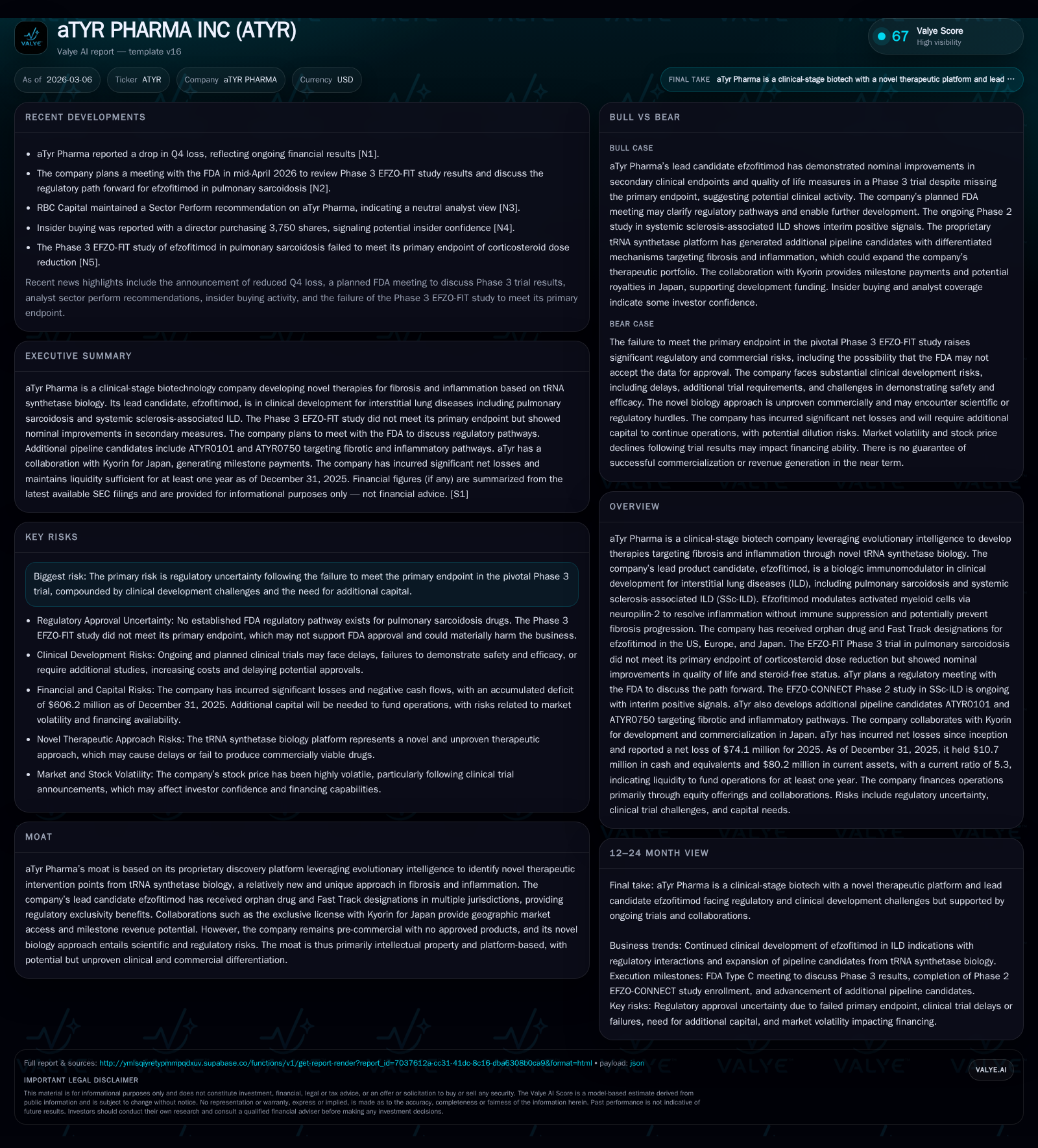

aTyr Pharma Faces Regulatory and Financial Challenges Following Phase 3 Trial Results

Clinical-stage biotech aTyr Pharma advances its novel tRNA synthetase biology platform but encounters setbacks with efzofitimod’s Phase 3 trial and ongoing capital demands.

aTyr Pharma Inc. is developing therapies targeting fibrosis and inflammation through a proprietary tRNA synthetase biology platform, focusing on interstitial lung diseases (ILD). Its lead candidate, efzofitimod, recently reported mixed Phase 3 results in pulmonary sarcoidosis, missing the primary corticosteroid reduction endpoint but showing nominal improvements in quality of life measures. The company remains pre-commercial, operating at sustained losses with limited cash reserves and a significant accumulated deficit. Future prospects depend on regulatory engagement outcomes, further clinical development, and capital raising efforts.

Company Overview

aTyr Pharma Inc. is a clinical-stage biotechnology company focused on developing treatments for fibrosis and inflammation by harnessing evolutionary intelligence applied to tRNA synthetase biology. This approach targets extracellular signaling domains evolved from tRNA synthetases to uncover novel therapeutic intervention points [S1].

Its lead product candidate, efzofitimod, is a biologic immunomodulator that selectively modulates activated myeloid cells through neuropilin-2 (NRP2), aiming to resolve inflammation in interstitial lung diseases (ILD) without broad immune suppression and potentially prevent fibrosis progression [S1].

Financial Performance

The company has incurred sustained losses typical of pre-commercial biotechs investing heavily in R&D. Operating income declined from -$46.4 million in 2022 to -$77.6 million in 2025, representing a 14.3% year-over-year deterioration. Net loss increased similarly to -$74.1 million in 2025 (-15.8% YoY). Operating cash flow remained negative though improved slightly to -$61.9 million compared with prior year [F1]. Capital expenditures were minimal at $77,000 in 2025 reflecting outsourcing focus.

Equity stood at approximately $67.5 million as of December 31, 2025, supported by recent equity raises primarily through an ATM program [F1][S13].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -74 | -62 | -78 | 0 | -15.8% |

| 2024 | -64 | -69 | -68 | 0 | -27.1% |

| 2023 | -50 | -33 | -55 | 4 | -11.1% |

| 2022 | -45 | -42 | -46 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -62 | -109.8 |

| 2024 | -69 | -91.4 |

| 2023 | -37 | -55.6 |

| 2022 | -44 | -63.4 |

Source: SEC companyfacts cache [F1].

Note: Figures rounded to nearest thousand USD.

Clinical Development Progress

aTyr’s clinical focus has been on efzofitimod for ILDs including pulmonary sarcoidosis and systemic sclerosis-associated ILD (SSc-ILD). The drug holds orphan drug designations and Fast Track status in the U.S., Europe and Japan [S1].

The EFZO-FIT Phase 3 trial evaluated two dosing regimens against placebo over 52 weeks in pulmonary sarcoidosis patients. The study did not meet its primary endpoint of statistically significant reduction in mean daily oral corticosteroid use at week 48 (p=0.3313 for the higher dose). However secondary endpoints showed nominal improvements in patient-reported outcomes such as the King’s Sarcoidosis Questionnaire lung domain (p=0.0479), fatigue scores (p=0.0226), and general health scores (p=0.0197). Lung function was maintained across groups [S1].

While these findings suggest biological activity consistent with the drug's mechanism of action, failure to meet the primary endpoint introduces regulatory uncertainty given no established FDA approval pathways for pulmonary sarcoidosis drugs [S2][N2]. A regulatory meeting is scheduled to discuss potential paths forward.

Market Positioning

aTyr’s unique platform targets previously unexplored extracellular signaling domains from tRNA synthetases offering a differentiated approach within fibrosis/inflammation therapeutics [S1]. Orphan drug designations provide exclusivity periods critical for small patient populations with high unmet medical need.

Partnership with Kyorin Pharmaceutical grants exclusive rights for efzofitimod development and commercialization in Japan along with milestone payments potential while mitigating direct commercialization risk there [S11][S13]. No commercial revenues have been generated yet.

Risks and Challenges

Key risks include:

- Regulatory uncertainty following failure of the pivotal trial's primary endpoint.

- Significant capital requirements amid limited liquidity.

- Dependence on contract manufacturing organizations posing operational risks.

- Exposure to complex healthcare compliance laws impacting future marketing.

- Challenges inherent to pioneering biologic therapies targeting novel mechanisms.

Outlook and Milestones

Future growth depends on:

- Outcomes from upcoming FDA meetings clarifying acceptable endpoints or trial designs.

- Expansion into other ILD indications or inflammatory/fibrotic diseases leveraging the platform.

- Strategic partnerships or licensing arrangements easing financial constraints.

- Demonstration of clinical differentiation translating into competitive positioning.

- Readiness for manufacturing scale-up aligned with commercialization plans.

No product sales revenues are currently reported; income arises mainly from collaboration milestones [F1][S11]. Regulatory approval remains prerequisite for commercial launch.

Capital Allocation and Return Metrics

aTyr’s capital allocation reflects typical early-stage biotech patterns with heavy R&D expense driving operating losses that increased year-over-year (-$77.6M OpInc in FY25 vs -$67.9M FY24) [F1]. No dividends or share repurchases occur given cash preservation needs.

Free cash flow remains deeply negative near -$62 million indicating ongoing dependency on financing events absent commercial inflows [F1]. Return on equity is highly negative (~-110%) reflecting accumulated deficits relative to shareholder equity [F1]. Minimal capex suggests reliance on outsourcing rather than internal asset buildout.

Conclusion

aTyr Pharma pursues a scientifically novel approach addressing ILDs through selective immunomodulation based on tRNA synthetase biology. Recent Phase 3 results present regulatory challenges despite encouraging secondary signals requiring further validation.

The firm faces typical pre-commercial biotech hurdles including sustained losses necessitating timely capital raises; uncertain regulatory pathways; reliance on external partners for manufacturing and market access; and risks associated with innovative therapeutic mechanisms.

Upcoming FDA interactions will be closely watched alongside clinical progress updates and capital management strategies determining operational runway sustainability.

This analysis integrates data from SEC filings [S1,S8,S11,S13,S14,S26] together with recent news reports [N1,N2], focusing strictly on verified information without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments