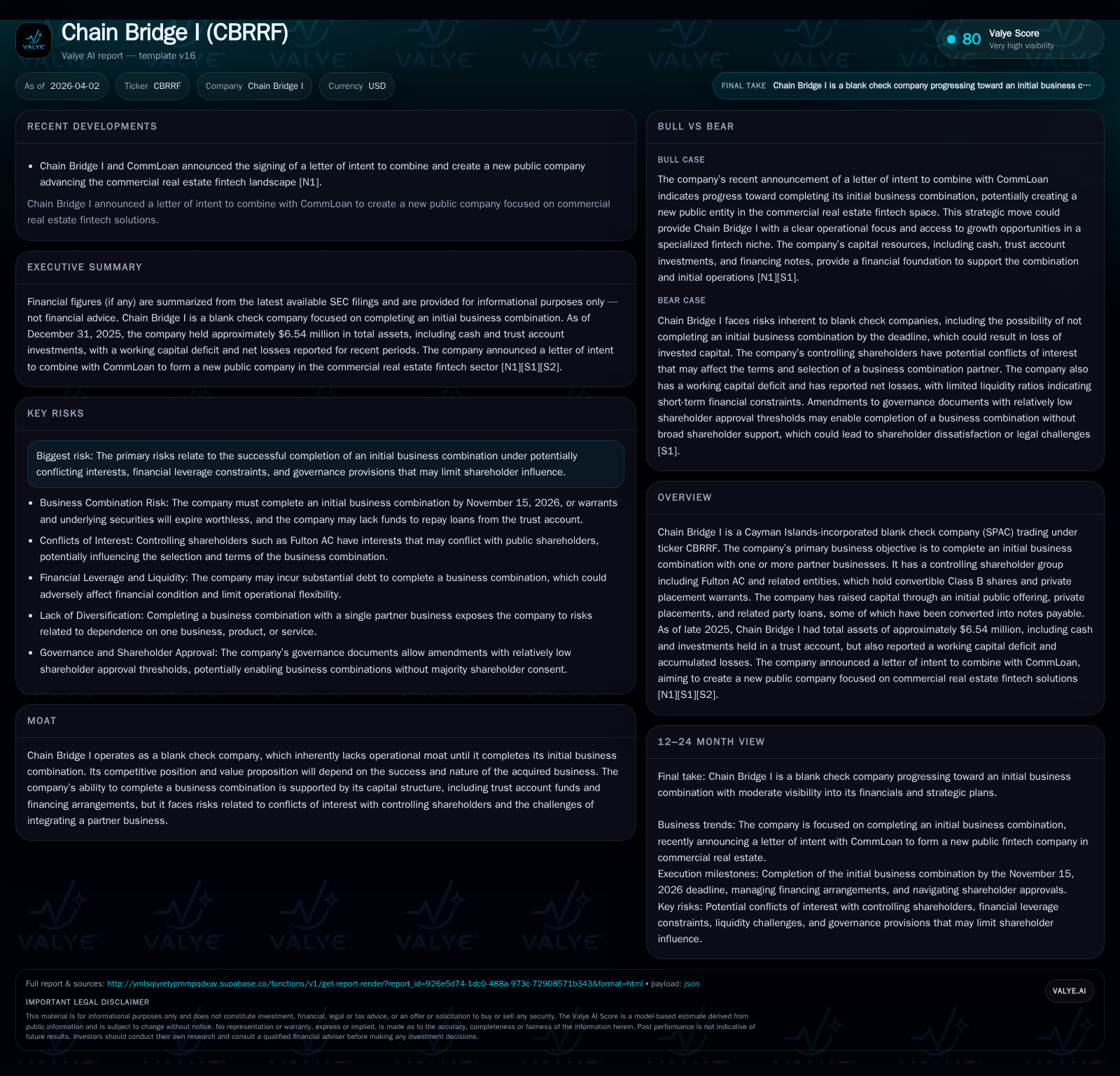

Chain Bridge I Charts Path to Growth Through Initial Business Combination with CommLoan

The Cayman Islands-based SPAC Chain Bridge I advances its planned merger with CommLoan, aiming to enter commercial real estate fintech amidst liquidity and governance challenges.

Chain Bridge I (CBRRF), a Cayman Islands-incorporated blank check company, has raised capital and secured financing to support an initial business combination targeting the commercial real estate fintech sector through CommLoan. Despite substantial funding efforts, the SPAC reported ongoing operating losses and liquidity constraints at the end of 2025, including a working capital deficit and outstanding unsecured promissory notes. The controlling shareholder group’s convertible equity and loan positions introduce governance complexities and potential conflicts of interest. The company aims to complete its business combination by November 15, 2026, after which failure to do so would trigger redemption offers and liquidation per Cayman law.

SPAC Model and Historical Financial Footprint

Chain Bridge I operates as a blank check company incorporated in the Cayman Islands, formed specifically to pursue an initial business combination (IBC) which will establish its first operational platform. As of fiscal year-end 2025, Chain Bridge I remains pre-combination without operating revenues or income streams.

The company has reported consistent operating losses over four consecutive fiscal years: from -$1.39 million in FY2022 to -$956 thousand in FY2025 [F1]. Net income similarly reflects deficits, amounting to approximately -$1.33 million in FY2025 [F1]. Operating cash flow has been negative throughout this period (e.g., -$763K in FY2025), illustrating ongoing cash burn inherent in maintaining the SPAC structure prior to business combination [F1]. Equity is notably negative at approximately -$3.87 million as of December 31, 2025 [F1], reflecting cumulative losses exceeding capital contributions net of buybacks.

This financial profile underscores reliance on external financing until completion of an initial business combination.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | -763581 | -1 | +6.4% |

| 2024 | -1 | -925535 | -2 | -118.7% |

| 2023 | 8 | -964321 | -1 | -28.8% |

| 2022 | 11 | -904319 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 5 | 34.5 |

| 2024 | 41 | 63.6 |

| 2023 | -9556.9 | |

| 2022 | -286.3 |

Source: SEC companyfacts cache [F1].

Note: Operating income improved modestly by FY2025 compared with FY2024 but remained negative; buybacks represent material capital outlays relative to equity levels.

Governance Structure and Capital Formation

Fulton AC and related affiliates such as CBG and CB Co-Investment serve as controlling shareholders holding convertible Class B shares along with private placement warrants exercisable after business combination at fixed terms but without entitlement to trust account liquidation proceeds [S1]. This dual-class share structure grants Fulton AC significant influence despite limited downside protections relative to public Class A shareholders.

Fulton AC has also provided non-interest bearing convertible promissory notes (e.g., Exchange Note exchanged from the Fulton AC Note) that may convert into securities at a premium under certain conditions [S1]. While Class B shares convert into Class A shares lacking trust account redemption rights post-conversion, they provide governance leverage during transaction negotiations and subsequent control.

Such ownership arrangements create potential conflicts of interest when selecting or negotiating with target businesses for the combination since Fulton AC’s interests may not fully align with those of unaffiliated public shareholders [S1][S4][S6].

Liquidity Position and Debt Profile Entering 2026

As of December 31, 2025 Chain Bridge I held approximately $390K in cash against current liabilities exceeding $1.22 million [F1], resulting in a working capital deficit near $808K indicative of constrained short-term liquidity.

The company carries multiple unsecured non-interest bearing promissory notes:

- Bridge Financing Note from Phytanix Bio totaling about $1.02 million as of late 2025 [S4][S22]

- Exchange Note owed to Fulton AC around $369K [S4]

- C/M Note issued September 30, 2025 for principal amount $1.25 million due June 30, 2026 [S4][S22]

These notes mature either upon consummation of the initial business combination or on fixed calendar dates—with no repayment from trust account funds reserved for public investors—highlighting dependence on closing the transaction timely to avoid default or acceleration risks [S4][S22][S24].

Available funds for completing the initial business combination were approximately $1.92 million as of March 27, 2026 excluding anticipated redemptions [S4]. However the low current ratio (~0.34 per [F1]) signals tight liquidity requiring careful capital management.

Initial Business Combination Opportunity and Governance Risks

Chain Bridge I announced a letter of intent to merge with CommLoan—a commercial real estate fintech firm—positioning itself within an innovative sector niche [S1]. This represents Chain Bridge’s growth strategy: transitioning from a blank check entity into an operational company leveraging fintech solutions for real estate finance.

Nonetheless governance risks persist due to Fulton AC’s dual role as lender and major equity holder wielding convertible instruments that may dilute or preferentially position sponsor claims relative to public shareholders [S1]. These conflicts could affect partner selection incentives or negotiation dynamics potentially disadvantaging unaffiliated investors.

Successful execution hinges on transparent deal structuring aligned with regulatory oversight.

Key Milestones and Monitoring Points Through Completion Window

While formal guidance is not provided by management yet several critical milestones are identifiable:

- Regulatory reviews including SEC comment letters or no-action relief supporting listing compliance,

- Shareholder votes approving the proposed business combination,

- Redemption rates among public shareholders impacting deal economics,

- Compliance with November 15th , 2026 deadline for closing the transaction—failure triggers mandatory liquidation procedures,

- Warrant expiration considerations affecting ownership dilution post-merger [S3][S13][S16][S21].

Stakeholders should track relevant filings through mid-to-late 2026 for directional updates.

Capital Allocation Amid Losses and Leverage Constraints

Despite sustained losses and negative equity deepening from roughly -$80K in FY2023 to nearly -$3.9 million in FY2025 [F1], Chain Bridge I has engaged in significant share repurchases totaling more than $4.7 million during FY2025 alone [F1]. These buybacks likely aim at sponsor alignment or capital structure optimization but raise questions given ongoing negative cash flows.

No dividends have been declared consistent with typical SPAC lifecycle practices awaiting transformative business combinations [S29].

Approximate return on equity calculated using FY25 net loss relative to negative equity is about -34.5%, underscoring poor profitability embedded within negative shareholder value context [F1]. Debt leverage from convertible promissory notes further limits flexibility for future investments post-close.

Strategic Risks and Exit Scenarios for Investors

Primary risks center on failure or delay completing the initial business combination which would require redemption offers to public shareholders followed by liquidation under Cayman jurisdiction [S13][S22]. Management disclosures note liquidity concerns tied to debt maturities compounded by lack of new financing commitments beyond existing arrangements [S4].

Post-combination concentration risk emerges as reliance shifts exclusively onto CommLoan’s operational success without diversification buffers [S4]. Debt covenants restrict additional borrowing capacity limiting adaptive response options amid market volatility [S4].

Sponsor conflicts may affect fairness of deal pricing or governance practices making timing and value realization uncertain.

This analysis is based solely on publicly available data up through early April 2026 filings; forward-looking outcomes remain subject to significant uncertainties inherent in SPAC transactions prior to consummation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments