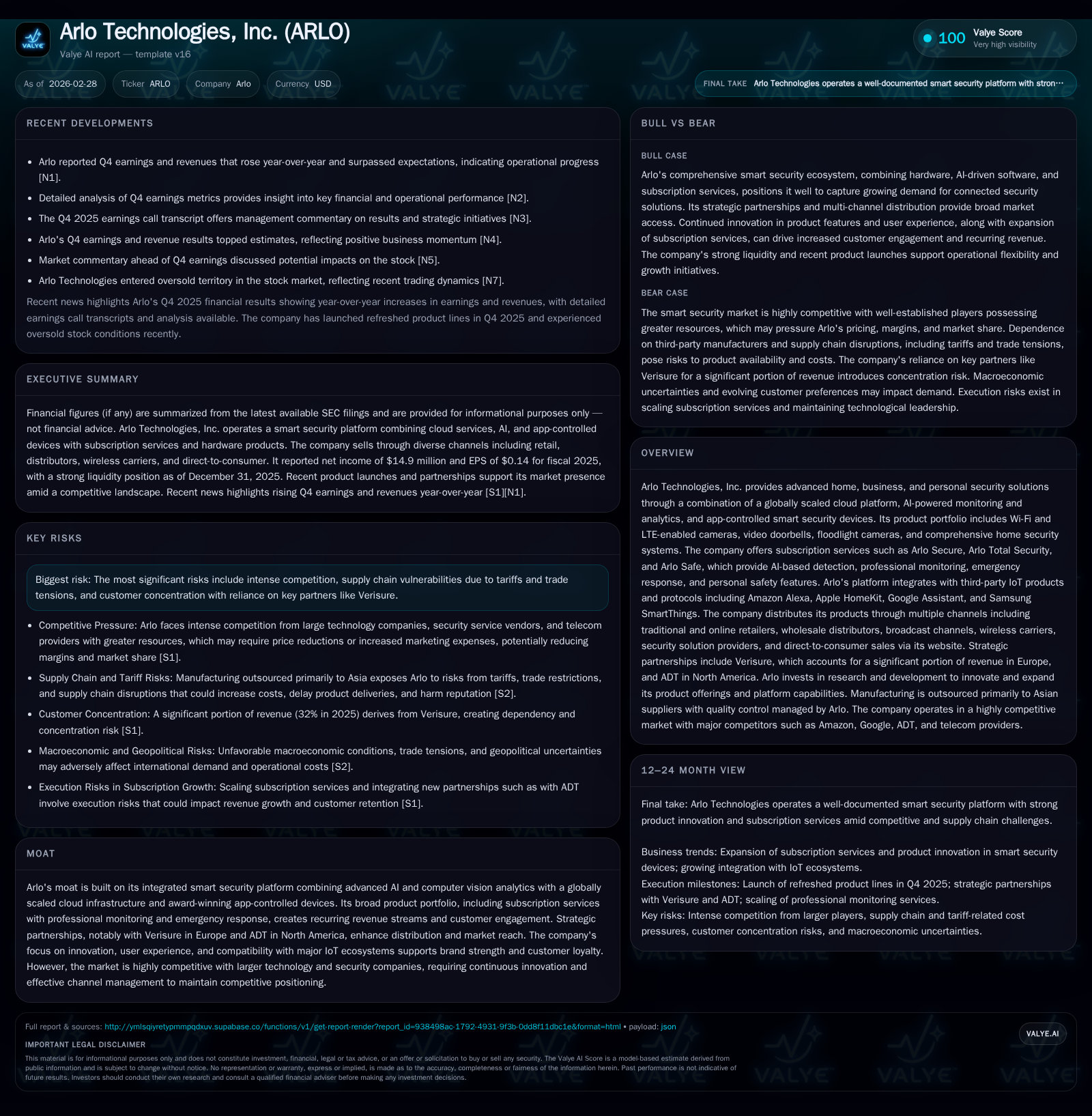

Arlo Technologies Escapes Past Losses with AI-Driven Security Platform and Strengthening Partnerships

The company's transition to profitability is underpinned by its integrated smart security ecosystem and expanding subscription services.

Arlo Technologies has reversed several years of operating losses, reporting positive operating and net income in 2025 supported by growing demand for its AI-powered smart security devices and subscription services. The firm benefits from strategic partnerships like Verisure and ADT, broad channel distribution, and a globally scaled cloud platform. Nonetheless, competitive pressures from large tech incumbents and evolving trade restrictions pose ongoing challenges. Investors should monitor the company’s ability to sustain growth in recurring revenues through service expansion and its progress in deepening user engagement across IoT ecosystems.

Historical Financial Performance

Arlo Technologies has experienced a notable financial turnaround entering the 2025 fiscal year. After consecutive years of operating losses peaking near -$57 million in 2022, the company swung to positive operating income of $6.1 million in 2025. Net income followed a similar trajectory, rising from a -$56.6 million loss in 2022 to nearly $15 million profit last year [F1]. This inflection reflects successful execution against competitive headwinds and structural shifts toward subscription revenue.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 15 | 79 | 6 | +148.9% | |

| 2024 | -31 | 51 | -35 | 3 | -38.4% |

| 2023 | -22 | 38 | -25 | 3 | +61.1% |

| 2022 | -57 | -46 | -57 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 46 | 11.7 | |

| 2024 | 4 | 49 | -30.2 |

| 2023 | 35 | -21.3 | |

| 2022 | -48 | -64.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not explicitly detailed in publicly available filings but growth trends are affirmed via earnings reports.

Drivers Behind Growth

The improvement stems from several operational advances detailed in Arlo’s latest annual report and quarterly disclosures. Product innovation continues at pace with the fourth-quarter launches of updated Essential series cameras featuring expanded fields of view and dual-band WiFi for connectivity robustness [S6]. The Pro series was refreshed with the Pro 6 models boasting improved battery endurance and an intuitive app interface.

Critically underpinning device sales is Arlo's focus on AI-powered monitoring via its subscription services — notably Arlo Secure providing unlimited camera coverage with customizable alerting leveraging advanced computer vision; Arlo Total Security extending professional monitoring anchored on its innovative multi-sensor home security system; and Arlo Safe which targets personal safety-mobile use cases with an emergency panic accessory [S13][S20].

These SaaS services provide recurring monthly revenue streams complementing upfront hardware sales. The integration across third-party ecosystems like Alexa and Google Assistant augments customer stickiness while increasing value proposition in the crowded IoT market [S6][S8].

Strategic Partnerships Bolster Distribution

Partnerships remain integral. Verisure’s exclusive European distribution business contributes roughly one-third of total revenues indicating strong market penetration there [S12]. Meanwhile the nascent alliance with ADT launched mid-2025 aims to amplify North American subscriptions through a digitally aligned partner offering no revenue contribution recorded yet but carrying significant growth potential given ADT’s customer scale [S12].

Distribution channels remain diversified: retail outlets including heavyweights such as Amazon and Best Buy coexist alongside wholesale distributors like Synnex plus wireless carriers like AT&T serving cellular product segments identified for expansion [S4][S11]. TV shopping networks HSN and QVC add niche access points.

Cash Flow Strength and Capital Deployment

Arlo’s operating cash flow jumped over half year-over-year to $78.7 million at year-end while capital expenditure remained subdued below $3 million indicating operational leverage benefits from scale without heavy fixed capex burden due to outsourced manufacturing predominantly in Asia [F1][S14]. Robust liquidity ($146 million cash) supports organic growth initiatives and financial stability while share repurchases rose markedly to nearly $46 million signaling management confidence after prior modest buyback levels [F1][S29].

Technology & Cloud Platform Advantage

Arlo emphasizes cloud-based architecture supporting AI analytics at scale with global data centers spanning North America, Europe (Ireland), Asia Pacific (Singapore), and Australia ensuring resilient uptime performance. This multiregional footprint enables reliable real-time video streaming and automation critical for emergency response features embedded within their Secure offerings [S5][S6].

Research & development investment remains substantial — spearheaded by roughly 186 engineers specializing across software algorithms to RF engineering fostering new product capabilities including wireless roaming LTE cameras tailored for remote site monitoring conjunctions popular for construction site security or wildlife observation [S14][S23].

Market Dynamics and Competitive Landscape

Arlo operates within an intensely competitive sector dominated by technologically resourceful giants: Amazon/Ring offers deep integration via Alexa plus consumer brand recognition; Google Nest similarly leverages vast AI R&D resources coupled with widespread Google ecosystem penetration; telecom operators bundle smart security with communication services while specialist providers like ADT carve niche professional segments offering onsite response services [S7][S12].

This pressure mandates ongoing investment in feature-rich hardware differentiation combined with advanced AI-driven subscriptions fostering customer loyalty via superior detection analytics or emergency response response time improvements reducing false alerts.

Risks Related to Supply Chain & Trade Environment

Manufacturing outsourcing predominantly across Vietnam, Thailand and Indonesia exposes Arlo to tariff impositions reflective of US-China trade tensions cited as inflating production costs potentially pressuring product margins if cost absorption is untenable or price increases impair customer demand [S9][S15][S28].

Uncertain trade policies heighten supply chain risk including delays or component scarcity which may impinge delivery timelines causing reputational damage indirectly impacting retail partner trust and end-customer satisfaction.

What To Watch Going Forward (Analysis)

Absent formal guidance disclosures post-earnings releases at this date , key milestones include subscriber account growth rates on flagship Arlo Secure platforms which will validate ongoing SaaS monetization effectiveness. Incremental revenue contributions from the recently inked ADT partnership merit close scrutiny through quarterly updates as execution progresses.

Continued refinement of device hardware along with possible expansion into non-camera IoT categories could unlock adjacent market white spaces needing confirmation.

Moreover consistent margin expansion reflecting operational leverage harnessed from fixed-cost absorption improvements or supply chain optimization could support sustained profitability beyond flattered cyclical gains.

Capital Returns & Financial Health Summary

Arlo's return on equity approximated at roughly 11.7% reflects a positive transition phase fueled by net earnings recovery versus lower equity bases from recent accumulated deficit drawdowns [F1]. Strong free cash flow generation estimated near $76 million after capex validates operational strength allowing continued shareholder-friendly capital allocation balanced between buybacks reaching almost $46 million last fiscal year while maintaining sizable cash buffers.

In absence of dividend payments outlined in filings or press releases suggests strategy remains focused on reinvestment plus share repurchase programs enhancing per-share metrics rather than yield generation currently.[F1][S29]

Conclusion

Arlo Technologies exemplifies an emerging leader reshaping its trajectory by embedding cutting-edge AI into smart security solutions distributed via multi-channel strategies fortified by strategic alliances globally. The pivot from protracted losses toward solid profitability underscores its platform approach blending hardware excellence with differentiated subscription services propelling recurring revenues.

Nonetheless risks emanate chiefly from fierce competition among giant tech incumbents wielding deeper pockets alongside tariff-driven supply chain volatility warranting vigilance.

Success will hinge on sustaining innovation cadence within hardware/software integration realms while capitalizing on partnership synergies especially tied to safety monitoring via professional networks.

This analysis is grounded exclusively on SEC filings dated no later than February 27th, 2026 ([F1], [S#]) augmented by contemporaneous news events ([N#]). It should not be construed as investment advice or an endorsement of any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments