Beachbody Company’s Q1 Strength Highlights Subscription and Product Synergies

Strong Q1 operational results combined with a refined credit agreement underscore Beachbody’s multi-channel growth potential amid sector competition.

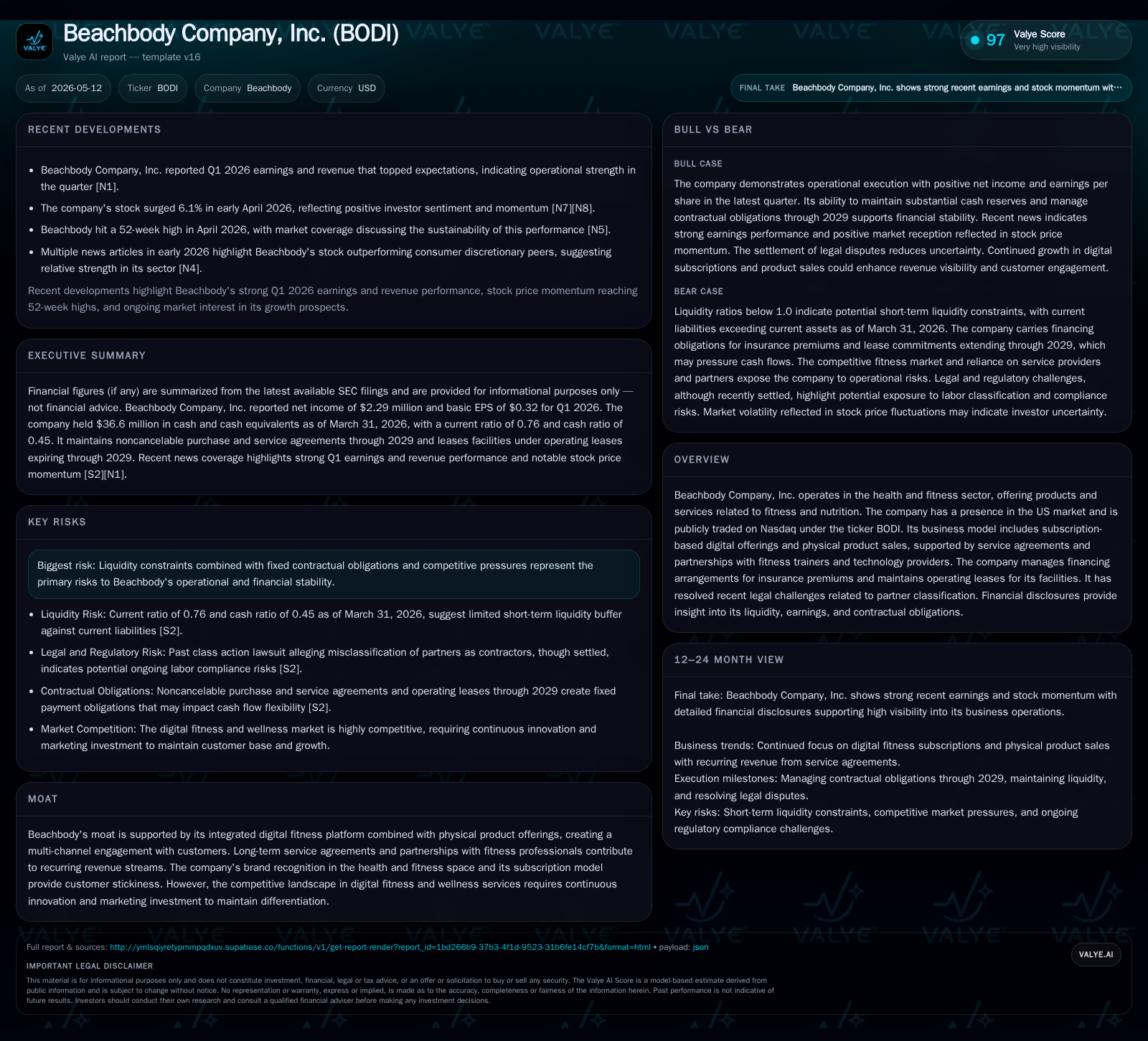

Beachbody Company, Inc. reported a Q1 revenue and earnings beat in its May 2026 10-Q, reinforcing the resilience of its integrated subscription-based fitness streaming platform alongside physical nutrition product sales. An amended asset-based lending facility (ABL) credit agreement improves near-term liquidity guardrails while easing digital subscription targets, enabling strategic focus on growth execution and covenant compliance. The company’s multi-channel business model, underpinned by long-term trainer partnerships and a subscription ecosystem, positions it well within a competitive but fragmented digital fitness market. Key risks include liquidity pressures, inventory valuation adjustments, and the need for ongoing innovation amidst intense competition. Upcoming milestones include monitoring subscriber metrics against amended covenant floors and managing debt amortization starting mid-2026.

Latest Quarterly Update: Operating Metrics and Credit Facility Amendments

Beachbody Company’s latest quarterly filing (10-Q dated May 12, 2026) reveals operational strength with revenue and adjusted earnings surpassing analyst expectations reported simultaneously in earnings announcements [N1], [S2]. The enhanced Q1 performance is supported by continued subscriber additions on the Beachbody On Demand Interactive (BODi) platform coupled with stable ongoing sales of weight management and nutritional supplements such as Shakeology shakes.

Inventory write-downs of $0.6 million recorded during the quarter highlight modest challenges in product demand forecasting or supply chain functioning but are not yet material to gross margin trajectory [S2]. Notably, the company finalized an amendment to its Asset-Based Lending (ABL) Facility credit agreement that increased minimum liquidity requirements from $12 million to $15 million while simultaneously reducing monthly digital subscription floor targets from 850,000 to 700,000 subscribers [S7]. These amendments provide enhanced flexibility around financial covenants that were at risk previously due to tightening operating conditions.

Amortization of the loan principal will commence July 1, 2026 at roughly $177k monthly installments extending through maturity in May 2028 unless extended by lender consent. This gradual amortization schedule allows near-term liquidity preservation while managing long-term leverage exposure [S2].

Beachbody’s Multi-Channel Business Model: Digital Subscriptions and Physical Products

Beachbody generates revenues primarily through a hybrid model comprising subscription access fees paid by consumers for streaming guided workout programs on BODi across multiple platforms—including web browsers, iOS/Android apps, and Roku devices—and direct sales of physical nutrition supplements and products in categories like weight management performance nutrition [S1], [S2]. Revenue flow is supplemented by royalties paid to fitness trainers whose branded programs are hosted on BODi; these royalties represent variable compensation dependent on downstream consumption and are accounted as cost of revenue.

This dual-channel approach promotes deeper user engagement by combining motivational content with tangible product solutions aimed at customers’ health goals. Long-term contractual service agreements with top-tier trainers create recurring revenue streams and support customer retention within the ecosystem. Switching costs arise partly from personalized program progress tracking within BODi and investment in consumption patterns of specific supplement regimens.

Moreover, Beachbody’s past pivot away from a multi-level marketing structure towards a single-level affiliate distribution model simplified partner relationships enhancing clarity around royalties while preserving network effects in social media-driven direct response advertising channels—a key driver of Customer Acquisition Cost efficiency and brand virality [S1].

Competitive Positioning within the Health and Fitness Sector

Beachbody operates in an intensely competitive landscape characterized by rapid innovation cycles among streaming fitness providers such as Peloton Digital, Mirror (acquired by Lululemon), Daily Burn (owned by IAC), alongside boutique app startups delivering niche wellness experiences. The physical nutrition supplement market further introduces competition from established brands like Herbalife alongside direct-to-consumer newcomers leveraging influencer marketing.

Beachbody enjoys moat advantages derived from its integrated service-product delivery model providing unified consumer journeys that competitors offering solely digital or physical products cannot easily replicate at scale without significant ecosystem build-out cost.

Brand recognition cultivated over years through high-profile fitness programs (e.g., "P90X," "21 Day Fix") confers pricing power yet demands continuous content refreshment alongside investments in AI-guided customization features within BODi's platform—features increasingly important for differentiation. Supply chain reliability for physical products further differentiates dependable fulfillment timelines amidst industry-wide raw material inflation challenges.

Nevertheless, market fragmentation compels constant marketing expense as retaining share among digitally savvy consumers sensitive to app experience quality and new workout trends remains challenging [S1], [S2].

Growth Drivers: Subscription Scale, Trainer Partnerships, and Innovation

Key growth levers center around scaling subscriber counts sustainably within adjusted covenant thresholds post-amendment (monthly targets reduced to 700k with conditional testing), deepening trainer partnership economics via royalties structured as growth incentives linked directly to sales uplift of their branded content/products.

Pipeline enhancements emphasize improved UI/UX integration on BODi including personalized content algorithms incorporating wearables data feeds potentially increasing session frequency and average revenue per user (ARPU). Expansion plans into adjacent categories such as mental wellness or recovery-focused programming may widen addressable markets. Additionally, geographic extension beyond core US markets remains an untapped avenue contingent on localizing content language/cultural fit.

Promoting cross-selling between digital subscriptions and physical supplements bolsters average customer lifetime value (LTV) while optimizing fulfillment economies of scale reduces per-unit distribution cost impacting gross margins favorably when volume ramps.

Risks and Headwinds: Liquidity Constraints, Competitive Pressures, and Inventory Write-downs

Despite recent covenant relief achieved via amended credit terms allowing more realistic subscriber floors conditional on cash buffer thresholds exceeding debt principal by $4.6m ($15m minimum liquidity), working capital pressure persists as reflected in suboptimal current ratio of approximately 0.76 suggests tight operational liquidity management is necessary [F1], [S7].

Inventory valuation adjustments totaling $0.6 million in Q1 signal potential inefficiencies either in demand forecasting accuracy or supply chain bottlenecks which can impair future margins if prolonged or amplified through channel destocking.

Technology platform roadmap progress including new feature rollouts or third-party integrations influencing engagement depth should be watched for scaling user stickiness key to reducing churn long-term.

Potential geographic expansions outside the US—if scoped publicly—would introduce new competitive landscapes requiring capital allocation discipline balancing near-term margin dilution versus incremental top-line contribution tradeoffs.

Financial Overview: Liquidity, Debt Maturity, and Earnings Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $37mm | |

| 2026-03-31 | ||

| Total debt | $25mm | |

| 2026-03-31 | ||

| Net debt | $-12mm | |

| 2026-03-31 | ||

| Current assets | $62mm | |

| 2026-03-31 | ||

| Current liabilities | $81mm | |

| 2026-03-31 | ||

| Current ratio | 0.76x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Beachbody closed Q1 with cash & equivalents totaling approximately $36.59 million against $25 million total debt outstanding under its ABL Facility yielding a net cash position near $11.59 million as of March 31, 2026 [F1], [S2].

The ABL Facility carries an effective interest rate averaging nearly 14.8% for Q1 due mainly to embedded floors on SOFR plus premium spreads—subject to step-downs contingent on improved FCCR compliance before year-end maturities reported via filings [S2]. Principal repayment deferrals until July 2026 allow near-term financial flexibility though amortization at ~$177k/month thereafter will require steady cash flow generation alignment.

Operating income remained positive in trailing periods albeit challenged by volatility in warrant liability fair value adjustments tied directly to common stock price movements adding non-cash swings below operating profit lines.

Current liabilities exceed current assets resulting in a current ratio below unity reflecting working capital deficits requiring close management focus [F1].

This analysis is based solely on publicly available SEC filings dated through May 12, 2026,and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments