Binah Capital Group Harnesses Hybrid Model for Advisor-Centric Wealth Management Growth

Binah Capital Group’s flexible advisor operating models and technological integration underpin its recent financial turnaround and set the stage for scalable expansion.

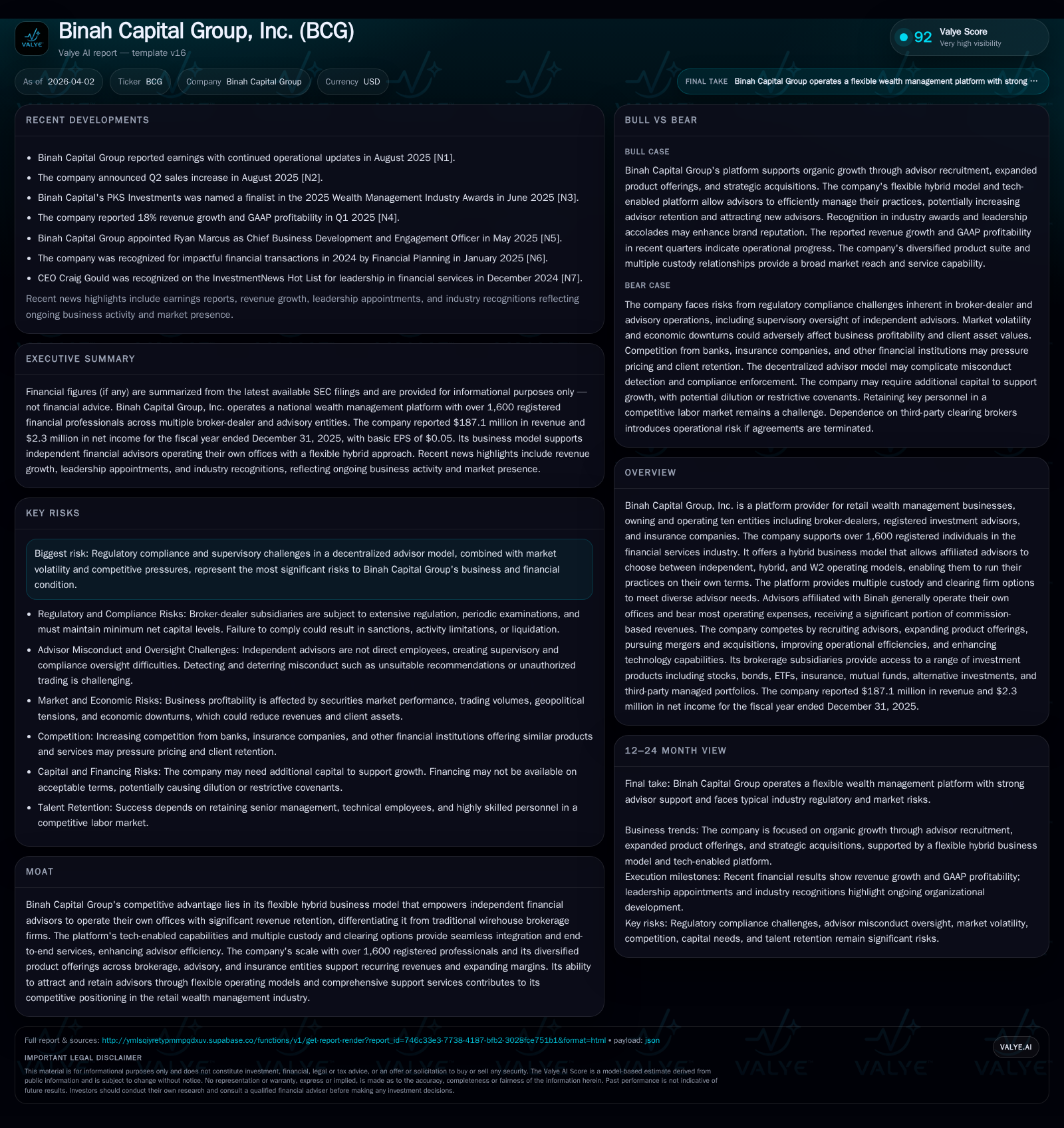

Binah Capital Group operates a unique retail wealth management platform that blends independent and corporate advisor business models. In 2025, the company demonstrated notable revenue growth of 10.8% and swung from a net loss to profitability, driven primarily by its hybrid model empowering advisors with autonomy and multiple custody options. Its capital allocation strategy prioritizes organic growth and operational efficiency, with positive cash flow generation signaling improving financial health. Key challenges include navigating regulatory complexities intrinsic to decentralized supervision and competitive pressures from larger banking and insurance firms. Future growth hinges on continued advisor recruitment, targeted acquisitions, technology enhancements, and regulatory adaptation.

From Commission-Based Roots to Hybrid Flexibility: Binah’s Growth Trajectory

Binah Capital Group has carved out a distinctive niche within retail wealth management by cultivating a platform that champions advisor autonomy combined with network scale efficiencies. This model departs from conventional wirehouse brokerage firms where advisors often face reduced revenue retention and limited operational independence.

Financially, Binah's move toward a hybrid platform has coincided with tangible top-line improvements as evidenced in its fiscal year 2025 results. The company's revenue increased by 10.8% year-over-year to $187.1 million [F1], reflecting broader advisor productivity gains and expanded product penetration across brokerage, advisory, and insurance entities under its umbrella. Meanwhile, net income transitioned positively from a loss of $5.29 million in 2024 to a net gain of $2.31 million in 2025 [F1]. The swing underscores not just top-line growth but also margin enhancements driven by operational leverage inherent in Binah’s model.

This historical performance pivot correlates directly with the structural shift toward empowering over 1,600 registered financial advisors operating mostly autonomous offices responsible for their own expenses yet retained a substantial share of their commission revenues . The resulting dynamic fosters entrepreneurial incentives that stimulate advisor recruitment and retention while sustaining fee-based asset management revenue streams.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 187 | 2 | 5 | 61000 | +10.8% | +143.6% |

| 2024 | 169 | -5 | -1 | 85000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 5 | 12.6 |

| 2024 | -1 | -32.7 |

Source: SEC companyfacts cache [F1].

Organic growth fueled by commissions retention under the hybrid model contributed materially to the earnings turnaround.

Decoding Binah’s Platform: How Advisor Autonomy Drives Competitive Differentiation

Central to Binah’s moat is its hybrid operating model that allows affiliated advisors to select from independent contractor roles, hybrid arrangements where some infrastructure is shared, or W2 employee relationships within the Purshe Kaplan Sterling entities [S4]. This flexibility powers personalized practice structuring which is rare among large wirehouses predominantly favoring full employee models.

From a sector perspective, this blend aligns closely with trends where "lift-out acquisitions" facilitate rapid scale by onboarding advisor teams seeking less restrictive environments while preserving brand identity [S4]. Advisors appreciate access to multiple clearing firms rather than single-provider custody arrangements common among traditional firms — this open architecture supports tailored client service frameworks as well as compliance segmentation.

Moreover, Binah’s tech-enabled platform ensures advisors enjoy seamless integration of back-office functions — compliance surveillance, trade execution access via major custodians, portfolio analytics — all contributing to higher operational efficiency without sacrificing independence [S4]. This shared services model spreads fixed costs across subsidiaries enhancing margin scalability.

Competitive benchmarking underscores Binah’s advantage lies not simply in technology adoption but rather in how these tools integrate within hybrid business lines offering diverse revenue sources like mutual funds commissions, advisory fees, insurance commissions and alternative investments distributions [S21]. Such diversification reduces dependence on pure brokerage commissions vulnerable to market cyclicality.

Revenue and Profitability Trends: A Look at Binah’s Financial Performance in 2025

The fiscal year ending December 31, 2025 marked a critical inflection point for Binah Capital Group’s financials enabled by faster advisor onboarding and tighter expense management [F1]. Revenue rose sharply by more than one-tenth reaching $187 million — reflecting firm-wide increases across brokerage commissions as well as asset-based advisory revenues tied to growing fee-based models [F1].

Net income benefits were equally pronounced moving from a negative $5.3 million in the prior year into positive territory at approximately $2.3 million — an impressive margin improvement against prior losses suggesting better operational discipline or pricing leverage [F1]. The company’s approximate return on equity was about 12.6%, signaling rising capital efficiency for stakeholders despite still modest absolute earnings scale [F1].

Operating cash flow dynamics further highlight improving business quality; CFO climbed nearly tenfold year-on-year surging from -$0.62 million in 2024 to +$5.15 million in 2025 while capital expenditures were trimmed by roughly a quarter down to $61 thousand annually [F1]. This operating cash flow strength provides internal runway for reinvestment without reliance on external financing or equity dilution [F1].

Such trends are consistent with scaled shared services benefiting from increased advisor count alongside software-enabled front-to-back office integration reducing per-advisor deployment costs [S4].

Strategic Expansion Pathways: Recruitment, Acquisitions, and Technology Enhancements

Binah plans future growth anchored on expanding its advisory force further via intensified recruiting initiatives fueled by the lure of its hybrid operating model providing autonomy rarely found elsewhere [S4]. Lift-out acquisitions remain core strategic levers to consolidate smaller broker-dealers onto Binah’s platform rapidly capturing accretive economy-of-scale benefits.

Further broadening product offerings beyond traditional securities into insurance products and alternative investments seeks cross-selling synergies enhancing wallet share per client relationship [S4]. Investments in tech stack sophistication continue including mobile access enhancements, customer-facing digital portals, portfolio modeling tools — imperative given competitive pressures from banks integrating robo-advisory capabilities alongside human advisors.

Industry realities reveal increasing overlap between wealth management services traditionally offered separately by banks or insurance groups placing pressure on standalone brokerage firms like Binah [S4]. However, the company's ability to cater flexibly through multiple RIA structures along with choice of custody solutions differentiates it amidst these crowded channels.

Navigating Regulatory Complexities in a Decentralized Advisor Network

Operating within a largely independent contractor framework generates inherent regulatory supervision challenges [S5][S7]. Broker-dealer subsidiaries must comply stringently with SEC, FINRA rules around sales practices, anti-fraud controls and net capital maintenance often complicated by dispersed advisor offices each responsible for separate compliance adherence.

Moreover, potential reclassification risks exist if regulators interpret advisors more strictly as employees under labor laws — imposing higher overhead costs due to benefits provision or payroll taxes [S9][S27]. Data privacy regulations impose further complexity particularly when proprietary technology platforms incorporate sensitive customer information; mandatory disclosures of software details risk diluting competitive edge should regulators demand transparency [S5].

Binah's adoption of captive insurance subsidiaries aims to self-insure certain liabilities mitigating external premiums though indemnity limits remain uncertain thus exposure exists [S7][S16]. Adequate internal controls for surveillance of misconduct such as unsuitable recommendations or unauthorized transactions remains paramount given agility in decentralized monitoring is challenged by geographic dispersion.

Capital Structure and Returns: Evaluating Binah’s ROE, Cash Flows, and Shareholder Rewards

At December 31, 2025 Binah held total equity capital near $18.3 million up modestly from $16.2 million at prior fiscal year-end denoting retained earnings accumulation driven by profitable operations during the period [F1]. The firm produced approximately $5.1 million free cash flow after accounting for minimal capital expenditures highlighting strong operational cash conversion supporting ongoing investment needs internally without need for equity raises at present levels [F1],[S6],[S8].

Importantly no dividends or share repurchase programs were disclosed consistent with typical capital allocation patterns observed among growth-stage wealth management platforms prioritizing reinvestment over distributions [F1],[S6],[S8]. The company maintains convertible preferred stock classes indicating layered funding mechanisms but no material leverage burdens aside from moderate notes payable disclosed preventing undue interest strain on operating cash flows [S6],[S8],[S11],[S14].

ROE of about 12.6% underscores effective use of equity capital returning value amid improving profitability metrics supporting further potential internal accumulation provided sustained growth trajectories persist [F1].

Outlook and Milestones to Watch: Opportunities and Constraints Ahead

While explicit quantitative guidance is absent from filings or disclosures presently [N#]/[S#], thematic indicators provide lenses on expectations.

Significant near-term milestones include ramping up advisor headcount beyond current ~1,600 professionals leveraging continued recruitment programs emphasizing autonomy coupled with scaling acquisitions funneling complementary broker-dealer teams onto Binah’s platform infrastructure [S4],. Monitoring integration efficiency post-acquisition will be key as lift-out acquisitions often hold execution risk despite clear economies-of-scale potential.

Technology rollout benchmarks such as expanded custody partnerships availability along with next-generation digital client servicing tools also prove pivotal given evolving customer expectations shaped by fintech advances across wealth segments [S4]. On risk factors side evolving regulatory frameworks especially any reinterpretations affecting advisor classification or data privacy compliance could curtail expansion momentum through increased compliance costs or forced tech disclosures adversely impacting competitive positioning [S5],[S7],.

Competitive pressures remain elevated as traditional wirehouses defend legacy assets while fintech disruptors encroach through robo-advisor offerings; however Binah's hybrid flexibility paired with diversified product suite offers durable differentiation if sustained investment continues.

Disclaimer: This analysis is based solely on publicly available information as of April 2026 including SEC filings (Forms 10-K/Q/8-K), company disclosures and companyfacts snapshot data points referenced without subjective forward-looking estimates beyond stated qualitative commentary.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments