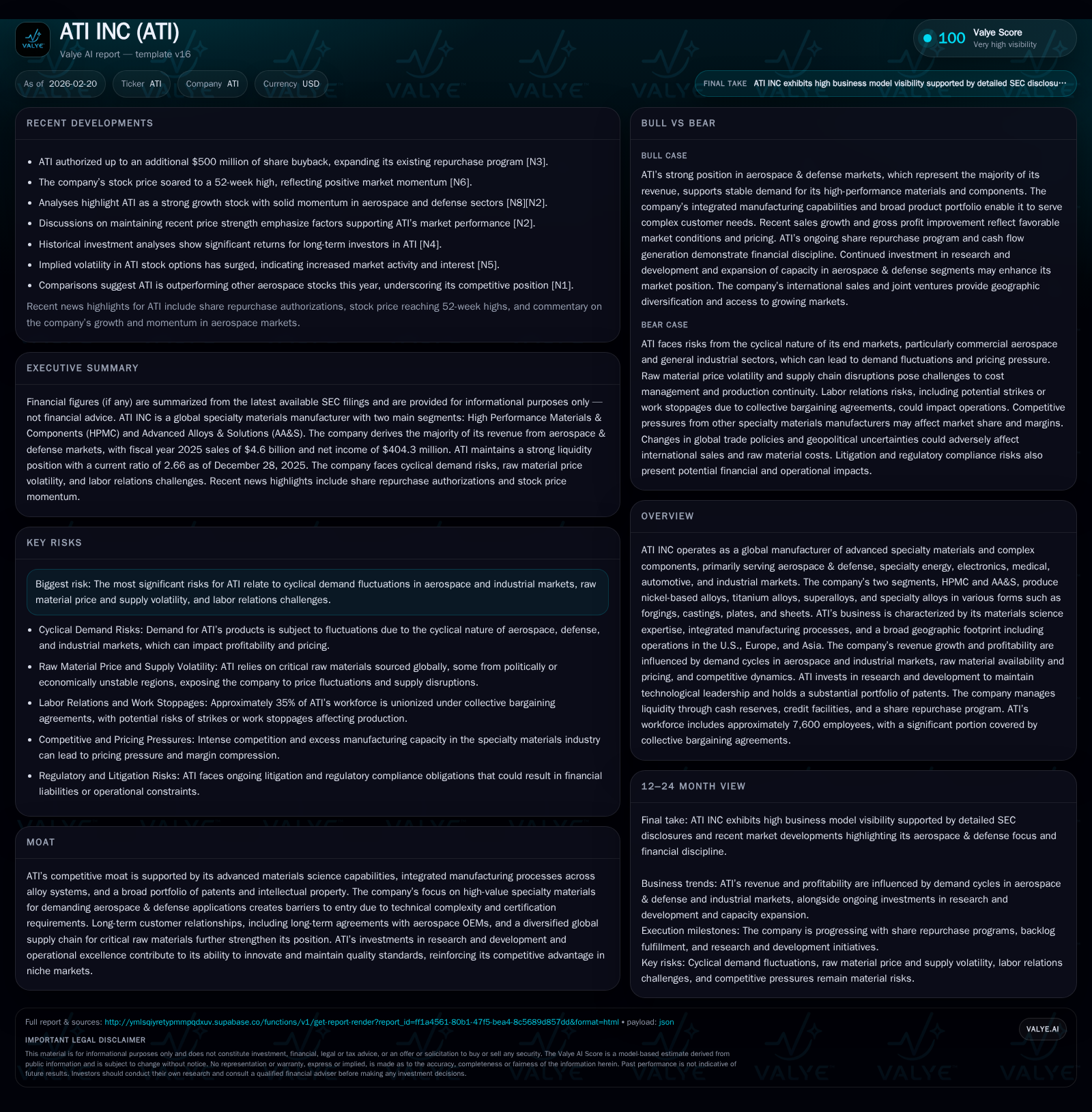

ATI INC's Aerospace-Driven Growth and Capital Deployment Amid Raw Material Volatility

ATI leverages specialty materials expertise to expand aerospace market share while navigating supply chain and labor challenges.

ATI INC delivered solid financial performance in fiscal 2025, with revenue growth driven primarily by aerospace & defense markets and improved gross margins supported by favorable sales mix. The company’s integrated manufacturing and advanced materials science capabilities underpin its competitive moat, especially in jet engine components. Looking ahead, growth is expected to stem from continued aerospace demand, defense sector expansion, and strategic capacity investments, although raw material price volatility and labor relations remain key risks. ATI’s disciplined capital allocation includes substantial share buybacks enabled by strong cash flow generation and a manageable debt profile.

Company Overview and Competitive Positioning

ATI Inc. stands out as a global leader in advanced specialty materials and complex components primarily targeting demanding aerospace & defense sectors alongside specialty energy, electronics, medical, automotive, and industrial markets [S1][S7]. Its business is organized into two segments: High Performance Materials & Components (HPMC), which specializes in precision forgings, castings and additive manufactured parts mainly serving commercial jet engines; and Advanced Alloys & Solutions (AA&S), producing nickel-based alloys, titanium alloys, flat plates and sheets for aerospace as well as broader industrial applications [S7][S11].

ATI's moat is anchored by its vertically integrated manufacturing processes across multiple alloy systems—from melting to machining—coupled with substantial R&D investments that have yielded hundreds of patents protecting its technological edge . Commercial jet engine products constitute approximately 68% of HPMC sales highlighting ATI’s entrenched customer relationships within OEM aerospace supply chains that require extensive certification and quality validation. The company's broad geographic footprint spans U.S., Europe and Asia including a majority interest in the STAL joint venture in China enhancing market access [S17][S14].

Historical Financial Performance

The company posted steady top-line expansion with revenues increasing from $4.17 billion in FY2023 to $4.36 billion in FY2024 (+4.6%), followed by a further gain to $4.59 billion in FY2025 (+5%) as aerospace markets strengthened post-pandemic recovery phases (see Table 1). Operating income similarly advanced from roughly $108 million in FY2023 (impacted by COVID-related disruptions) to nearly $609 million in FY2024 then $641 million in FY2025 (+105% over two years) reflecting margin recovery through pricing power on nickel-based superalloys and higher volumes principally in the HPMC segment focused on commercial jet engines [F1][S8][S17].

Net income exhibited comparable improvement growing from $146 million in FY2023 to $368 million in FY2024 then reaching $404 million in FY2025 (+177% over two years). This performance supported a strong return on equity approximating 22.4% in the most recent reporting period based on net income relative to reported equity [F1]. Operating cash flow surged from just $86 million in FY2023 to over $407 million in FY2024 then climbed further to $614 million by year-end 2025 (+615% over two years), driven by improved earnings quality and efficient working capital management despite inventory build-ups aligned with production ramp-ups targeting aerospace OEM demand [F1][S22]. Capital expenditures rose progressively each year from approximately $131 million in FY2022 to nearly $240 million for capacity enhancements prior to rising again to almost $281 million invested during FY2025 focusing on expanding aircraft materials capacity reflective of ATI’s growth strategy emphasizing aerospace materials leadership [F1][S21].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 404 | 614 | 641 | 281 | +9.9% |

| 2024 | 368 | 407 | 609 | 239 | +152.4% |

| 2023 | 146 | 86 | 108 | 201 | +11.3% |

| 2022 | 131 | 225 | 287 | 131 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 470 | 334 | 22.4 |

| 2024 | 260 | 168 | 19.9 |

| 2023 | 85 | -115 | 10.6 |

| 2022 | 140 | 94 | 12.5 |

Source: SEC companyfacts cache [F1].

Note: Buybacks shown where data available; Dividends not included due to insufficient recent data.

Growth Drivers and Future Outlook

Revenue growth continues to be propelled predominantly by strengthening demand for commercial jet engine components within HPMC, accounting for nearly three quarters of segment revenue combined with sturdy expansion of defense-related products which grew around 24% year-over-year recently [S17][N14]. AA&S’s growth is underpinned by its push into high-value titanium mill products gaining traction amid aerospace & defense expansions plus resilient orders linked to energy sectors despite softness elsewhere such as medical devices or conventional energy headwinds [S8][N14].

ATI emphasizes strategic capital deployment targeting capacity expansions tailored for the aerospace supply chain where long lead times prevail due to intricate certification processes required for nickel-based superalloys and titanium alloys fabrication at scale—a notable rationalization given the complexity of thermal fatigue resistance required for turbine engines [analysis: niche metallurgy specialization creates high barriers]. R&D outlays sustained above $20 million annually support proprietary alloy development alongside additive manufacturing methods that improve yield and reduce scrap rates while broadening product applicability particularly for emerging electric flight opportunities or hypersonic defense applications contingent on thermal stability enhancements [S13].

Going forward, ATI projects adjusted EPS guidance well above consensus estimates signaling confidence rooted in backlog strength backed by long-term agreements with OEMs emphasizing supply security amidst ongoing geopolitical tensions affecting raw material sourcing [N14][N4]. However, raw material price volatility particularly nickel (sourced mainly from Canada, Norway, Japan), titanium sponge (China, Japan), cobalt (Norway) introduces procurement cost pressures that could compress margins if not offset timely via customer pricing or operational efficiencies [S19]. Labor relations pose additional risk given about one-third workforce unionized predominantly under USW collective bargaining agreements expiring at staggered intervals; recent six-year contracts covering ~1,000 union employees mitigate immediate strike risk but remain an area warranting careful management due to concentration among skilled metallurgical workers critical for quality consistency [S2].

On geographic diversification, multinational presence including the majority-owned STAL joint venture positions ATI favorably within Asian markets while maintaining dominant U.S./European footprint reflective of concentrated aerospace production hubs despite currency translation exposures that account for meaningful earnings variability over time [S24][analysis: aviation global supply chains necessitate multi-region manufacturing spread enabling resilience].

Capital Allocation and Financial Health

In fiscal year 2025 ATI allocated significant free cash flow toward shareholder returns repurchasing shares amounting to $470 million following incremental authorization for an additional $500 million buyback program validated by improved liquidity buffers totaling around $1.1 billion available including cash balances near $417 million and undrawn revolving credit facilities up to $600 million backed by accounts receivable and inventory collateralization frameworks established recently through extended Asset Based Lending amendments through June 2030 [N5][S18][S20].

Debt metrics reflect prudent deleveraging evidenced by a net debt to Adjusted EBITDA ratio improving from approximately 1.63x at year-end prior period to near 1.56x latest period driven by higher EBITDA coupled with redemption of convertible debentures thereby reducing interest burdens slightly despite incremental term loans permitted under credit facility amendments priced at SOFR plus spreads hovering near mid-single digits annualized rates [F1][S10][S15]. Pension funding obligations remain manageable albeit closely monitored given ~2,000 participants under qualified defined benefit plans entailing modest contribution requirements forecast around $4 million this year plus long-term expected payments totaling ~$40 million over coming decade assuming actuarial assumptions hold steady [S18]. Capital expenditure commitments approach levels exceeding recent years fueled by planned aerospace capacity growth initiatives requiring careful cash flow oversight.

Profitability advances rely on continuous margin enhancement strategies involving favorable product mix shifts toward higher value nickel-based alloys commanding premium pricing power offsetting inflationary raw material cost headwinds less fully passed through due to contractual arrangements extending years before resets can occur wholesale across tiers within complex supply ecosystems characteristic of aerospace manufacturing cycles lasting multiple quarters before visibility stabilizes fully for volume planning purposes resulting often in working capital timing variability linked closely with inventory turns deteriorated modestly year-over-year amid volume ramp considerations [F1][S22][S28].

Sector Context

Given the specialty materials sector’s cyclical nature tied heavily to macroeconomic swings influencing airlines’ capital spending patterns or defense budget appropriations subject also to geopolitical developments affecting supply chain reliability ATI's focus on high-technology alloy niche markets grants insulation against commodity substitutes but entails exposure nonetheless given global competitive pressures from major players such as Berkshire Hathaway’s Precision Castparts Corporation along with Howmet Aerospace increasing titanium focus challenging certain product lines alongside European specialists such as VDM Metals GmbH for flat rolled alloys creating an evolving competitive dynamic necessitating constant innovation .

Risk Factors Summary

Critical risks include:

- Cyclicality inherent in aerospace/industrial end-markets causing periodic demand fluctuations impacting utilization rates;

- Frequent raw material availability disruption risks stemming from political-economic instability across supplier countries leading doping costs;

- Labor unrest potential derived from collective bargaining agreement cycles covering skilled production employees necessary for maintaining precision manufacturing standards;

- Legal contingencies ranging from environmental remediation obligations estimated around $15 million reserved yet potentially scalable depending on regulatory developments;

- Currency volatility impacting foreign subsidiary earnings translation complicating profit consistency targets.

Conclusion

ATI’s strong operational execution anchored by differentiated materials science capabilities fuels consistent growth trajectory largely insulated by specialized end-market focuses such as commercial jet engines within HPMC complemented by diversified AA&S platforms servicing broader industrial verticals. Capital strength characterized by robust operating cash flows allocates effectively toward capacity builds supporting long-term market share gains together with generous shareholder return programs complemented by judicious balance sheet management positioning ATI well relative to sector cyclicality challenges albeit mindful vigilance remains warranted regarding raw material sourcing complexities and workforce dialogue dynamics.

This analysis relies solely on publicly available information obtained through official filings and news sources as cited; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments