revenues—signaling ongoing dilution risk if equity markets fluctuate unfavorably [F1][S4].

Capital Allocation and Returns Profile

Returns metrics reflect developmental stage biotech norms—with no profitability or positive cash flow generation recorded historically:

- Approximate Return on Equity for FY2025 stands near negative 189%, driven primarily by persistent net losses relative to equity base ($102.7 million equity vs $194 million net loss) [F1].

- Operating cash outflows ballooned above $123 million despite controlled capex just above $2.4 million indicating most spend directed at trial/study costs rather than asset buildup.

- Dividend payments or share repurchases are absent consistent with clinical-stage status reliant largely on dilutive funding rounds or debt-like royalty monetization instruments [S4][S18].

- Recent increases in royalty monetization liabilities (from roughly $59 million end-2024 up toward $191 million combined short/long-term liabilities by September 2025) hint at financing strategies tied directly to anticipated future royalty income streams but add balance sheet leverage complexities [S13][S18].

Regulatory & Legal Considerations

FDA has imposed multiple clinical holds affecting lead therapies developed through NAV platform utilization—highlighting regulatory sensitivity that may cascade into protracted review timelines or increased compliance burden [N7][N11]. Additionally litigation risks typical within biotech IP licensing environments exist but appear isolated with no material contingent liabilities referenced recently [S1][S7].

Summary

REGENXBIO exemplifies an innovative platform-centric gene therapy company confronting critical inflection points where promising technology meets harsh regulatory realities. The firm leverages collaborative licenses involving reputed pharmaceutical partners which partially mitigate product risk yet offer limited near-term profits amid expensive trial operations.

Near-term prospects hinge on resolving FDA concerns for MPS-targeted programs while maintaining sufficient liquidity through capital markets access or non-dilutive structures given shrinking cash reserves. Investors monitoring this space should prioritize upcoming pipeline data releases alongside partnership deal evolutions that signal durability both commercially and scientifically.

Disclaimer: This report is strictly for informational purposes reflecting current publicly available data as of early March 2026. It is not investment advice nor a recommendation regarding any securities mentioned herein.

Comments